Beach Energy Limited

BPT Details

Announcement for Dividends: Beach Energy Limited (ASX: BPT) is actively engaged in the exploration, development, and production of hydrocarbons. The Company’s operating segments include SAWA-South Australia and Western Australia, Victoria, and New Zealand. BPT has announced on 15 Feb 2021 about the important dates and the amount of dividend to be paid to its shareholders. BPT will be paying a dividend amount of A$0.010 for which Ex-Date will be 25 February 2021, Record Date 26 February 2021 and Payment Date 31 March 2021.

Decent Financials: BPT has posted a NPAT of $128.7 mn in 1HFY21 considering a pandemic situation. The production remained steady at 13.0 MMboe and came in line with 1HFY20 figure. EBITDAX of $446mn has generated a revenue sales margin of 63% in 1HFY21.

Production Guidance for FY21 (Source: Company Reports)

Outlook: As per the company reports, BPT is looking to commence offshore Otway campaign with the rig at the Artisan 1 location. BPT is also making progress towards FEED on Trefoil after the acquisition of Mitsui’s interests. BPT is expecting to uplift the field output to ~20 TJ per day through the Beharra Springs Facility.

Valuation Methodology: EV/Sales Multiple based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: In the last one month, BPT has decreased by 15.99% and increased by 9.8% during the last three months on ASX. The stock is currently trading slightly above the average 52-weeks’ price level range of $0.92-$2.40. On the technical analysis front, the stock has a support level of ~$1.563 and resistance of ~$1.891. We have valued the stock using an EV/Sales based multiple relative valuation method and have arrived at a target price of low double-digit upside (in % terms). For the purpose we have taken peers Sensex Energy Ltd (ASX: SXY), Contact Energy Ltd (ASX: CEN), Origin Energy Ltd (ASX:ORG), to name a few. Considering the company’s decent financials, steady production, valuation, and current trading level, we give a “Hold” rating on the stock at the current market price of $1.68, down by 4.274% as on 15 February 2021.

BPT Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Cooper Energy Limited

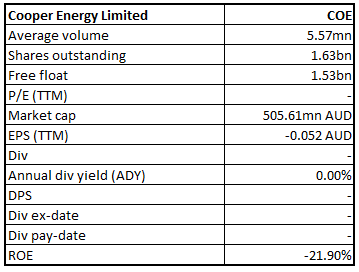

COE Details

Significant Increase in Production During 1HFY21: Cooper Energy Limited (ASX: COE) is an upstream oil and gas exploration and production company whose primary purpose is to secure, find, develop, produce, and sell hydrocarbons. COE has registered a significant rise in production to 1.20 MMboe during 1HFY21 as compared with 0.66 MMboe during 1HFY20. Likewise, Sales Volume increased by 86% during the same period.

Production and Sales (Source: Company Reports)

Profits impacted due to Commissioning of OGPP Project: COE has registered a 40% decline in its EBITDAX to $9.7mn in 1HFY21. Underlying net loss after tax stood at $17.4 mn in 1HFY21 ($2.0mn loss in 1HFY20) on the back of higher costs associated with reconfiguration and commissioning works related with Orbost Gas Processing Plant project.

Outlook: As per the company’s guidance, the company expects the production in a range of 1.50-1.70 MMboe in 2HFY21 which will take its total production to 2.7-2.9 MMboe by the end of FY21. Whereas sales volume can see a significant rise to 2.9-3.1 MMboe by the end of FY21.

Valuation Methodology: EV/Sales Multiple based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: In the last one month, the stock has decreased by ~21.7% and ~12.86% during the last three months. The stock is currently trading below the average 52-weeks’ price level range of $0.295-$0.570. On the technical analysis front, the stock has a support level of ~$0.296 and resistance of ~$0.334. We have valued the stock based on EV/Sales multiple relative valuation and have arrived at a target price of low double-digit upside (in % terms). For the purpose, we have taken peers Worley Ltd (ASX: WOR), Woodside Petroleum Ltd (ASX: WPL), Oil Search Ltd (ASX: OSH) and more. Considering a significant rise in production, sales volume, valuation, current trading level and key risks associated with the business, we give a “Speculative Buy” rating to the stock at the current market price of $0.305, down by 1.613% as on 15 February 2021.

COE Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...