National Australia Bank

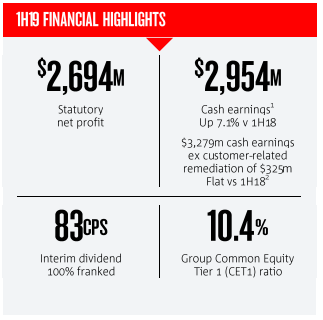

Understanding 1H FY 2019 Results: National Australia Bank (ASX: NAB) had stated that 1H FY 2019 was a challenging period and the Royal Commission indicated the need to take actions in order to earn back the trust of the customers and community. The earnings for 1H FY 2019 included a further $525 million in the customer-related remediation costs. The bank stated that productivity benefits from the transformation program helped in reducing the expenses by 2% as compared to 2H FY 2018 and NAB is on track to deliver the broadly flat costs in FY 2019 and FY 2020 (excluding the large notable expenses).

1H FY 2019 Financial Highlights (Source: Company Reports)

The bank stated that the dividend reduction helped in improving capital generation. The bank’s dividend got reduced by 16% amidst the tough operating environment as well as in order to improve the capital generation. However, the bank also stated that there is potential to grow the dividend in the medium term. Also, the bank’s asset quality was broadly stable, and its transformation savings are on track.

What To Expect From NAB: The bank had stated that the productivity benefits would be the primary driver of the underlying profit growth and its capital settings provide greater flexibility which helps in accommodating the potential earnings volatility as well as regulatory change. Also, the balance sheet strength happens to be a priority for the bank.

Stock Recommendation: The stock of NAB had delivered the return of 1.70% in the span of six months and, on the YTD basis, the return stood at 9.10% which can be considered at decent levels considering the challenging operating environment. Also, National Australia Bank had stated that they are having robust capital position and they are well-positioned to surpass APRA’s “unquestionably strong capital” benchmark by the month of January 2020. Hence, considering the decent fundamentals, we maintain our “Buy” recommendation on the stock at the current market price of A$25.700 per share (down 0.31% on 2 May 2019).

Magellan Financial Group Limited

Rise in Total FUM: Magellan Financial Group Limited (ASX: MFG) had released the funds under management (or FUM) update and stated that its total FUM amounted to A$79,442 million at the end of March 29, 2019. However, at the end of February 28, 2019, the company’s FUM stood at A$76,030 million. In the month of March 2019, the company encountered net inflows amounting to $1,177 million which consisted of net retail inflows of $357 million and the net institutional inflows of $820 million.

.png)

FUM Update (Source: Company Reports)

The company had earlier made an announcement that Ms Marcia Venegas had been placed as the Company Secretary of MFG. Magellan Financial Group had also stated that Mr. Geoffrey Stirton had resigned from the post of Company Secretary. The company had earlier made an announcement about the interim results for the period ended December 31, 2018. During the same period, the company’s average funds under management witnessed a rise of 35% and stood at $72.1 billion. However, its adjusted net profit after tax witnessed a rise of 62% and stood at $176.3 million.

What to Expect From MFG: Magellan Financial Group is expected to maintain robust balance sheet in proportion to scale of the business, which includes increased liquidity levels in order to ensure that the business withstands almost any market condition or unforeseen event. The top management of the company had stated that the company’s 1H FY 2019 was supported by the robust investment performance in the volatile market conditions.

Stock Recommendation: The stock of Magellan Financial Group had witnessed the rise of 65.10% in the span of previous six months, while in the time frame of past three months, it encountered the rise of 57.01%. However, on a YTD basis, the stock witnessed the rise of 90.67%. Coming to the stock’s valuations, the company’s P/B ratio stood at 11.94x which is higher than the peer median of 3.73x which reflects that the stock is overvalued at the current juncture. Also, the company’s stock price is trading towards its 52-week higher level. As per ASX, the company is having an annual dividend yield of 3.68%.

Considering the aforesaid parameters, we give a “Sell” rating on the stock at the current market price of A$44.670 per share (up 0.247% on 2 May 2019) and we advise to investors that they should book the profit at the current level and wait for further correction to get the better entry levels.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...