Treasury Wine Estates Limited

.png)

TWE Details

TWE Considering Demerger of the Penfolds Business: Treasury Wine Estates Limited (ASX: TWE) is an international wine business offering a portfolio of luxury, premium and commercial wines to consumers. Recently, the company denied all the allegations filed against TWE in the Supreme Court of Victoria by Maurice Blackburn on behalf of the plaintiff in relation to misleading or deceptive conduct.

TWE’s Potential Demerger of Penfolds: In another update, the company announced about its intention for the demerger of the Penfolds business and associated assets into a different entity by CY21. The company also stated it will ensure that the business persists to operate through the recent COVID-19 crisis. Presently, TWE is unable to forecast any financial guidance for FY20 with the ongoing uncertainties due to coronavirus outbreak.

COVID-19 Business Update: The company also provided an update, stating that its staff in China have returned to working in the office, as have most of its partnership network. The company is closely working with its partners to resume operations through the remainder of FY20. In each geography, the company’s supply chain operations have continued, with no substantial disruptions so far.

Interim Results: During the half-year ended 31st December 2019, the company reported a decline of 0.7% in revenue, which came in at $1,536.1 million, owing to volume declines. The business witnessed strong performance across Asia, ANZ and EMEA regions, led by Luxury and Masstige growth. EBITS for the period stood at $366.7 million, up 2.9% year over, whereas NPAT before material items and Self-Generating and Regenerating Assets (SGARA) rose 5.1% to $229.2 million.

.png)

1HFY20 Revenue (Source: Company Reports)

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company has corrected by 46.37% in the last six months and is currently inclined towards its 52-week low level of $8.400. The company has a market capitalisation of $6.81 billion, with annual dividend yield of 4.23%. The company has a flexible and cost-effective capital structure, with cash and undrawn debt facilities amounting to ~$1.1 billion as on 31st March 2020. Considering the trading levels, resilient financial position, adaptive nature of the business towards a changing environment and current trading level, we have valued the stock using Price to Cash Flow multiple based relative valuation method (illustrative) and arrived at a target price with an upside of lower double-digit (in percentage terms).For the purpose, we have taken the peer group - Coca-Cola Amatil Ltd (ASX: CCL), The A2 Milk Company Ltd (ASX: A2M), and Graincorp Ltd (ASX: GNC). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $9.68, up by 2.434% on 4 May 2020.

TWE Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

United Malt Group Limited

.png)

UMG Details

UMG Implements Demerger: United Malt Group Limited (ASX: UMG) is a newly established demerger of GrainCorp’s global malting business and is involved in the production, sale and distribution of bagged malt, hops, yeast, adjuncts and related products to major brewers, craft brewers, distillers and food companies. As on 4 May 2020, the market capitalization of the company stood at $1.05 billion. Recently, the company announced the implementation of the demerger of United Malt from GrainCorp Limited. Consequently, United Malt Shares have been assigned to potential GrainCorp shareholders and the sale agent. The total number of United Malt Shares on issue stood at 254,284,032.

FY19 Financial Highlights: During FY19, Malt reported EBITDA of $176 million, as compared to $170 million reported in FY18. The increase was primarily on the back of robust customer demand, high capacity utilization and continuous operational productivity. Group reported total revenues of $4,849.7 million, as compared to $4,253.1 million in FY18.

.png)

FY19 Financial Highlights (Source: Company Reports)

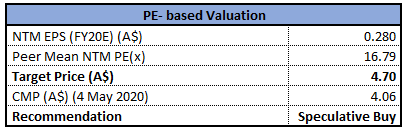

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:As per ASX, the stock of UMG is trading slightly below the average of its 52-week high and low level of $5.240 and 3.600, respectively. The stock of the company has corrected 8.83% in the last one month. The company has a strong market position and is likely to have a prudent balance sheet to support its planned growth prospects.We have valued the stock using Price to Earnings multiple based relative valuation method (illustrative) and arrived at a target price with an upside of lower double-digit (in percentage terms).For the purpose, we have taken the peer group - Costa Group Holdings Ltd (ASX: CGC), Elders Ltd (ASX: ELD), and Graincorp Ltd (ASX: GNC), to name few. Considering the above factors and current trading levels,we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $4.06, down by 1.695% on 4 May 2020.

UMG Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...