.png)

Stocks’ Details

Centuria Office REIT

COF Secures Debt Facility: Centuria Office REIT (ASX: COF) is engaged in owning a portfolio of high-quality office assets throughout Australia. In a recent update, the company stated that it has secured a further seven-year debt facility from Crédit Agricole, which, in turn, will increase its debt maturity to 3.7 years from 3.4 years as at April 2020.Additionally, the company increased its diversified number of debt lenders to five and undrawn debt facility to $131.5 million. The latest debt facility offers enhanced flexibility to the company’s balance sheet, thereby strengthening its liquidity position.

Q3FY20 Business Update: The company has taken necessary steps to curb the impact of COVID-19 outbreak, with utmost attention towards the safety and well-being of its tenant base, and the community. Although, the impact from COVID-19 remains unclear, the company is well positioned with robust capital and quality office portfolio. The company recently updated its 3QFY20 fund position, wherein the company’snational portfolio comprises 23 high-quality office assets, with 99% occupancy of its portfolio with a WALE of 4.9 years. Notably, more than 60% of its portfolio leases expire at or beyond 30 June 2024. The company’s 25% of portfolio income is derived from government tenants, whereas the remaining 75% of total portfolio income is derived from government, listed or multinational corporations.

COF to Take Over Augusta: The company had inked a deal to acquire Augusta Capital Limited (Augusta), one of New Zealand’s largest listed real estate funds management companies, for a consideration of NZ$180 million. The takeover bid is subject to closing customary condition and approval from the Overseas Investment Office in relation to sensitive lands regulations. Notably in 1HFY20, the company’s Assets Under Management expanded to $7.3 billion.

.png)

AUM Highlight (Source: Company Report)

Withdrawal of FY20 Outlook:Due to the escalated tension caused by COVID-19 related disruptions, COF found it prudent to withdraw its FY20 FFO guidance. Nonetheless, FY20 distribution outlook of 17.8 cents per unit will remain, subject to any changes in situations.

Valuation Methodology:P/E Multiple Based Relative Valuation (Illustrative)

.png)

P/E Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per the ASX, the stock is trading below the average of its 52-week low and high of $1.375 and $3.3. As on 19 May 2020, the company’s market capitalisation stands at ~$936.43 million, with an annual dividend yield of 9.73%. The stock of the company gave negative returns of 43.83% over a period of three months.In 1HFY20, the company’s EBITDA and operating margins stood at 69% and 68.6%, respectively. We have valued the stock using a P/E multiple based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers such as Aventus Group (ASX: AVN), Charter Hall Retail REIT (ASX: CQR), and Vicinity Centres (ASX: VCX), to name few. Thus, considering a favourable valuation, recent takeover bid, higher recurring revenue, and improvement in key margins, we give a “Buy” recommendation on the stock at the current market price of $1.875 per share, up 3.022% on 19 May 2020.

Lifestyle Communities Limited

LIC to Buy a New Site: Lifestyle Communities Limited (ASX: LIC) is engaged in developing, owning, and managing reasonable residential land lease communities. On 13 May 2020, the company announced that it has implemented a contract to acquire a new site situated in Clyde North, Victoria. The final settlement is likely to take place in mid-2021 with construction expected to commence thereafter. Due to this contract, the company’s portfolio will rise to 4,288 home sites, consisting of sites in planning, development or under management.

COVID-19 Update: The company has taken necessary steps to curb the impact of COVID-19 outbreak, by ensuring safety and wellbeing of its team, homeowners, and communities. On 20 March 2020, the company had settled 144 homes. Further, it has an additional 81 long-established settlement bookings prior to 30 June 2020. The company remains on track to complete a total of 342 homes prior to 30 June 2020, subject to construction activity. The Company’s balance sheet and debt position remains strong, with more than $90 million in cash balance. It has no debt facilities maturing in the coming one year.

1HFY20 Operating Highlights for the Period Ended 31 December 2019: During the period, the company reported total home settlement revenue of ~$40 million, down 36.4% year over year. Total management and other revenue amounted to $15.3 million as compared to $12.5 million in 1HFY19. Net profit after tax came in at $15.1 million, down 31.1% in comparison to $21.9 million in the previous corresponding year. The decrease was on the back of lower number of settlements relative to the prior comparative period. Revenue from site rentals stood at $11.4 million, up 25.6% year over year, on the heels of higher number of homes under management and a rental surge of 3.5% Cost of sales included $9.3 million for a share of the community infrastructure sold with each home.

.png)

Key Financial Highlights (Source: Company Report)

Stock Recommendation: The stock of the company is trading at $8.31 with a market capitalisation of ~$858.32 million. At the current market price of $8.31, the stock is available at a price to earnings (P/E) multiple of 17.77x, which is higher than the industry median of 9.8x. Enterprise Value (EV) to Sales multiple of the company stands at 8.1x on TTM basis as compared to the industry median of 4.7x. It reported a higher EV/EBITDA multiple of 15.9x against the industry median of 11.3x indicating that the stock is overvalued. The stock has corrected 8.68% and 2.84% in the last three months and six-months, respectively. At the current market price, the stock is trading near the upper band of its 52-week trading range of $4.530 to $9.87. Due to the high level of uncertainty caused by COVID-19 outbreak, the company has suspended its FY20 and all forward looking outlook. Considering the aforesaid facts, price movements, current trading levels and valuations, we recommend an “Expensive” rating on the stock at the current market price of $8.31, up 1.218% as on 19 May 2020.

Aspen Group Limited

Business Update: Aspen Group Limited (ASX: APZ) is engaged in owning, operating, and developing high-quality accommodation at reasonable prices in the residential, retirement and short stay sectors space. On 18 May 2020, the company informed the market that it has continued with productivity amid COVID-19 outbreak. The company also stated that it has not seen any rise in arrears due to COVID-19 impact. Notably, more than 50% of its tourist cabins are now engaged at an average rent of $243 per week, aided by customers who are willing to stay for a long period of time.

Latest Acquisition Details: Recently, the company entered a contract to purchase a partially completed build-to-rent development at Burleigh Heads, Queensland under a mortgagee in possession sale. This residential community incorporates 18 large townhouses that are appropriate for families and co-living. The purchase price stands at $3.15 million, along with certain amount of GST. The settlement for this contract is expected to occur in a few months post the completion of subdivision. The company expects net rental yield on cost to be ~4.5-5.0% upon completion and letting out. The latest move is likely to enhance Aspen’s business and portfolio.

1HFY20 Key Highlights for the Period Ended 31 December 2019: During the period, the company reported total operating revenue of ~$15.1 million, up 11% year over year. Total development profit amounted to $414K in 1HFY20. EBITDA came in at $4.36 million, up a whopping 55% in comparison to $2.8 million in the previous corresponding year.

.png)

Key Financial Highlights (Source: Company Reports)

COVID-19 Impact & Outlook: Despite the challenging economic conditions due to COVID-19 led crisis, the company reinstated FY20 underlying earnings and distribution outlook to be in the range of 6.75-7.00 cents per share and 6.00 cents per share, respectively. The company remains on track to invest in the upkeep of the properties and has reduced its corporate overheads.

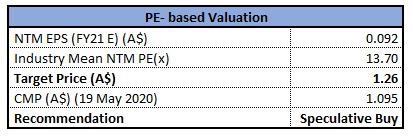

Valuation Methodology:P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading on the upper band of its 52-week low and high level of $0.8 and $1.24, respectively. As on 19 May 2020, the company’s market capitalisation stood at ~ $99.21 million, with an annual dividend yield of 5.29%. The stock of the company gave negative returns of 11.21% over a period of three months. We have valued the stock using a P/E based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). Thus, considering the above factors, current trading levels, favourable valuation, recent takeover bid, higher operating revenue, and positive outlook, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.095 per share, up 6.311% on 19 May 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...