.png)

Stocks’ Details

Tyro Payments Limited

TYR Notifies on Approval of Tender: Tyro Payments Limited (ASX: TYR) is a provider of EFTPOS payments solutions, small business loans as well as banking products to Australian businesses. The market capitalisation of the company stood at A$1.69 Bn as on 14th January 2020. The company recently announced that Danita R. Lowes has become a substantial holder on 6th December 2019 with a voting power of 5.44%. In another update, the company notified that the Department of Human Services has advised that its tender for the provision of Medicare Easyclaim Claiming Services has been marked as successful. Department of Human Services (DHS) also advised that a new contract is under preparation and would be updated on in the near term. The following picture provides an idea of financial performance for FY19:

.png)

Financial Performance (Source: Company Reports)

Future Focus: The company’s key priorities and strategies for FY20 are aimed at continued growth in its payments as well as banking businesses.

Stock Recommendation:The capital management objective of the company intends to maintain enough capital level above the regulatory minimum for providing a buffer against loss arising from unanticipated events, and to allow TYR to continue as a going concern. As per ASX, the stock of TYR is trading below the average of its 52-week trading range of $3.220 - $3.870. Thus, considering the objectives of the company related to capital management and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of A$3.420 per share, up by 0.588% on 14th January 2020.

IOOF Holdings Ltd

Acquisition of Businesses of ANZ: IOOF Holdings Ltd (ASX: IFL) provides services such as financial advice and distribution, portfolio and estate administration, investment management, etc. The market capitalisation of the company stood at A$2.88 Bn as on 14th January 2020. The company recently announced that Renato Mota, Director of the company, has made a change to holdings in the company by acquiring 75,000 performance rights on 17th December 2019. In another update, the company stated that it has received approvals from the Australian Prudential Regulation Authority for holding the controlling stake in OnePath Custodians Pty Limited and Oasis Fund Management Limited. It added that these approvals were the last remaining requirements with respect to the transfer of the ANZ Wealth Pension and Investments business to IFL. The following picture depicts an idea of Funds movement for the quarter ended 30 September 2019:

.png)

Fund Movements (Source: Company Reports)

Focused on Shareholder’s Value:The company is well-positioned for delivering value to its shareholders in the future. The recent investment into uplifting governance as well as the client focus provides a valuable foundation that would benefit all clients and members including those from the ANZ P&I business.

Valuation Methodology: P/E Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per the key personnel of the company, the proprietary platforms continue to attract significant inflows. The company is constantly benchmarking its proprietary solutions to best in market offerings, ensuring that they meet its advisers and their client needs. Debt to equity multiple of the company stood at 0.26x in FY19 as compared to the industry median of 0.47x. We have valued the stock using P/E based relative valuation method and arrived at a target price, which is offering an upside of higher single-digit (in percentage terms).Thus, in the light of decent growth in FUM in Q1FY20, decent outlook and deleveraged balance sheet, we give a “Hold” recommendation on the stock at the current market price of A$8.280 per share, up 1.099% on 14th January 2020.

EML Payments Limited

Awarded with New Agreement: EML Payments Limited (ASX: EML) is an issuer of pre-paid financial cards and the market capitalisation of the company stood at A$1.59 Bn as on 14th January 2020. The company via a release confirmed that it has been given a 5 + 2-year agreement with NSW Health to act as a provider of branded General-Purpose Reloadable card programs for employee salary packaging. EML has replaced Bellamy's Australia Limited on S&P/ASX 200, which came into effect on 11th December 2019. Also, the company has recently wrapped up the retail component of its fully underwritten 1 for 5 accelerated pro-rata non-renounceable entitlement offer and raised around A$93 million. The below picture depicts a track record of EBITDA growth:

.png)

EBITDA Growth (Source: Company Reports)

Focused on Improving its Product Offerings: As per the 2019 Annual report, the company would continue to grow volumes by recognising opportunities that offer significant payment volumes. EML would also continue to improve its product offerings as well as actively target clients in high volume industries.

Valuation Methodology: P/B Multiple Approach

.png)

P/B Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Net margin of the company stood at 8.7% in FY19, reflecting YoY growth of 5.6%. This reflects that the company has improved its position to convert its top-line into the bottom-line. Debt to equity multiple of the company stood at 0.10x in FY19 against the industry median of 0.40x. We have valued the stock using Price to Book based relative valuation method and for this purpose, we have taken the peer group – Pushpay Holdings Ltd (ASX: PPH), SmartPay Holdings Ltd (ASX: SPY), NEXTDC Ltd (ASX: NXT), and reached at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering the improvement in margins, outlook and valuation, we maintain a “Hold” recommendation on the stock the current market price of A$5.230 per share, up by 7.172% on 14th January 2020, primarily due to the confirmation of new agreement with NSW Health.

Challenger Limited

CGF Introduces New Funds Management Products: Challenger Limited (ASX: CGF) is a multi-faceted financial services organisation having its core businesses in annuities, funds management and administration platforms. The market capitalisation of the company stood at A$5.07 Bn as on 14th January 2020. The company recently announced that Challenger Limited and its entities have become an initial substantial holder in Pendal Group Limited on 20th December 2019 with a voting power of 5.08%. During FY19, the company has delivered across all four pillars of its strategy. It announced an expanded strategic partnership with MS&AD and brought new funds management products to the market. The following picture depicts an idea of the 2020 financial calendar:

2020 Financial Calendar (Source: Company Reports)

Guidance for NPBT: For FY20, the company is aiming for a normalised net profit before tax in the range of $500 million and $550 million. The guidance for FY20 fully accounts for the impact of low interest rates as well as for the disruption the company has witnessed in the Australian wealth management industry. The company expects this to continue throughout FY20.

Valuation Methodology: P/E Multiple Approach

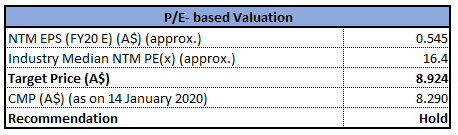

P/E Based Valuation (Source: Thomson Reuters)

Valuation Methodology: P/B Multiple Approach

P/B Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has commenced FY20 with total assets under management in a decent position, which stood at $84 billion in Q1, reflecting a rise of 3%. This increase came in as a result of strong flows in the business and by positive investment markets. The stock of CGF has generated returns of 22.29% and 21.04% over a period of three months and six months, respectively. We have valued the stock using P/E and P/B based relative valuation methods and arrived at an upside of single-digit (in percentage terms). Thus, in light of a decent start to FY20 and favourable upside, we maintain a “Hold” rating on the stock at the current market price of A$8.290 per share on 14th January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...