.png)

Stocks’ Details

Alumina Limited

FY19 Results Highlights:Alumina Limited (ASX: AWC) is a metal and mining company focused on refining the intermediate alumina product in the aluminium supply chain. The company has a 40% interest in the AWAC joint venture and 55% interest in the Portland aluminium smelter in Victoria Australia. In 2019, the company reported a net profit after tax of US$326.6 million and EBITDA of US$1,260.7 million. During the years, the company experienced a softening alumina market leading to a steady decline in the Alumina Price Index (API). Despite softer prices, the company saw record production at AWAC’s tier 1 low cost refineries which enabled it to deliver strong margins and returns. The company is planning to hold its Annual General Meeting on 20 May 2020 at the offices of Deloitte, 550 Bourke Street, Melbourne, Victoria.

.png)

Key Financials (Source: Company Reports)

Consistent Source of Strong Dividends:Due to the company’s low leverage and improved joint venture position, AWC was able to deliver healthy level of dividends to its shareholders. For the second of FY19, the company declared a fully franked final dividend of 3.6 US cents per share, bringing the full year dividend to 8.0 US cents per share. Notably, AWC has been a consistent source of strong dividends over the last 3 years and since 2017 it has delivered an average yield for shareholders of 8.6 per cent per annum, not including franking.

What to expect:Going forward, the demand for Aluminium is expected to grow in near-term as trade friction subsides. The financial results of Alumina Limited are dependent upon AWAC’s operational performance and profitability. In FY20, AWAC is expected to produce around 12.7 million tonnes of alumina and approximately 162,000 tonnes of aluminium. It is expected that in FY20, total receipts by Alumina Limited will exceed its corporate needs.

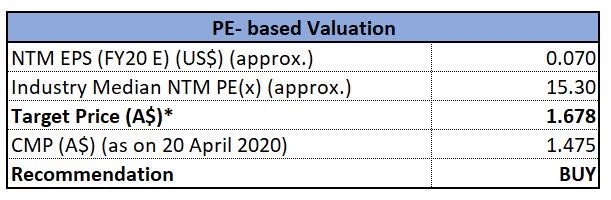

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters), *1USD = 1.567 AUD as at 20 April 2020

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the last three months, the stock of AWC has corrected by 31.22% and is currently trading near its 52-week low of $1.295, offering a decent opportunity for accumulation. We have valued the stock using P/E multiple based illustrative relative valuation method, and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like South32 Ltd (ASX: S32), BlueScope Steel Ltd (ASX: BSL) and OZ Minerals Ltd (ASX: OZL). Considering the company’s decent FY19 performance, consistency in paying dividends, and current trading levels, we are giving a “Buy” recommendation to the stock at a market price of $1.475, down by 6.349% on 20 April 2020.

Buru Energy Limited

March Quarter Highlights:Buru Energy Limited (ASX: BRU) is an oil and gas exploration and production company with a diverse portfolio of exploration assets. On 20 April 2020, the company released its March 2020 Quarter report, wherein it assured that it has appropriately responded to the recent oil price collapse and Covid-19 situation with significantly reduced operating and corporate costs. From its Ungani Oilfield, the company reported total production of ~88,000 bbls (gross) for the March quarter.

Exploration Progress at Canning Basin:The company is currently conducting a detailed regional technical review at the exploration permits at Canning Basin. Till now, the review has identified various new exploration play areas with potential for large scale conventional oil discoveries. A farmout process is currently underway focused on incorporating the results of the review and new play types.

Cash Position:The company currently has a strong balance sheet with ~$30.1 million in cash and cash equivalents as at 31 March 2020. During the March quarter, BRU spent $2.7 million on development activities and $2.4million on exploration activities.

.png)

Cash Position (Source: Company Reports)

Stock Recommendation: The company has a current ratio of 3.61x, higher than the industry median of 1.11x, demonstrating that the company is well positioned to pay its short-term obligations. In the last three months, the stock of BRU has corrected by 49.09% and is currently trading near to its 52-week low of $0.062. The stock is trading at a price to book multiple of 0.5x, as compared to the industry average (Energy) of 1.1x on TTM basis. Considering the aforesaid facts, the company’s liquidity position, current trading levels, and decent performance in March quarter, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.087, up by 3.571% on 20 April 2020.

Leigh Creek Energy Limited

Tackling Covid-19 Impacts:Leigh Creek Energy Limited (ASX: LCK) is an energy and minerals explorer, focussed on developing its Leigh Creek Energy Project (LCEP), in northern South Australia. In response to Covid-19, the company has implemented a range of actions to preserve shareholder funds, whilst maintaining the positive business progress that has been achieved over the last year. After reviewing all elements of expenditure, the company has introduced a range of cost saving measures, which has put the organisation in a strong position for the remainder of 2020.

Joint Venture for InSitu Gasification operations in China:Recently, Leigh Creek Energy Limited and China New Energy Group Limited signed a binding term sheet for their proposed Joint Venture for InSitu Gasification operations in China. It is expected that this JV will provide LCK access to the Chinese market, with a trusted partner and access to significant revenue stream.

H1FY20 Highlights:In the first half of FY20, the company reported an operating loss of $3.19 million, lower than the loss reported in pcp. During the period, the company confirmed the receipt of a Research and Development Tax Incentive cash rebate from the Australian Taxation Office of $6.39 million. The net cash provided by operating activities stood at $2.936 million. At the end of H1FY20, the company had a cash balance of $3.88 million.

.png)

Cash Flow from Operating Activities Source: Company Reports)

Stock Recommendation: LCK has a current ratio of 4.45x, as compared to the industry median of 1.05x. In the last six months, the stock of LCK has corrected by 52.2% and is trading close to its 52 weeks low price of $0.087, offering a decent opportunity for accumulation. Considering the recently signed binding agreement for the proposed Joint Venture for InSitu Gasification operations, the company’s recently implemented measures to preserve shareholder funds amid Covid-19 crisis, and its current trading levels, we give a “speculative buy” recommendation on the stock at the market price of $0.130, up by 32.653% on 20 April 2020, owing to the news related to the signing of the binding agreement for the proposed Joint Venture for InSitu Gasification operations.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...