.png)

Stocks’ Details

Syrah Resources Limited

Maintaining existing market and operational capability:Syrah Resources Limited (ASX: SYR) is a leading high-quality natural graphite producer with a market capitalization of ~$120.22 million (as at 22 May 2020). On 22 May 2020, the company held its virtual Annual General Meeting (AGM), wherein the Management highlighted that Syrah is currently focused on maintaining existing market and operational capability during challenging near-term market conditions. In the meeting, the management emphasized on the company’s Balama operations and assured that Balama is well-positioned to translate the demand growth of natural graphite to improvement in the equity value of the company’s stockholdings.

March Quarter Highlights:During the March quarter, the company produced 12kt natural graphite from Balama operaions, 3Kt lower than the previous quarter, due to prevailing demand in China which was negatively impacted by COVID 19 supply chain disruptions. Over the quarter, the company sold and shipped 7kt of graphite, 10kt lower than the prior quarter, mainly due to supply chain disruptions in China due to COVID 19. At the end of the March quarter, the company had a cash balance of US$64.7 million.

.png)

Balama Production and Sales (Source: Company Reports)

What to expect:Moving forward, the company is focused on growing Balama’s position in a rebalanced market with an asset cost structure and operating methodology more adaptable to market conditions. The company is positioning its Balama operations to meet the challenges caused by the unprecedented COVID-19 situation.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

* 1 USD = ~1.53 AUD

EV/Sales Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the last six months, the stock of SYR has corrected by 27.5% on ASX and is inclined towards its 52-week low of $0.150, offering investors an opportunity for accumulation. For FY19, the company reported current ratio of 7.49x, higher than the industry median of 1.76x, demonstrating that the company is well-equipped to pay its short-term obligations. We have valued the stock using EV/Sales multiple based illustrative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like Orocobre Ltd (ASX: ORE), Galaxy Resources Ltd (ASX: GXY) and Pilbara Minerals Ltd (ASX: PLS). Considering the company’s robust liquidity position, current trading levels, and potential for further growth, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.285, down by 1.724% on 22 May 2020.

Cooper Energy Limited

Commissioning of Orbost Gas Processing Plant: Cooper Energy Limited (ASX: COE) is an energy company which generates revenue from gas supply to south-east Australia and low-cost Cooper Basin oil production. On 22 May 2020, the company announced regarding the commissioning of the Orbost Gas Processing Plant which processes gas from Cooper Energy’s Sole gas field for supply to customers in south-east Australia. Ongoing commissioning plans are focused on achieving a progressive, sustained increase in output rates while maintaining stable plant operation.

March Quarter Update:During the March 2020 quarter, the company reported production of 0.28 million boe, up from 0.27 million boe in the prior quarter. For the quarter, the company reported sales revenue of $15 million, taking the year to date revenue to $54.1 million. At the end of the March quarter, the company had a cash balance of $142.5 million and net debt of $84.4 million.

.png)

March Quarter Results (Source: Company Reports)

FY20 Guidance:For FY20, the company expects its total output to be around 1.2 million barrels of oil equivalent from its existing operations in the Otway and Cooper basins. For the full year, the company expects its capital expenditure to be in the middle of $86 million - $93 million.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earning Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months,

Stock Recommendation:In the last three months, the stock of COE corrected by 27.78% on ASX, and is inclined towards its 52 weeks low price of $0.340, offering investors a decent opportunity for accumulation. The company has a current ratio of 2.7x, higher than the industry median of 1.06x, demonstrating that the company is well equipped to pay its short-term obligations. We have valued the stock using a Price to Earnings multiple based illustrative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like Senex Energy Ltd (ASX: SXY), New Hope Corporation Ltd (ASX: NHC) and Z Energy Ltd (ASX: ZEL). Considering the company’s current trading levels, its liquidity position, and FY20 guidance, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.410, up by 5.128% on 22 May 2020, owing to the recent Sole Gas Project update.

Western Areas Limited

Major Drill programme at Mt Alexander Project: Western Areas Limited (ASX: WSA) is an Australian metal and mining company, primarily involved in the exploration of Nickel. The company currently owns 25% interest in the Mt Alexander project, located in the north-eastern Goldfields. The remaining 75% is owned in St George Mining Limited (ASX: SGQ), a growth focused Western Australian nickel company. On 22 May 2020, SGQ announced that it has commenced a major drill programme at Mt Alexander, to test new conductive features identified by the magnetotelluric (MT) and audio-magnetotelluric (AMT) surveys completed earlier this year.

March Quarter Highlights:During the March 2020 quarter, the company mined 5,896 tonnes of Nickel, taking the year to date total to 17,550 tonnes. During the quarter, the company implemented several measures to protect its employees and staff from Covid-19 virus. It is to be noted that, the company’s Nickel production and sales volumes proceeded as planned during the quarter with guidance remaining on track for FY20, following the implementation of Covid-19 plans. Despite the various challenges encountered during the quarter, the company’s Forrestania operations produced reliable operating result and delivered a backlog of concentrate from the prior quarter.The company is currently in a strong financial position with around $181.4 million cash at bank as at 31 March 2020, and no debt.

.png)

March Quarter Result (Source: Company Reports)

Valuation Methodology: Price to Book Multiple Based Relative Valuation

.png)

Price to Book Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months,

Stock Recommendation: With a strong financial position, the company is currently well placed to emerge from the COVID-19 pandemic. In the past six months, the stock of WSA has corrected by 19.72% on ASX and is currently inclined towards its 52 weeks low price of $1.625, offering investors an opportunity for accumulation. We have valued the stock using a Price to Book Value multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like Nickel Mines Ltd (ASX: NIC), IGO Ltd (ASX: IGO) and Panoramic Resources Ltd (ASX: PAN). Considering the company’s resilient performance during the March quarter, its current trading levels, and strong financial position, we give a “Buy” recommendation on the stock at the current market price of $2.220, down by 2.632% on 22 May 2020.

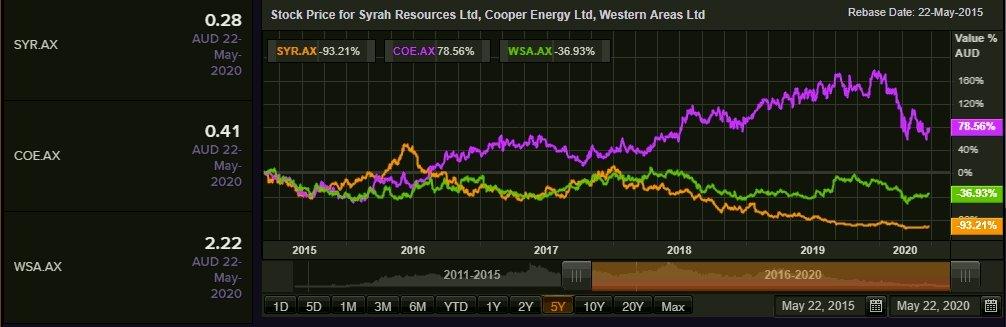

Comparative Price Chart(Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...