Kalkine has a fully transformed New Avatar.

.png)

Stocks’ Details

South32 Limited

Strong Operating Results for 1HFY20:South32 Limited (ASX: S32) is engaged in mining and metal production from a portfolio of assets.

Performance Highlights for 1HFY20: During the half year ended 31st December 2019, the company reported a strong operating performance against a challenging scenario for key commodities. The company has invested in exploration to improve its portfolio performance and deliver better returns for shareholders. During the half, it reported record production at Brazil Alumina. The company entered into an agreement for the sale of its South Africa Energy Coal business and advanced its pre-feasibility study at Hermosa. At the end of the period, the company had a net cash balance of US$277 million. Revenue for the period came in at US$3,216 million, down 16% on the prior corresponding period revenue of US$3,811 million due to lower realised prices for key commodities..png)

1HFY20 Results (Source: Company Reports)

Valuation Methodology: P/CF Based Valuation.png)

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 8.60% in the past one month and is currently trading below the average of its 52-week trading range of $2.360 - $3.973. As a result of a strong operating performance in the first-half, the company has reduced the FY20 operating unit cost guidance for most of its operations and has also reduced the capital expenditure guidance as the plans to open new mining areas were deferred. We have valued the stock using Price to Cash Flow based relative valuation method and for the purpose, have taken the peer group - Rio Tinto Ltd (ASX: RIO), BHP Group Ltd (ASX: BHP), Iluka Resources Ltd (ASX: ILU), etc. As a result, we have arrived at a target price offering an upside of lower double-digit (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $2.590, up 1.569% on 13th February 2020.

Newcrest Mining Limited

NCM Invests for Future Growth:Newcrest Mining Limited (ASX: NCM) is engaged in the exploration, mine development and operation, and sale of gold. The company also provides gold and copper concentrate.

Highlights of Half-Year Results: During the six months ended 31st December 2019, the company reported production of gold at 1.1 million ounces, representing a decline of 12% on the prior corresponding period. All-In Sustaining Cost for the period was 18% higher than the prior corresponding period at US$880 per ounce. Gold revenue for the period came in at US$1,497 million, up 2% on the prior corresponding period. The company highlighted that in the first half it invested to increase its potential for future growth. For instance, the company acquired 70% of the Red Chris mine in Canada. Adjusted free cash flow before the acquisition of Red Chris and additional investment in Lundin Gold came in at US$106 million..png)

Mineral and Ore Reserves Estimate: The company also provided an update on its Mineral resources and Ore Reserves estimates for the 12 months ended 31st December 2019. Ore reserves and mineral resources are expected to contain 52 million ounces and 110 million ounces of gold, respectively.

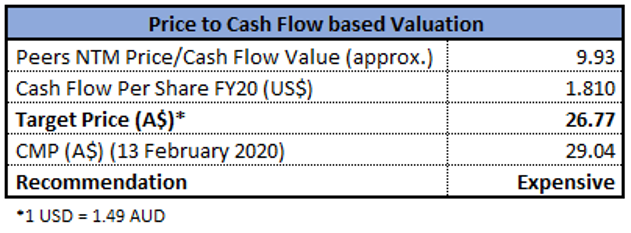

Valuation Methodology: P/CF Based Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 3.90% over a period of 1 month and is currently trading close to the average of its 52-week high and low of $38.870 and $23.530, respectively. The company reported robust drilling results at Havieron and Red Chris during the first half. In the second half, the company expects to report a stronger free cash flow as compared to the first half, which was impacted by the acquisition and investment. We have valued the stock using Price to Cash Flow based relative valuation method and for the purpose, have taken the peer group - Evolution Mining Ltd (ASX: EVN), Northern Star Resources Ltd (ASX: NST), Silver Lake Resources Ltd (ASX: SLR), etc. As a result, we have arrived at a price correction of higher single-digit (in % terms). Hence, we give an “Expensive” rating on the stock at the current market price of $29.040, down 1.726% on 13th February 2020.

Woodside Petroleum Limited

WPL Focused on Strengthening its Balance Sheet Position:Woodside Petroleum Limited (ASX: WPL) is engaged in hydrocarbon exploration, evaluation, development, production and marketing.

On 13th February 2020, the company released the annual report for the period ended 31st December 2019. During the period, the company reported gas production of 89.6 MMboe, at a unit production cost of US$3.9 per boe. Production for the period was below the target of 91 MMboe due to extended plant turnarounds and Tropical Cyclone Veronica. Net profit after tax came in at US$343 million. Profit during the period was impacted by delays in business plan priorities and impairment of the Kitimat LNG asset.

Outlook: For 2020, the company is expecting investment expenditure in the range of US$4,100 million - US$4,400 million, representing increased expenditure on growth projects and exploration expenditure. NPAT for the period will see a consolidated impact of US$34 million, by movements in the Brent oil price and the AUD/USD exchange rate.

Valuation Methodology 1: P/CF Based Valuation

P/CF Based Valuation (Source: Thomson Reuters)

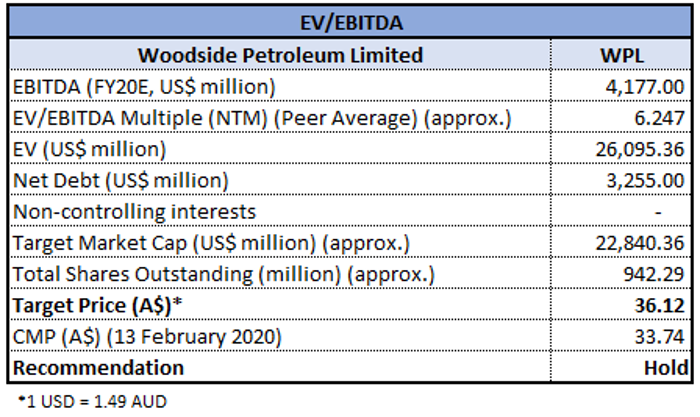

Valuation Methodology 2: EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated returns of 1.93% over a period of 6 months. Currently, the stock is trading close to the average of its 52-week high and low of $37.700 and $30.580, respectively. The company is focused on building a resilient balance sheet and had a liquidity position of US$6,952 million at the end of FY19, against a net debt of US$2,791 million. Moreover, the company is actively engaged in managing its debt portfolio and aims to minimise near-term maturities awhile maintaining a low cost of debt. We have valued the stock using Price to Cash Flow and EV/EBITDA based relative valuation methods. For the purpose, we have taken the peer group - Oil Search Ltd (ASX: OSH), Beach Energy Ltd (ASX: BPT), Origin Energy Ltd (ASX: ORG), etc. As a result, we have arrived at a target price offering an upside of single-digit (in % terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $33.740, down 0.354% on 13th February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...