.png)

Stocks’ Details

Premier Investments Limited

Closure of All Retail Stores: Premier Investments Limited (ASX: PMV) operates numerous specialty retail fashion chains within the specialty retail fashion markets in Australia, New Zealand, Asia and Europe. The market capitalisation of the company stood at $2.21 Bn as on 28th April 2020. The company closed all its retail stores in Australia on 22nd April 2020 as protective measures imposed by the Federal and State governments to stop the spread of COVID-19. In addition, the state Governments have implemented measures to continue these restrictions (social distancing, public gathering, and stay home directions) until at least 11 May 2020. Hence, the company has decided to temporarily close its all retail stores until 11th May 2020.

During 1HFY20, the company reported net profit after tax amounting to $99.6 million, reflecting a rise of 12.2%. The company has recorded a fully franked interim dividend of 34 cps, which indicates the decent balance sheet and long-term strength of the Group.

.png)

Net Profit after Tax (Source: Company Reports)

Focus for Future Growth: Going forward, the company is planning to significantly grow its Smiggle business and will be focused on the expansion and growth of online businesses.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: With respect to the retail segment, the company reported a decline of 94 bps in CODB (Cost of Doing Business). The costs for the segment would continue to be well controlled despite structural inflationary pressure. We have valued the stock using P/CF-based illustrative relative valuation method, and for the purpose, we have taken peers such as JB Hi-Fi Ltd (ASX: JBH), Bapcor Ltd (ASX: BAP), etc., and arrived at a target price with an upside of lower double-digit (in percentage terms). Therefore, considering thestrong balance sheet, long-term strength of the Group and decline in CODB, we give a “Buy” recommendation on the stock at the current market price of $14.270 per share, up by 2.367% on 28th April 2020.

Wesfarmers Limited

Sales Growth in Bunnings and Officeworks: Wesfarmers Limited (ASX: WES) is primarily engaged in retailing of home improvement and outdoor living products and supply of building materials. The market capitalisation of the company stood at $42.66 Bn as on 28th April 2020. The company recently announced that every single business of the group has executed numerous changes to protect the health and safety of team members and customers. This mainly includes store-based measures to support social distancing requirements, the launch of protective screens at registers and increased levels of personal protective equipment for team members.

WES added that Bunnings and Officeworks have experienced significant growth in demand during March and April. Hence, sales growth in Bunnings and Officeworks for the Q3 FY20 and the first three weeks of April has increased in comparison to the levels achieved during 1H FY20.

.png)

1H FY20 Results (Source: Company Reports)

Focused on Shareholders Returns: The company is well-placed to deliver satisfactory shareholder returns over the long term with the help of its portfolio of cash-generative businesses along with the leading market position. WES is focused on operating its businesses in a manner so that it protects the health and safety of its teams and customers during this uncertain period.

Valuation Methodology: P/BV Multiple Based Relative Valuation (Illustrative)

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has undertaken numerous actions to strengthen its balance sheet, which include the sale of a 5.2% interest in Coles for pre-tax proceeds of around $1,060 million on 31st March 2020. We have valued the stock using P/BV based illustrative relative valuation method and for the purpose, we have taken peers such as JB Hi-Fi Ltd (ASX: JBH), Woolworths Group Ltd (ASX: WOW) and Coles Group Ltd (ASX: COL) and arrived at a target price with an upside of single digit (in percentage terms). Hence, in light of the steps taken to strengthen the balance sheet and sales growth, we give a “Hold” recommendation on the stock at the current market price of $37.730 per share, up by 0.292% on 28th April 2020.

Select Harvests Limited

A Quick Look at 2020 Crop: Select Harvests Limited (ASX: SHV) is engaged in growing, processing and packaging of almonds from company-owned orchards and investor-owned orchards. The market capitalisation of the company stood at $687.68 Mn as on 28th April 2020. Recently, the company has notified the market with the 2020 crop update and stated that 97% of its orchards have been harvested. It added that 90% of the crop has been harvested in near perfect conditions and the remainder of the harvest has been disrupted by rain events, but there was no effect on quality as the later harvest varieties are closed shell. The company has delivered 60% of the estimated crop to its Carina West processing facility, and more than 25% of the crop has been processed

Coming to the market condition, the February Almond Board of Australia full-year Position report stated a rise of 26% to 76,556MT in exports on a YoY basis. The below picture gives an idea of financial performance for FY20:

.png)

FY20 Financial Highlights (Source: Company Reports)

Benefits from Investments: The company is witnessing benefits from the continued investment in its horticultural practices as well as new technology in the Company’s northern Victorian processing facility.

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 2.74x in FY19 as compared to the industry median of 1.42x. This reflects that SHV is in a decent position to address its short-term obligations against the broader industry. Debt to equity multiple of the company stood at 0.09x against the industry median of 0.27x. We have valued the stock using P/E multiple based illustrative relative valuation method and for the purpose, we have taken peers such as Tassal Group Ltd (ASX: TGR), Graincorp Ltd (ASX: GNC), Elders Ltd (ASX: ELD) etc., and arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, considering the decent liquidity position and deleveraged balance sheet, we maintain a “Hold” recommendation on the stock at the current market price of $6.860 per share, down by 4.056% on 28th April 2020.

Asaleo Care Limited

Returned to Positive Cash Position: Asaleo Care Limited (ASX: AHY) is engaged in the manufacturing, marketing and distribution of consumer products in relation to feminine hygiene. The market capitalisation of the company stood at $537.69 Mn as on 28th April 2020.During FY19, underlying EBITDA witnessed a decline of 10.9% to $82.4 million, due to significant rise in advertising & promotion spend and incremental investment in trade promotional activity to generate sales growth and protect market share. During 2H FY19, the company returned to positive cash generation and paid an unfranked dividend of 2 cents per share.

.png)

FY19 Highlights (Source: Company Reports)

EBITDA Guidance: For FY20, it expects underlying EBITDA to be in the range of $84 - $87 million.The company expects both a positive and negative impact on its business due to economic uncertainty caused by COVID-19 pandemic, with the net position expected to be in-line with previous guidance.

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation (Illustrative)

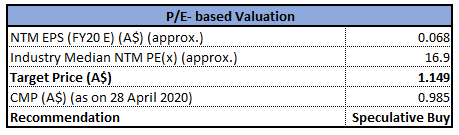

Price to Earnings Multiple Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The focus of AHY for 2020 is to drive sales growth, a differentiated offer and supply chain excellence. Return on equity of the company stood at 16.4%, reflecting YoY growth of 16.0%. We have valued the stock using P/E multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). During the span of one month and six months, the stock of AHY has provided returns of 2.06% and 5.88%, respectively. Thus, considering key focus area for 2020 and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.985 per share, down by 0.505% on 28th April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...