Coronado Global Resources Inc.

.png)

CRN Details

Robust Growth in Net Income Aided by Operational Efficiencies: Coronado Global Resources Inc. (ASX: CRN) operates in Mining, Quarrying, Oil & Gas Extraction and mining activities. With a market update, the company reported that ASX Settlement will remove the Foreign Ownership Restriction (FOR) United States (U.S.) person tag from the Company’s CDIs with effect from 6th March 2020.

FY19 Operational Highlights for the Period ended 31 December 2019: CRN declared its full-year results, wherein it reported revenue of $2,215.8 million, down 3.5% on y-o-y basis, on account of a weaker metallurgical coal market during H2FY19. The company reported Adjusted EBITDA of $634.2 million, up 5.9% underpinned by lower mining cost per tonne. The company reported net income after tax of $305.5 million, up 80.9% on y-o-y basis. The company reported ROM production of 30.8 Mt, exhibiting a growth of 0.2%. The period was marked by 6.4% improvement in dragline efficiency at Curragh during FY19, on top of the 8.1% improvement in FY18. Sales volumes came in at 19.9 Mt, which is slightly lower than FY18 on account of the increased inventory at US operations. During the period, the company successfully commenced three new mining sources resulted in an increase in the metallurgical coal production. The company reported metallurgical pricing of $128.8 per tonne, down 3.4% compared to FY18, due to soft market conditions.

.png)

Key Business Highlights for FY19 (Source: Company Reports)

The Board of Directors declared a fully franked dividend of $0.025 per ordinary share with a payment date of 31st March 2020 and ex-date of 9 March 2020.

Valuation Methodology: Price to Cash Flow Based Relative Valuation

.JPG)

Price to CF based relative valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of CRN is trading at $1.69 with a market capitalization of ~$1.56 billion. The stock made a 52-week low and high of $1.535 and $3.163 and is currently trading at the lower band of its 52-week trading range. The stock has delivered negative returns of 19.5% and 37.35% in the last three months and six-months, respectively. The company reportedsuccessful eecution of the New Coal Supply Agreement with Stanwell Corporation which completes the acquisition of Stanwell Reserved Area. Considering the aforesaid facts, current trading levels and business prospects, we have valued the stock using price to cash flow based relative valuation method and arrived at a target price of higher single-digit upside (in % terms). Hence, we give a ‘Speculative Buy’ on the stock at the closing price of $1.69, up 4.969% as on 02nd March 2020.

CRN Daily Technical Chart (Source: Thomson Reuters)

OceanaGold Corporation

.png)

OGC Details

FY20 AISC expected Between US$1,075 oz to US$1,125oz: OceanaGold Corporation (ASX: OGC) is engaged in operating, processing and exploration of gold and other minerals. Recently, OGC has signed a forward gold sale arrangement with the support of members of the Company’s current banking group to deliver 48,000 ounces of gold between September and December 2020. Under this, it will receive a pre-payment of $78.5 million (approximately $1,635 per ounce) on February 28, 2020.

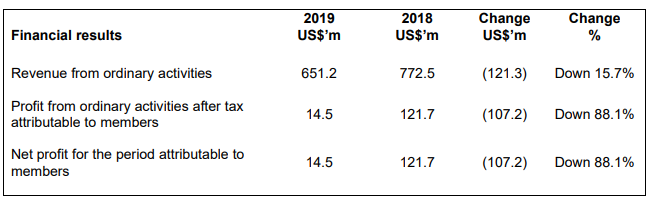

FY19 Financial Highlights for the Period ended 31 December 2019: OGC declared its full-year results, wherein it reported revenue from ordinary activities of US$651.2 million, down 15.7% on y-o-y basis, due to due to zero sales from Didipio plant, during the second half, which partially offset by a 7% higher average gold price from FY18 and increased sales volumes from Haile. The company reported consolidated production of 470,601 ounces of gold and 10,255 tonnes of copper. The business reported all-in sustaining costs (“AISC”) of US$1,061 per ounce. The company reported net profit of US$14.5 million, down 88.1% due to the combination of lower revenue, higher operating costs and higher non-production costs. During the second half, the company reported an unrealised loss of $12.5 million on the fair value of undesignated gold hedges.

Key Income Statement Highlights (Source: Company Reports)

Guidance: FY20, the company expects cash costs of $675 per oz to $725 per oz sold while all-in sustaining costs (AISC) are expected at US$1,075 per oz to US$1,125 per oz sold.

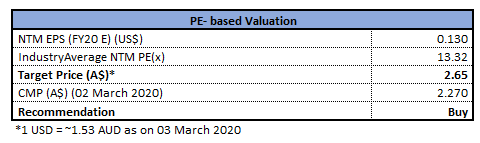

Valuation Methodology: Price to Earnings Based Relative Valuation

Price to Earnings Based Relative Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of OGC is trading at $2.27 with a market capitalization of ~$1.56 billion. The stock made a 52-week low and high of $2.18 and $4.81 and is currently trading at the lower band of its 52-week trading range. The stock has delivered negative returns of 11.03% and 29.58% in the last three months and six-months, respectively. The business is working on Martha Underground project and expects its first production to commence in the second quarter of FY21.Considering the aforesaid facts, current trading levels and business prospects, we have valued the stock using a relative valuation method, i.e., price to earnings multiple and arrived at a target price of lower double-digit upside (in % terms). Hence, we give a ‘Buy’ rating on the stock at the market price of $2.27, down 9.2% as on 02nd March 2020.

%20(1).png)

OGC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...