Boral Limited

.png)

BLD Details

Undervalued position at the current juncture: Boral Limited (ASX: BLD) has an engagement in the manufacturing and supply of building and construction materials in Australia, the USA, and Asia. The company recently announced that it has entered into a property development management deed with Mirvac in relation to its Scoresby site in Victoria. Under the agreement, Mirvac will manage the urban development of the 171-hectare site over a multi-decade period, including a proposed new housing community and substantial new parklands.

Boral expects to receive around $66 Mn of EBITDA by FY2026, including $3 Mn in FY2019. Additional significant earnings are projected from the development of Scoresby from FY2027 through to anticipated project completion in 2035. It is expected that Scoresby will be an important earnings contributor for Boral over the next 20 years.

H1FY19 (ended on December 31, 2018) Key Highlights: Total revenue increased by 1.8% to $2,990.3 Mnas compared to $2,937.0 Mn in H1FY18. The net profit attributable to members increased by 36.7% to $236.5 Mn as compared to $173.0 Mn in H1FY18.

.png)

H1FY19 Income Statement (Source: Company Reports)

What to expect: As per the release, it is expected that Boral Australia will deliver broadly similar EBITDA this year as in FY18,excluding property in both years, with property earnings to be around $30 Mn compared to $63 Mn in FY18. Boral North America is expected to deliver EBITDA growth of around 15% in USD in FY19for the continuing operations, reflecting volume growth, further synergy delivery and operational improvements.

USG Boral is expected to deliver slightly lower profits in FY19as compared to FY18. Across most businesses, higher volumes, together with business improvement initiatives, will contribute to an expected second-half skew.

Stock Recommendation: The company’s stock is trading closer to its 52-week low level of $4.400, and therefore, probability to bounce back increases. Its current ratio for H1FY19 stood at 1.84x, which is better than the industry median of 1.38x, which implies the company is in a better position to address its short-term obligations than its peer group. On the valuation front, its EV/Sales and Price/Cash Flow multiple on TTM basis stand at 1.4x and 7.1x, which are lower than the industry median of 1.9x and 8.0x, respectively, indicating undervalued position at the current juncture.

Hence, considering the aforesaid facts and current trading level, we recommend a “Buy” rating on the stock at the current market price of $5.160 (down 8.021% on July 31, 2019).

.png)

BLD Daily Chart (Source: Thomson Reuters)

Premier Investments Limited

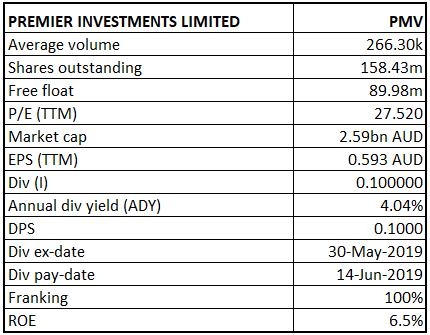

PMV Details

Decent top-line and bottom-line performance in H1FY19 on pcp:Premier Investments Limited (ASX: PMV) operates in several specialty retail fashion chains within the specialty retail fashion markets in Australia, New Zealand, Asia and Europe.

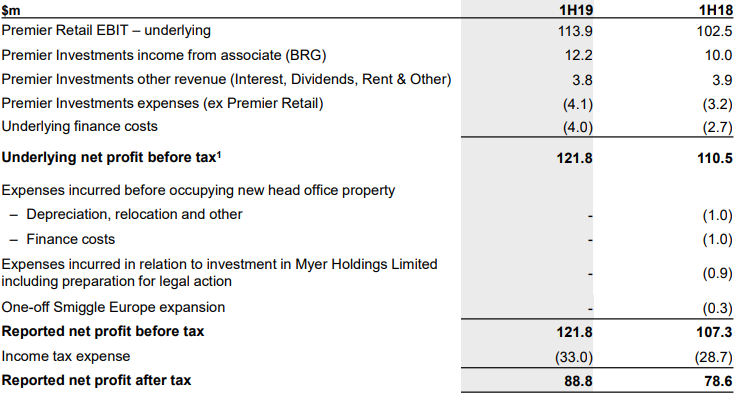

The company in its H1FY19 results, highlighted that NPAT (Net Profit After Tax) increased by 13% on pcp to $88.8 Mn.The premier Retail EBIT increased by 11.1% on pcp to $113.9 Mn. Its sales in the half year period increased by 8% on pcp to $680.2 Mn, which can be attributed to decent increase in LFL sales, apparel brand sales, Online sales, Peter Alexander sales and Smiggle sales. At the end of H1FY19, PMV reported cash on hand at $182.3 Mn.

Investment in associate Breville Group Limited was reported at $238.9 million and investment in Myer Holdings Limited was reported at $34.9 Mn. Due to strong balance sheet and decent performance of Premier Retail, the Board of Directors declared interim ordinary dividend of 33 cents per share fully franked, with record date and payment date on May 31, 2019 and June 14, 2019.

H1FY19 Income Statement (Source: Company Reports)

What to expect: The management added that Peter Alexander’s strategic 2020 Growth Plan of delivering in excess of $250 million in annual sales by FY20 is well ahead of plan. The brand has opened 26 new stores over the past 18 months and therefore remains well ahead of its planned 40 new store openings between FY18 and FY20. Peter Alexander has confirmed four new stores to open in H2FY19.

Stock Recommendation: PMV’s share generated positive YTD return of 13.25%. Its gross margin, EBITDA margin and net margin for H1FY19 stood at 63.1%, 18.9% and 13.0%, better than the industry median of 25.1%, 9.2% and 5.7%, respectively, which implies the decent fundamentals of the company. Its current ratio for H1FY19 stood at 2.49x, better than the industry median of 1.57x, which implies that company is in a better position to address its short-term obligations than its peer group. Hence, considering the aforesaid facts and current trading level, we recommend a “Buy” rating on the stock at the current market price of $15.760 (down 3.491% on July 31, 2019).

.png)

PMV Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...