.png)

Stocks’ Details

Nib Holdings Limited

Approval Received for 2020 Premium Changes: Nib Holdings Limited (ASX: NHF) is a private health insurer whereby it underwrites and distributes private health insurance to Australian and New Zealand residents as well as international students and visitors to Australia. As on 30 January 2020, the market capitalization of the company stood at $2.47 billion. NHF will announce its FY20 interim results on 24 February 2020. The company has recently announced that it has received approval from the Federal Minister to increase insurance cover premiums for the health funds by an average of 2.90% across all products, effective from 1 April 2020.

Decent Increase in NPAT: During FY19, total group revenue of the company went up by 8.3% to $2.4 billion, and NPAT witnessed an increase of 11.8% and stood at $149.3 million. Owing to the decent financial performance of the company, the Board paid full year dividends of 23 cents per share.

.png)

FY19 Financial Performance (Source: Company Reports)

What to Expect: The company has indicated that FY20 Group underlying operating profit is expected to be at least $170 million, mainly due to an increase in claims expense across several underwriting business lines. NIB also expects to deliver a net margin of approximately 6%. FY20 risk equalisation net contribution is expected to increase by 9% and be around $250 million.

Valuation Methodology: Price/Book Based Valuation

.png)

Price/Book Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of NHF is trading very close to its 52-week low of $5.125, proffering a decent opportunity for accumulation. Over the span of 4 years, the company witnessed a CAGR of 10.08% in total revenue. Considering the trading levels, CAGR in total revenue and decent outlook, we have valued the stock using Price/Book based relative valuation method and arrived at a target upside of lower double-digit (in percentage terms). For the said purposes, we have considered Insurance Australia Group Ltd (ASX: IAG), Steadfast Group Ltd (ASX: SDF) and Platinum Asset Management Ltd (ASX: PTM) as peers.Hence, we recommend a “Buy” rating on the stock at the current market price of $5.390, down by 0.37% on 30 January 2020.

Collection House Limited

Decent Rise in EBIT: Collection House Limited (ASX: CLH) provides debt collection services and purchase of consumer debt. As on 30 January 2020, the market capitalization of the company stood at$149.05 million. In the recently held AGM, the top management stated that revenue of the company went up by 12% on FY18 and stood at $161.1 million. This was mainly due to the second transaction with Balbec Capital LP, PDL growth and a positive revenue recognition change under AASB 9. During FY19, Earnings Before Interest & Tax went up by 18% to $51.3 million from $43.4 million in FY18. The decent financial performance enabled the Board to declare fully franked dividends of 8.2 cents per share.

.png)

FY19 Financial Performance (Source: Company Reports)

What to Expect: The company expects a positive outlook in FY20 owing to its growth in market share in Australia and New Zealand through the acquisition of debt portfolios. The company has provided cash collection guidance for the PDL segment and expects it to be in the range of $145 million to $155 million, including the PDL purchases of $80 million to $100 million in FY20. The company expects its statutory EPS to be between 23 cents per share to 24 cents per share.

Stock Recommendation: As per ASX, the stock of CLH is trading very close to its 52-week low of $1.030, proffering a decent opportunity for accumulation. Over the span of 4 years, the company witnessed a CAGR of 6.34% in revenue and a CAGR of 5.39% in gross profit. During FY19, net margin of the company witnessed a slight improvement over the previous year and stood at 19.1%, up from 18.2% in FY18. In the same time span, ROE of the company was 14.1%, up from 13.2% in FY18. On the TTM basis, the stock is trading at a P/E multiple of 4.710x, lower than the industry median (Industrials) of 10.9x. The stock is also trading at EV/Sales multiple of 0.9x, lower than the industry median (Industrials) of 1.6x. Considering the trading levels, CAGR in revenue and gross profit and improvement in ROE, we recommend a “Buy” rating on the stock at the current market price of $1.065, up by 1.429% on 30 January 2020.

Suncorp Group Limited

Natural Hazard Update: Suncorp Group Limited (ASX: SUN) provides banking, insurance, wealth and other financial solutions to the retail, corporate and commercial sectors. As on 30 January 2020, the market capitalization of the company stood at $16.29 billion. The company has recently provided an update on natural hazard costs and has stated that it has received over 25,000 claims in relation to the hailstorms and over 1,400 claims in relation to the heavy rain. SUN has declared three natural hazard events since the start of 2H20, but the reinsurance protection provides confidence that FY20 net natural hazard costs should remain within the natural hazard allowance of $820 million.

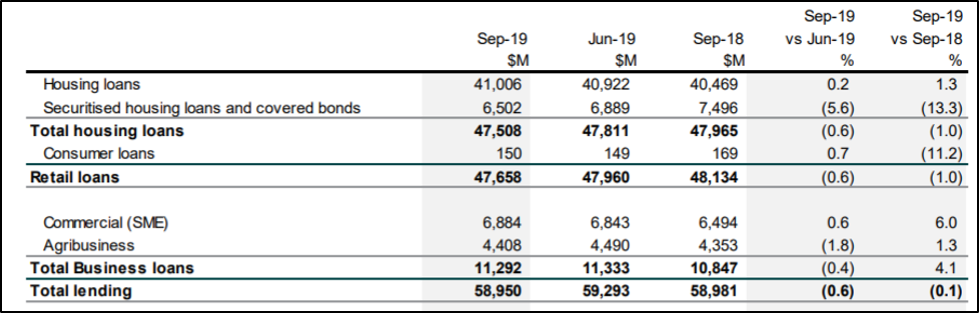

Suncorp Closes Capital Notes 3 Offer: The company has completed the Capital Notes 3 offer and has raised $389 million through the issue of 3,890,000 Capital Notes 3 for $100 each. In the quarterly update for September 2019, the company stated that growth in commercial lending was offset by a contraction in the retail and agribusiness portfolios and total lending contracted by 0.6%. In the same time span, Net Stable Funding Ratio was 115.1%, and the Bank’s capital position was strong with a Common Equity Tier 1 ratio of 9.31%.

Loans and Advances (Source: Company Reports)

Growth Opportunities: The company’s expectations of 1H20 natural hazard costs remain unchanged at $519 million. It also expects the reserve releases for 1H20 to be in between $50 million to $70 million. SUN anticipates that there will be ongoing competitive pressure for home loan refinancing options during the second half of FY20.

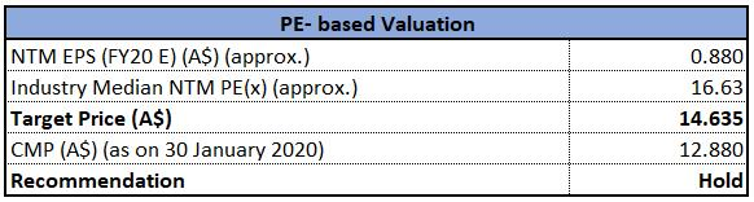

Valuation Methodology: Price to Earnings based Valuation

Price to Earnings based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of SUN is trading very close to its 52-week low of $12.575. During FY19, premiums earned ratio of the company stood at 10.9%, higher than the industry median of 9.8%. Considering the trading levels, decent growth opportunities and strong capital position, we have valued the stock using price to earnings based relative valuation method and arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $12.880, down by 0.31% on 30 January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...