Qantas Airways Limited

.png)

QAN Details

Proposal of ACCC: Qantas Airways Limited (ASX: QAN) is engaged in the operation of international and domestic air transportation services. The market capitalisation of the company stood at A$10 Bn as on 28th January 2020. The company recently announced that Debra Joan Smith has resigned from the role of Company Secretary, which became effective on 20th December 2019. The ACCC (Australian Competition and Consumer Commission) through a release has proposed to grant authorization, which allows Qantas, BP Australia and independent BP petrol stations to collectively participate in the BP Rewards, Qantas Frequent Flyer and Qantas Business Reward programs. The ACCC has proposed to give a five-year authorisation for these arrangements which includes allowing BP to require BP-branded petrol stations to take part in the Qantas reward programs.

During Q1 FY20, the company reported revenue amounting to $4.56 billion, reflecting a rise of 1.8%. Also, group unit revenue witnessed a rise of 2.1% as compared to the prior corresponding period, which has been mainly fueled by strong Qantas International performance. The company also added that protests in Hong Kong would adversely impact the 1H profit performance of the group by $25 million, with continuing capacity reduction in place to reduce the second-half impact.

.png)

Financial Highlights for FY19 (Source: Company Reports)

What to Expect: The capacity of the group is anticipated to rise in the range of 0.5% to 1.0% in the first half of the financial year 2020, with improvement in domestic and international flying. The company is capable to generate value with the help of its cornerstone partnerships with Emirates, China Eastern and American Airlines.

Valuation Methodology: P/E Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Gross margin of the company stood at 53.2% in FY19 as compared to the industry median of 39.7%. Net margin of the company stood at 5.0% in FY19 against the industry median of 4.2%. This reflects that the company has better capabilities to convert its top-line into bottom-line, in comparison to the broader industry. We have valued the stock using P/E based relative valuation approach and arrived at a target price offering limited upside (in percentage terms). Therefore, in the light of decent valuations and improvement in key margins, we maintain a “Hold” recommendation on the stock at the current market price of A$6.360 per share, down by 5.216% on 28th January 2020.

QAN Daily Technical Chart (Source: Thomson Reuters)

Webjet Limited

.png)

WEB Details

Extension of Managing Director’s Term: Webjet Limited (ASX: WEB) provides a full range of online travel booking services for flights, hotels, car hire, cruises, tours, etc. The market capitalisation of the company stood at A$1.95 Bn as on 28th January 2020. The company recently announced that Mitsubishi UFJ Financial Group, Inc. has made a change to its substantial holding in the company on 17th January 2020 and the current voting power stands at 10.28% as compared to the previous voting power of 9.05%. In another update, the company announced that it has extended the term of Managing Director, John Guscic and provided changes to his service contract. The contract has been extended to 30 June 2023, from 30 June 2021 earlier. The below picture provides an overview of EBITDA margin for FY17-FY19:

.png)

EBITDA Margin (Source: Company Reports)

Guidance for Underlying EBITDA: The company anticipates underlying EBITDA for FY20 in the ambit of $157 and $167 million, excluding one-off revenues and costs and the impact of AASB16. This indicates an improvement of around 26-34% as compared to FY19, and 16-23% organic EBITDA growth, post adjustment of the additional 5-month contribution from DOTW in 1HFY20. Based on Statutory EBITDA, the company anticipates operating cash conversion for the full year to be in line with its target range of 95-110%.

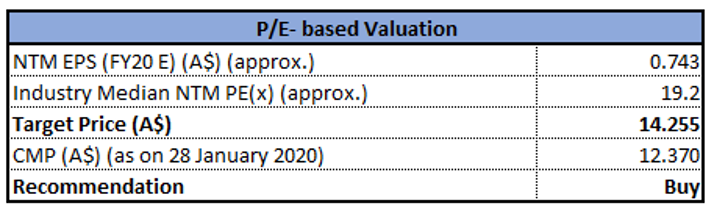

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: With respect to the WebBeds business in the Asia Pacific, the company anticipates significant growth opportunities in China, India and Japan, which offers potential for additional $75-125 million TTV in FY20. Net margin of the company stood at 16.5% in FY19, reflecting YoY growth of 11.0%. During the span of one month and three months, the stock of WEB has provided returns of 9.62% and 30.19%, respectively. We have valued the stock using a P/E based relative valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, considering the decent outlook and favourable valuation, we give a “Buy” recommendation on the stock at the current market price of A$12.370 per share, down by 13.858% on 28th January 2020. The fall in the share price was largely due to the outbreak of coronavirus.

WEB Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...