.png)

Stocks’ Details

Transurban Group

TCL Successfully Completed Its $500 Mn ‘Pro-Rata’ Institutional Placement: Integrated transport company, Transurban Group (ASX: TCL) is involved in the development, operation, maintenance and financing of toll assets as well as management of the associated customer and government relationships. The company recently announced that it has successfully completed its $500 Mn ‘pro-rata’ institutional placement at a placement price of $14.70 per new stapled security. The proceeds raised under the placement and security purchase plan will contribute to funding Transurban’s acquisition of the remaining 34.62% interest in M5 West for $468 Mn (excluding stamp duty and transaction costs of $47 Mn), and for general corporate purposes. TCL will issue 34,013,606 new securities under the Placement which will rank equally with ordinary securities from the date of allotment. The new securities are not entitled to the FY19 final distribution of 30 cents per security because the record date for that distribution was 28 June 2019. In addition to the Placement, TCL will undertake a non-underwritten SPP, to be capped at $200 Mn to the eligible holders of Transurban securities.

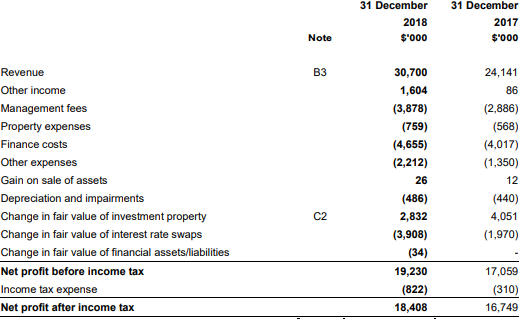

FY19 (ended on June 30, 2019) Key Highlights: The total revenue increased by 26.3% to $4.17 Bn in FY19 as compared to $3.30 Bn in FY18. EBITDA for FY19 increased by $347 Mn. The profit from continuing operations for FY19 was reported at $170 Mn as compared to $468 Mn in FY18.

.png)

FY19 Income Statement (Source: Company Reports)

What to expect: As per the report, FY20 distribution guidance of 62.0 cents per security has been provided including 4.0 cps fully franked.

Stock Recommendation: Its EBITDA margin for FY19 stands at 48.5%, better than the industry median of 47.2%. Its cash cycle for FY19 stands at negative of 75.8 days, lower than the industry median of 32.3 days, which implies the company is efficiently converting its investments into cash flows.Its dividend yield has been reported at 3.87%.

Hence, considering the aforesaid facts and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $15.190 per share (down 0.263% on August 8, 2019).

Rural Funds Group

RFF’s Share Rose Over 41% Post Response To Bonitas Research LLC: Rural Funds Group (ASX: RFF) is involved in the leasing of agricultural properties and equipment. Recently, Bonitas Research LLC selectively released a document about the financial position of RFF.In response, Rural Funds Management Limited has engaged Ernst & Young to independently investigate the matters raised and assess RFF's rejection of each of the claims made in the document.

On 31st July 2019, RFF updated the market about the dividend/distribution of AUD 0.02607500 on security ‘RFF - FULLY PAID UNITS STAPLED SECURITIES’ with ex-date, record date, and payment date on June 27, 2019, June 28, 2019 and July 31, 2019, respectively.

H1FY19 Performance Highlights: Rural Funds Management Ltd (RFM), as a responsible entity and manager of the Rural Funds Group (RFF), announced HY 2019 financial results. There was a 7% increase in the adjusted funds from operations (AFFO) to 6.4 cpu and 4% increase in the distributions per unit (DPU) to 5.22 cents.

H1FY19 Income Statement (Source: Company Reports)

What to expect: RFM has confirmed FY19 forecast AFFO of 13.2 cpu and distributions of 10.43 cpu. RFM would continue to oversee as well as manage the existing assets and developments while considering new investments and lessees.

Stock Recommendation: RFF’s annual dividend yield stands at 7.67%. It is presently trading slightly above the average of 52 weeks high and 52 weeks low levels. Its gross margin and EBITDA margin for H1FY19 stood at 97.5% and 82.9%, better than the industry median of 74.1% and 62.2%, respectively, which implies decent fundamentals of the company. Its current ratio for H1FY19 stood at 0.88x, better than the industry median of 0.49x, which implies the company is in a better position to address its short-term obligations. Hence, considering the aforesaid facts and current trading levels, we give a “Hold” recommendation on the stock at the current price of $1.920 per share (up 41.176% as on August 8, 2019).

National Storage REIT

Undervalued Position at The Current Juncture: National Storage REIT (ASX: NSR) is a fully integrated owner and operator of self-storage centres. The company recently announced that Mitsubishi UFJ Financial Group, Inc. became a substantial holder in the company with the voting power of 5.90%, effective from August 2, 2019. On June 24, 2019, NSR informed the market about the dividend/distribution of AUD 0.05100000, with record date and payment date on June 28, 2019 and September 5, 2019, respectively.

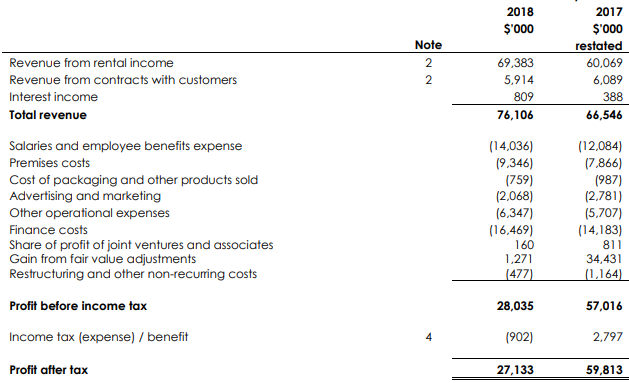

H1FY19 Key Highlights: The IFRS profit after tax decreased by 55% on pcp to $27.1 Mn. The underlying earnings for the period increased by 17.4% on pcp to $26.3 Mn. The following picture provides an overview of the company’s key financial numbers:

H1FY19 Income Statement (Source: Company Reports)

What to Expect: As per the reports, with the capital raising plans via institutional and security purchase plan to replenish investment capacity and maintain funding flexibility, NSR expects its FY20 earnings growth to be not less than 4%. Its strategy is expected to accelerate earnings and value growth as the proceeds are deployed, and assets are incorporated into the NSR portfolio.

Stock Recommendation: NSR’s annual dividend yield stands at 5.82%. Its ROE for H1FY19 stood at 31.5%, better than the industry median of 5.0%, which implies the company generated better return for its shareholders than its peer group. Its current ratio for H1FY19 stood at 1.46x, better than the industry median of 0.49x, which implies the company is in a better position to address its short-term obligations than its peer group. On the valuation front, its next-twelve-months EV/Sales and EV/EBITDA multiple stand at 11.1x and 18.6x, lower than the industry median of 16.5x and 18.7x. Hence, considering the aforesaid facts and current trading levels, we give a “Hold” recommendation on the stock at the current price of $1.660 (up 0.606% as on August 8, 2019).

Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...