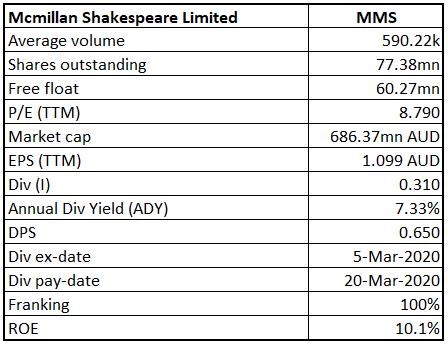

Mcmillan Shakespeare Limited

MMS Details

Acquiring 25% interest in Plan Partners: Mcmillan Shakespeare Limited (ASX: MMS) is a leading provider of salary packaging, novated leasing, asset management and related financial products and services. The company has recently reached an agreement to acquire its joint venture partner’s 25% interest in Plan Partners for $8 million. Following this, the company will wholly own Plan Partners. The transaction is expected to complete on or around 30 June 2020 and it will be funded from existing cash reserves. It is worth noting that Plan Partners has not experienced any disruption to its business because of the COVID-19 containment measures.

Business Update: In a recent business update provided on 29 June 2020, the company informed that its salary packaging business has been largely unaffected by the COVID-19 containment measures, however, its new asset financing in Australia and New Zealand remained subdued. The company has now decided to restructure its UK operations and will focus more on off-balance sheet originations and fleet management. The company expects its FY20 statutory profit after tax to be impacted by around £8-10 million due to the write-down of intangibles and restructuring costs. Further, the company’s statutory profit after tax from Retail Financial Services is expected to be reduced by an intangible impairment of approximately $30-$35 million.The company’s underlying net profit after tax for FY20 is expected to be between $69-$72 million. MMS’s FY20 results are scheduled to release on 19 August 2020.

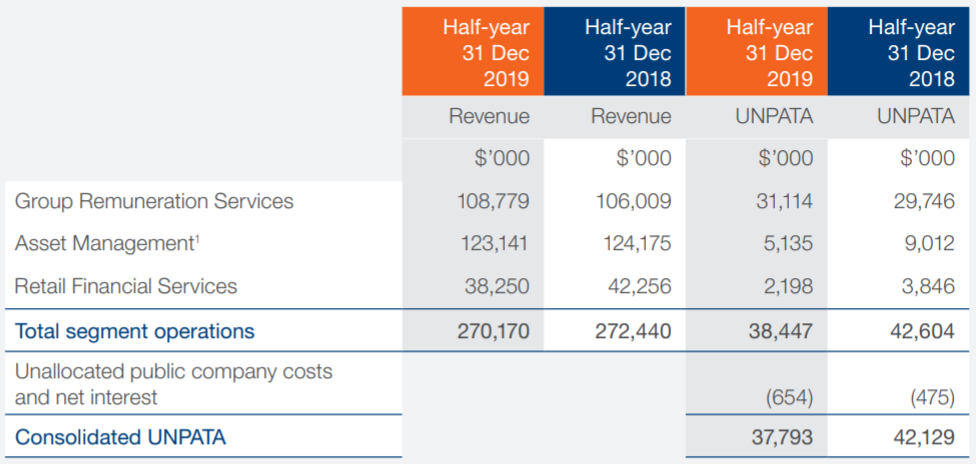

H1FY20 Highlights: For the first half of FY20, the company reported revenue from ordinary activities of $270.39 million and NPAT of $33.95 million. The Group Remuneration Services segment reported revenue of $108.78 million and UNPATA of $31.11 million for H1FY20. The Asset Management segment reported revenue of $123.12 million and UNPATA of $5.135 million. Further, the Retail Financial Services segment reported revenue of $38.25 million and UNPATA of $2.198 million.

H1FY20 Segment Results (Source: Company Reports)

Key Risks: The company’s activities are exposed to a variety of financial risks: market risk (including currency risk and interest rate risk), credit risk and liquidity risk. The company’s results are also exposed to the risks related to lender appetite and new car sales.

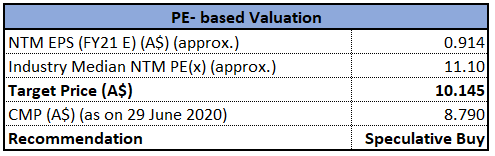

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the last six months, the stock has corrected by 33.65%, but it has increased by 37.52% in the past three months. The stock is currently inclined towards its 52-week low of $5.010. The company currently has senior debt facilities of $320 million that partly fund the Company’s asset management businesses in Australia and New Zealand and the UK. We have valued the stock using the price to earnings multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). Considering the resilient performance of the company’s salary packaging business, its recent steps to restructure its UK operations, expected FY20 results and current trading levels, we give a “Speculative Buy” recommendation to the stock at the current market price of $8.790, down by 0.902% on 29 June 2020.

MMS Daily technical Chart (Source: Refinitiv, Thomson Reuters)

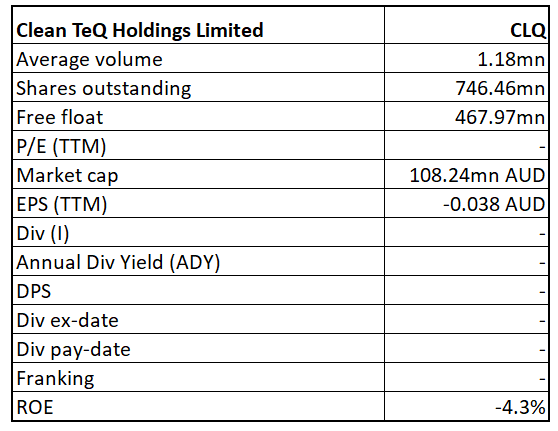

Clean TeQ Holdings Limited

CLQ Details

Commissioning of Tianjin BIOCLENS Factory:Clean TeQ Holdings Limited (ASX: CLQ) is an environmental and mining services group that provides metals recovery and industrial water treatment solutions to its clients. On 25 June 2020, the company announced that its BIOCLENS production facility in Tianjin, China, has been successfully commissioned and achieved steady-state operations. The company has awarded a contract to pilot the BIOCLENS technology to treat 100 cubic meters per day of wastewater produced by a shrimp farm located in Tianjin. The addition of BIOCLENS technology will allow the company to provide a broad suite of solutions to the global water treatment market that are focused on cost-effectiveness, performance, and sustainability.

Sunrise Project Update:The company is currently progressing with the Project Execution Plan (PEP) at its Sunrise Project in conjunction with Fluor Australia Pty Ltd. It is worth noting that Sunrise is one of the largest and most cobalt-rich laterite deposits in the world. Recently, the company implemented a range of measures that reflect the fact that the level of Sunrise Project activity will significantly reduce over the next few months once the PEP is delivered.

Covid-19 Update:As per the update provided on 20 March 2020, there have been no material impacts on Clean TeQ’s ongoing operations from Covid-19. The company has implemented various control measures in several regions where its operate which are limiting the movement of people. The company seems to be well capitalized in order to navigate through this period of near-term uncertainty.

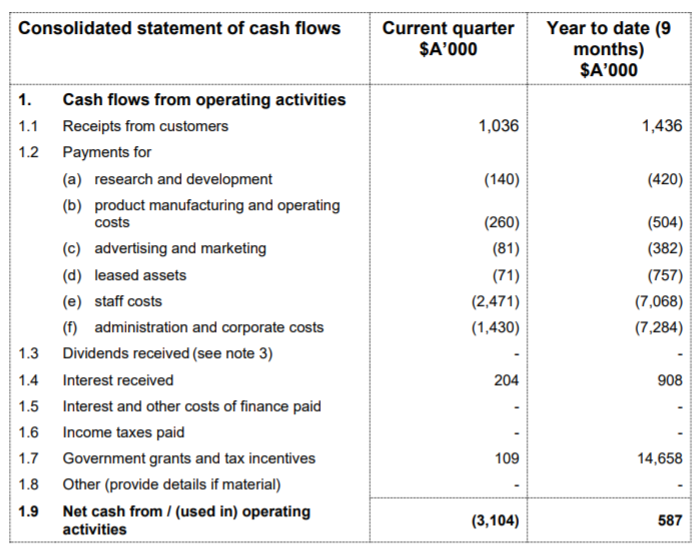

March Quarter Cashflow:During the March quarter, the company received $1.036 million as receipts from customers. Over the quarter, the company spent $140k on research and development, $260k on product manufacturing and operating costs, and $1.43 million on administration and corporate costs. Total net cash used in operating activities stood at $3.104 million.

Cashflow from Operating Activities (Source: Company Reports)

Key Risks:The company’s operations are exposed to various risk including unexpected changes in laws, rules or regulations, changes in investor demand; the results of negotiations with project financiers; the failure of parties to contracts to perform as agreed; changes in commodity prices; unexpected failure or inadequacy of infrastructure, or delays in the development of infrastructure, and the failure of exploration programs or other studies to deliver anticipated results.

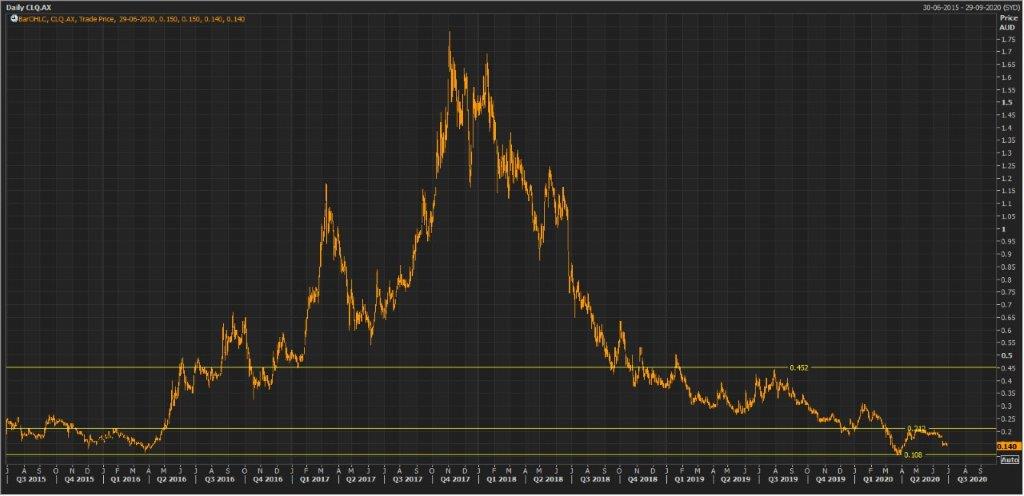

Stock Recommendation:The company remains well capitalized, with around $42.2 million of cash as at 31 May 2020. In the past three months, the stock has increased by 26.09% and is inclined towards its 52-weeks low price of $0.105. The company currently has a current ratio of 4.95x, higher than the industry median of 1.29x. On the TTM basis, the stock is trading at a price to book value multiple of 0.5x, lower than the industry median (Industrials) of 1.7x. Considering the company’s resilient performance amid Covid-19, recent commissioning of Tianjin BIOCLENS factory, progress made in relation to the development of Sunrise Project, and current trading levels, we give a “Speculative Buy” recommendation to the stock at the current market price of $0.140, down by 3.448% on 29 June 2020.

CLQ Daily technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...