Stocks’ Details

Wisr Limited

Delivered a Loan Growth of 36% QoQ:Wisr Limited (ASX: WZR) provides a unique financial wellness eco-system supported by consumer finance products which result in better outcomes for borrowers, investors and general citizens. Recently, the company announced regarding a change in a Director’s interest wherein, John Nantes has acquired 1,920,000 ordinary shares, on disposal of Performance Rights.

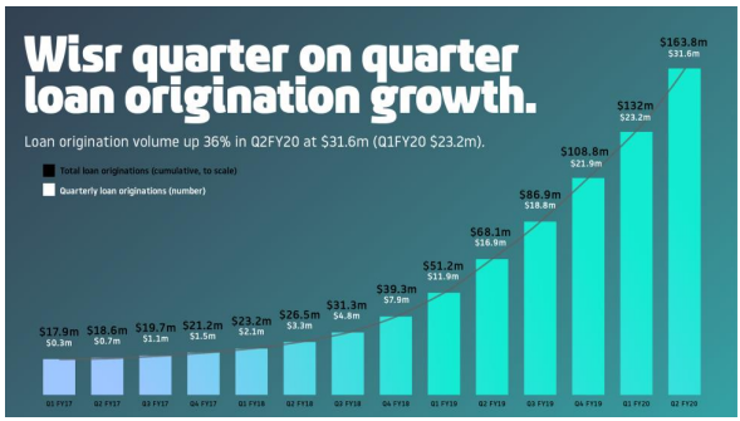

Key Operating Highlights for the Period ended 31st December 2019: WZR announced its quarterly highlights, wherein the company added $31.6 million of new loans, witnessing 36% q-o-q growth. Total loan originations stood at $163.8 million as on 31st December 2019. During the quarter, the business witnessed addition of 120,000 customers into the Wisr Ecosystem. Since the launch of Wisr App, the business witnessed more than 54,000 app downloads, who paid ~$365,000 worth of debt. The company confirms the reappointment of Anthony Nantes for the role of Chief Executive Officer (CEO), with new contract terms for the coming three-year period. The Business is well capitalised to drive future growth as it raised $33.5 million in January 2020 through placement of ~181 million ordinary shares.

Quarterly Loan Origination data (Source: Company Reports)

Cash Flow Highlights: For the first six months of FY20, the company reported net cash used in operating activities of $1.66 million, net cash used in investing activities of $22.18 million while the company derived $22.04 million from its financing activities. As on 31 December 2019, the company reported a cash balance of $10.19 million.

Stock Recommendation:The stock of WZR is trading at $0.280 with a market capitalization of $247.73 million. The stock made a 52-week low and high of $0.051 to $0.295 and currently, the stock is trading at the upper band of its 52-week trading range. The stock has delivered stellar returns of ~103% and ~112% in the last three months and six months, respectively. The business will utilize its funds in the scaling of its core lending business followed by the development of its Wisr Ecosystem. The company will prioritise on recruiting the best talents to aid improved business prospects in the coming months. Considering the recent price movements, trading levels with decent loan growth, we have a watch stance on the stock at the current market price of $0.28, up 5.66% as on 04 February 2020.

ELMO Software Limited

Reported Statutory Revenue Growth of 33.9%:ELMO Software Limited (ASX: ELO) offers a unified cloud-based platform of HR & Payroll software which is used for payroll management and rostering / time & attendance.

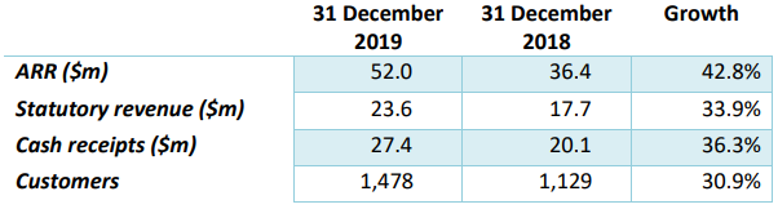

H1FY20 Key Highlights for the Period ended 31 December 2019: ELMO came up with its six-months operating highlights, wherein the company posted statutory revenue of $23.6 million, depicting an increase of 33.9% from H1FY19. During the period, the company reported record cash receipts of $27.4 million on account of 30.9% uplift in active customers. During the second quarter of FY20, the company reported cash receipts of $15.4 million, depicting a growth of 57.2% on y-o-y basis. During the last twelve months, the business reported a cash collection of $52.4 million, up 40.6% on pcp. The company reported annualised recurring revenue (ARR) of $52 million as on 31st December 2019, up 42.8% on pcp. The business reported a closing cash balance of $78.2 million as on 31st December 2019, including $15 million received from the Share Purchase Plan (SPP) during October 2019.

Operational Highlights (Source: Company Reports)

Stock Recommendation:The stock of ELO is trading at $7.20 with a market capitalization of $522.27 million. The stock made a 52-week low and high of $4.450 to $7.740 and currently, the stock is trading at the upper band of its 52-week trading range. The stock has delivered mixed returns of 7.23% and -1.97% in the last three months and six months, respectively. The business witnessed acquisition of new customers coupled with cross-sell to ELMO’s existing customer base. The business foresees H2FY20 with a strong sales pipeline and a drastically improved prospect for long-term sustainable growth. Considering the recent price movements, current trading levels with decent customer growth, we give a “Hold” rating on the stock at the current market price of $7.20, up 3.3% as on 04 February 2020.

Temple & Webster Group Limited

Trade and Commercial Segment Reported a Growth of 75% y-o-y: Temple & Webster Group Limited (ASX: TPW) is an e-commerce company that operates in the furniture and homewares market across Australia.

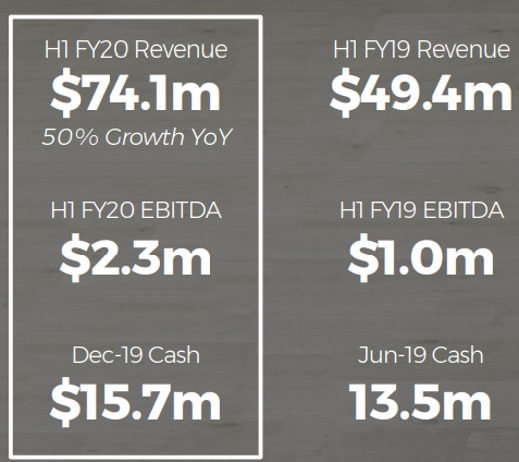

H1FY20 Operating Highlights for the Period ended 31 December 2019: TPW announced its half-yearly results, wherein the company reported revenue of $74.1 million, up 50% on y-o-y basis. Growth was majorly driven by 45% y-o-y growth in active customers. The company reported active customers of 330,000 for the last twelve months. EBITDA for the half stood at $2.3 million, as compared to $1 million in the prior corresponding period. The business reported 75% y-o-y growth in the trade and commercial segment. The quarter was marked by the launch of first beta mobile app followed by the establishment of a data team, to support personalization, customer acquisition, etc.

H1FY20 Financial Highlights (Source: Company Reports)

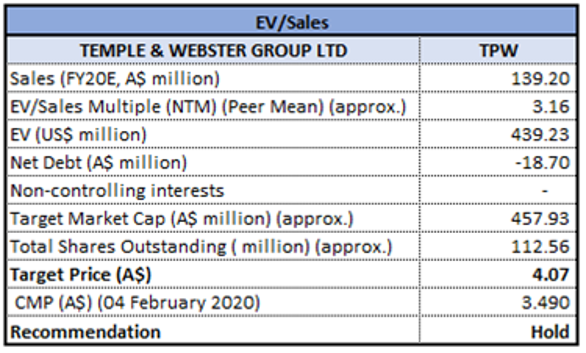

Valuation Methodology: Enterprise Value to Sales based Approach

Enterprise Value to Sales based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The stock of TPW is trading at $3.490 with a market capitalization of $320.99 million. 52-week low and high for the stock stands at $1.240 - $3.54 and currently, the stock is trading at the upper band of its 52-week trading range. The stock has delivered returns of 29.82% and 69.46% in the last three months and six months, respectively. Within Australia, the furniture & homewares market is estimated at ~$13.9 billion. The business is committed to its high growth strategy to take advantage from the growing online segment. In the coming quarters, the business will invest in short-term growth initiatives such as Technology & Data, Mobile App, Trade & Commercial, Private Label and Logistics, etc. Considering the recent price movements, trading levels with decent customer growth, we have valued the stock using Enterprise Value to Sales based relative valuation method. We have taken peers like Jumbo Interactive Ltd (ASX: JIN), Redbubble Ltd (ASX: RBL) and AP Eagers Ltd (ASX: APE) and arrived at a target price with lower double-digit upside (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $3.49, up 23.32% on account of robust 1HFY20 numbers as on 04 February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...