.png)

Stocks’ Details

Seven Group Holdings Limited

Decent Growth in Top line: Seven Group Holdings Limited (ASX: SVW) is an operating and investment group; with interests in heavy equipment sales and service, equipment hires, media, broadcasting, and energy assets. The market capitalisation of the company stood at $5.99 billion as on 19th June 2020. The company recently stated that its businesses are well-positioned to support customer investment, with robust demand for domestic energy. On its WesTrac business, the company experienced a minimal impact from COVID-19 outbreak. During 1H FY20, its trading revenue went up by 12% to $2.3 billion, and underlying net profit after tax amounted to $255.7 million, indicating a rise of 3% over pcp. These results reflected the strength of the Industrial Services businesses, supported by strong demand from the mining and infrastructure sector.

.png)

Key Summary (Source: Company Reports)

Suspension of Guidance: Previously, the company has suspended its market guidance for FY20 due to the uncertainty around trading conditions relating to the impact of COVID-19.

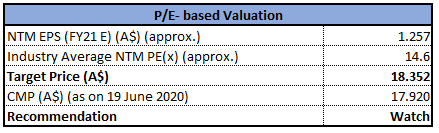

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk:The company’s business is likely to be impacted by the results of the significant escalation measures taken by Governments to curb the impact of COVID-19 infection. Moreover, SVW is sensitive to various risk factors that may impact the company’s future performance such as commodity price risk, which arises due to the volatility in the prices of oil and natural gas.

Stock Recommendation: Current ratio of the company stood at 2.14x in 1H FY20 as compared to the industry median of 1.34x. This indicates that the company is in a decent position to address its short-term obligations. The stock has moved up by 25.02% and 51.03% during the span of one month and three months, respectively. Currently, the stock is inclined towards its 52-week high of $21.960. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with limited upside (in percentage terms). Hence, considering the aforesaid facts, current trading levels and valuation, we have a watch stance on the stock at the current market price of $17.920 per share, up by 1.587% on 19th June 2020.

Atlas Arteria

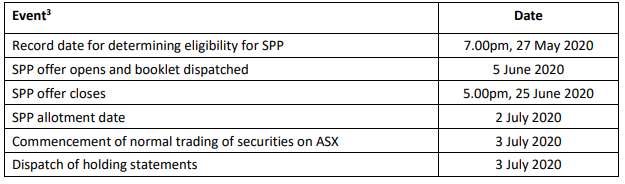

Opening of Share Purchase Plan:Atlas Arteria (ASX: ALX) is an operator and manager of a portfolio of toll-road assets. The market capitalisation of the company stood at $6.43 Bn as on 19th June 2020. Recently, the company has opened its share purchase plan to raise up to A$75 million. The SPP followed a successful institutional placement of $420 million. The company would use the proceed raised from the Placement and SPP for restructuring its balance sheet by repaying the MIBL debt facility, to improve resilience and to provide additional capacity for growth.

Key SPP Dates (Source: Company Reports)

1QFY20 Key Highlights:During Q1 FY20, the company reported a fall of 6.8% in toll revenue over pcp and weighted average traffic went down by 8.8% compared to the prior corresponding period, reflecting the global impacts of Government policy responses to the COVID-19 pandemic.

Growth Opportunities: The company is well placed to navigate the COVID-19 pandemic with strong liquidity and improved flexibility to pursue future growth opportunities following the repayment of the MIBL Facility. Going forward, the company remains optimistic about its future growth prospects.

Key Risk: As of the now, the risk with the company involves the impact of COVID-19, which left an adverse effect on its financial performance and position.

Stock Recommendation: Current ratio of the company stood at 15.2x in FY19 as compared to the industry median of 1.16x. This indicates that the company is in a decent position to pay its short-term obligations as compared to the peer group. The stock of ALX has delivered a return of 10.23% within last one month. The stock of ALX is trading at a price to book value multiple of 1.9x as compared to the industry median (Transport Infrastructure) of 2.1x on TTM basis. Thus, considering the decent liquidity position, recent equity raising and future opportunities, we give a “Hold” recommendation on the stock at the current market price of $7.00 per share, up by 3.093% on 19th June 2020.

Primero Group Limited

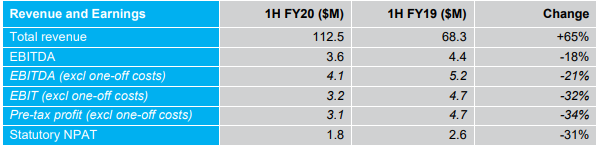

PGX Awarded Contract Extension:Primero Group Limited (ASX: PGX) is an engineering contract company. The market capitalisation of the company stood at $42.19 Mn as on 19th June 2020. Recently, the company announced that it has been awarded a material contract extension to the existing Koodaideri Non-Process Infrastructure (NPI) contract presented in late 2019, for the construction of the Koodaideri Airport Terminal and Infrastructure. The total contract value now stands at around $150 million. In another update, the company stated that major project works are underway and progressing well. PGX’s business growth activities are steady with ongoing awards of sustaining capital works, minerals processing feasibility works and Early Contractor Involvement (ECI) engagements. The below picture gives an overview of key financials for 1H FY20:

Key Financials (Source: Company Reports)

Addition in Order Book: The company continues to operate at a run-rate consistent with its FY20 contracted order book guidance of around $195 million. For FY21, the company’s contracted order book now stands at approximately $220 million with the recent NPI contract addition.

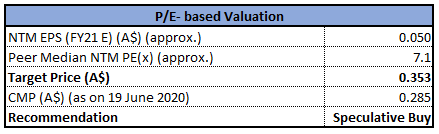

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: The company is exposed to specific and operational risks, which include construction claims and dispute. PGX is also exposed to macro-economic cycles, where weakness in the broader construction and engineering sector and a reduction in growth capital expenditure in major new natural resource projects would impact the company.

Stock Recommendation: The company possesses strong liquidity and a very low level of gearing. As at 8 May 2020, the cash balance of the company stood at $19 million. Debt to equity of the company stood at 0.13x in 1H FY20 against the industry median of 0.54x. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of low-double-digit (in percentage terms).For the purpose, we have taken peers such as Acrow Formwork and Construction Services Ltd (ASX: ACF), SRG Global Ltd (ASX: SRG) and Austin Engineering Ltd (ASX: ANG).

Thus, in light of the strong liquidity, deleveraged balance sheet, the increased order book for FY21 and key risk associated with macro-economic factors, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.285 per share, up by 16.327% on 19th June 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...