.png)

Stocks’ Details

Qantas Airways Limited

CEO’s Address to Shareholders:Qantas Airways Limited (ASX: QAN) is in the operation of international and domestic air transportation services. The company is also involved in the sale of worldwide and domestic holiday tours. The market capitalisation of the company stood at A$9.86 Bn as on 25th October 2019. Chief Executive Officer- Alan Joyce addressed the shareholders recently and stated that the company is resilient in a challenging operating environment and that resilience comes from the collective strength of the portfolio of businesses. With respect to domestic market, the Management stated that its dual brand strategy has continued to deliver in FY19. It was mentioned in the release that Qantas International rebounded strongly, following a steep increase in fuel prices at the start of FY19. The following picture provides an overview of results for Q1 FY20:

.png)

Results of Q1 FY20 (Source: Company Reports)

What to Expect:As per the Chairman’s address to shareholders, the company is taking important steps to decrease 75% of its waste to landfill by the end of 2021 and removing 100 Mn single use plastics from its operations by the end of 2020. The company recently came up with its quarterly updates for FY20, which showed the Group’s resilience in the face of mixed markets.

Stock Recommendation: At the current market price of $6.250, the stock is trading at a price to earnings multiple of 11.500x. The stock has gained 9.79% in the last 6 years and is currently trading above the average of its 52-week high and low. Gross margin and operating margin of the company stood at 53.2% and 8.1% in FY19 as compared to the industry median of 39.7% and 7.4%, respectively. However, the net margin reached to 5.0% in FY19 against the industry median of 4.2%. This implies that the company has better capabilities to convert its top-line into the bottom-line in comparison to the broader industry. On the valuation front, the company is trading at EV to EBITDA multiple of 4.2x as compared to the industry median 6.7x on TTM basis. The stock has EV to sales multiple of 0.7x over the industry median of 1.6x on TTM basis. Hence, considering the decent key metrics, valuation parameters and the company’s resilience in the face of mixed market, we maintain a “Hold” rating on the stock at the current market price of A$6.250 per share, down 0.478% on 25th October 2019.

Medibank Private Limited

Response Towards the Proceedings by ACCC:Medibank Private Limited (ASX: MPL) is in the business of underwriting and distributing private health insurance policies under its two brands, Medibank and ahm as a private health insurer. The company would be conducting its 2019 Annual General Meeting on 14th November 2019. As per the release dated 3rd September 2019, Medibank and ahm have responded the proceedings by Australian Competition and Consumer Commission (ACCC), which was related to an issue identifying eligibility when responding to customer enquiries and paying claims for joint investigations and reconstruction procedures for customers on ahm Boost and Lite products.

It was outlined in the release that Medibank voluntarily notified the ACCC of the issue in 2018 and briefed the regulator on its approach to customer communication as well as its compensation process. Medibank has been working cooperatively with the ACCC across its investigation. The following picture depicts an idea of financial results for FY19:

.png)

Results Summary (Source: Company Reports)

Future Aspects: The company anticipates witnessing Medibank brand volumes stabilise by the end of FY20 and grow during FY21 on the back of current policyholder trajectory. It added that the hospital and extras utilisation growth to remain around current levels for FY20 with prostheses expenditure anticipated to add modestly to claims growth against FY19.

Stock Recommendation:The company aims to continue to aspire for stronger growth in volumes at a reasonable margin, while retaining the continued tight control of its management expenses. The asset to equity ratio of the company stood at 1.88x in FY19 as compared to the industry median of 5.89x. However, on the valuation front, the stock of MPL is trading at the EV to Sales multiple of 1.4x as compared to the industry median of 5.5x on TTM basis. The stock is available at an EV to EBITDA multiple of 11.2x against the industry median of 11.5x on TTM basis. On the stock’s performance front, it produced a return of 20.08% in the time period of six months. Therefore, in light of above-stated facts and current trading levels, we give a "Hold" recommendation on the stock at the current market price of A$3.410 per share on 25th October 2019.

BINGO Industries Limited

A Look at the Acquisition of DADI:BINGO Industries Limited (ASX: BIN) is a provider of recycling and waste management solutions throughout building demolition, commercial and industrial waste streams with capabilities across waste collections, processing, separation and recycling components of the waste value chain. The market capitalisation of the company stood at A$1.58 Bn as on 25th October 2019. The company announced that it would be holding its Annual General Meeting for 2019 on 13th November 2019. The management of the company stated that DADI acquisition has materially changed its business, and it made a great progress since completion, integrating DADI into its operations. The contribution from DADI since the completion of the acquisition was in-line with the anticipations.

.png)

Key Metrics (Source: Company Reports)

Future Prospects:The company is on track to deliver annualised cost synergies amounting to $15 Mn over the two years from FY20. It has exceeded the network capacity target of 3.4 Mn tonnes per annum in FY 2019 after the completion of announced development program along with the acquisition of DADI. It added that the network reconfiguration plan is well-advanced and is anticipated to return $80 Mn via the sale of non-core assets and Banksmeadow in FY20.

Stock Recommendation:The Board of the company declared a final dividend amounting to 2.0 cps. In combination with the half-year dividend of 1.72 cents, which was paid on March 2019, the total dividend for the year stands at 3.72 cps. Gross margin and EBITDA margin of the company stood at 53.2% and 25.3% in FY19 as compared to the industry median of 39.0% and 22.4%, respectively. The current ratio of the company stood at 0.99x in FY19, reflecting a YoY growth of 2.7%. This implies that BINGO has improved its position to address its short-term obligations. When it comes to the price performance, it delivered returns of 7.11% and 38.90% over the period of one month and six months, respectively. Hence, considering the acquisition of DADI, decent metrics, dividend to shareholders, etc., we give a “Buy” recommendation on the stock at the current market price of A$2.360 per share, down 2.075% on 25th October 2019.

Helloworld Travel Limited

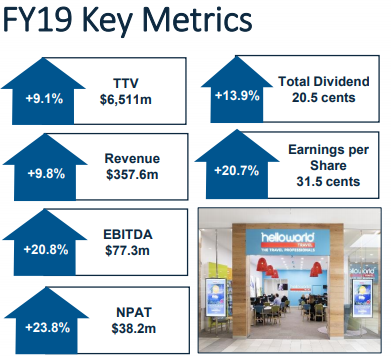

Acquisition of TravelEdge:Helloworld Travel Limited (ASX: HLO) is involved in the selling of international and domestic travel products and services. The company is also in the operation of retail distribution networks of travel agents. The company recently updated the market with the results for quarter ended 30 September 2019, i.e., Q1FY20, wherein it stated that it is a strong start to the financial year 2020 and reported TTV for the quarter amounting to $1.878 Bn, reflecting a rise of 10.4% over the same period last year and was up 9.2%, excluding the impact of business acquisitions and disposals. On 30th September 2019, the company wrapped up the acquisition of TravelEdge, and now has annualised corporate TTV of more than $1.6 Bn, which makes the company’s corporate division the second-largest corporate travel business in ANZ.

Key Metrics (Source: Company Reports)

Future Guidance. Following the completion of the acquisition of TravelEdge, the company announced a revision in EBITDA guidance to $86 Mn - $90 Mn in comparison to the earlier guidance range of $83 Mn to $87 Mn, provided on 17th September 2019. However, the guidance is subject to no material change in trading conditions over the remainder of the financial year. This excludes the impact of the new lease accounting standard.

Stock Recommendation:On the valuation front, the stock of HLO is trading at EV to sales multiple of 1.5x in comparison to the industry average of 3.4x on TTM basis. It has EV to EBITDA multiple of 6.7x against the industry median of 7.7x on TTM basis. Net margin of the company stood at 10.7% in FY19 against the industry median of 9.2%. This implies that the company has better capabilities to convert its top-line into the bottom-line as compared to the broader industry. As per the ASX, HLO is trading towards its 52-week lower levels which can be considered a decent level to make an entry into the stock. Hence, considering the updated guidance for EBITDA, the recent acquisition of TravelEdge as well as valuation parameters, we give a “Buy” recommendation on the stock at the current market price of A$4.480 per share, down 0.665% on 25th October 2019.

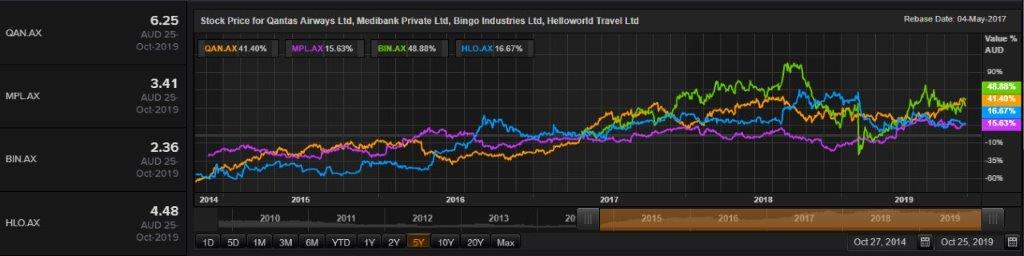

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...