Commonwealth Bank of Australia

Semi Annual Interest Payment: Commonwealth Bank of Australia (ASX: CBA) is into banking, financial and related services. CBA has advised the details for next interest payment on USD $750,000,000 3.375% Fixed Rate Notes due 20 October 2026. As per the release, rate of interest stood at 3.375% per annum and interest payment date stood at 20 April 2020. The record date happens to be 5 April 2020 and the interest period is from and including October 20, 2019 to but excluding April 20, 2020.

Recent Announcements: Commonwealth Bank of Australia acknowledged the class action proceedings filed by Slater and Gordon in Federal Court of Australia against Colonial First State Investments Limited (or CFSIL), subsidiary of CBA. The class action is related to certain fees charged to the members of Colonial First State FirstChoice Superannuation Trust.

CommBankPERLS XII Capital Notes - Replacement Prospectus: PERLS XII are subordinated, unsecured notes, issued by CBA to raise A$1.25 billion. The offer raises Tier 1 Capital to satisfy CBA’s regulatory capital requirements and maintain the diversity of CBA’s sources and types of funding. The net proceeds of the offer will be used to fund CBA’s business. PERLS XII are perpetual and each PERLS XII is scheduled to pay floating rate Distributions quarterly until that PERLS XII is exchanged or redeemed.

Future Prospects: The bank anticipates the operating context to remain challenging as CBA adapts to increased regulatory change, growing competition, changing customer preferences, and the need to invest in risk and compliance, and in technology and innovation.CBA is, however, well-positioned to pass through this transforming landscape with the backing of a resilient balance sheet, solid customer base and leading distribution and digital assets.

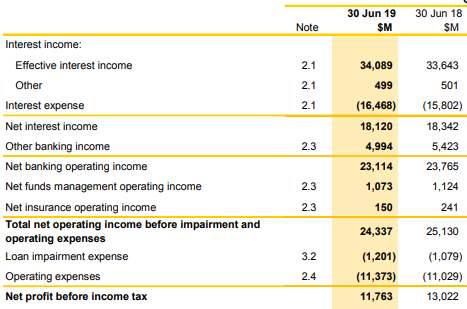

Financial Performance (Source: Company Reports)

Stock Recommendation: The stock of CBA witnessed a rise of 7.12% in the past 6 months and has fallen 3.35% in the past 3 months. The bank’s net interest income has witnessed a CAGR growth of 3.45% in the time span of FY15 to FY19 which can be considered at respectable levels. As per the annual report, CET1 capital ratio of the bank stands at 10.7%. The Bank will focus on serving the changing customer needs and is making the necessary changes to become a simpler, better bank. As per the ASX, the stock of CBA is trading towards its 52-week high of $83.990. Considering the higher trading levels, competitive environment, and other factors, we have a watch stance on the stock at the price of A$79.690 per share, down by 0.957% on October 30, 2019.

Costa Group Holdings Limited

Completion of Institutional Entitlement Offer: Costa Group Holdings Limited (ASX: CGC)is the leading horticulture group in Australia and the leading grower, packer and marketer of fresh fruit and vegetables. The company announced that it has completed the institutional component of its fully underwritten 1 for 4 pro rata accelerated renounceable entitlement offer with retail rights trading. The institutional entitlement offer has been successfully wrapped up, raising around $87 million and it was strongly supported by the eligible Costa institutional shareholders, who took up around 88% of their entitlements.

A bookbuild for institutional entitlement offer shortfall shares was conducted on October 29, 2019 to October 30, 2019 as well as attracted robust demand from the existing shareholders and other institutional investors. The bookbuild cleared at a price of $2.30 per new share, representing premium of $0.10 to offer price of $2.20 per new share.

Financial Highlights: CY19 was a difficult year with performance below expectations. The diversified business model was not as effective as in the previous years. However, the company believes that growth strategy and portfolio of categories will deliver strong shareholder returns over the medium to long term. During the half year ended 30 June 2019, revenue went up by 11.8% on the prior comparative period to $573 million which was mainly driven by growth in production, led by new Colignan farm sales and increased table grape marketing volume and international growth from China and Morocco. The following image gives the broader overview of the key numbers:

.png)

Financial Performance (Source: Company Reports)

Outlook: CGC anticipates CY20 EBITDA-SL to be around $150 million and NPAT-SL to be approximately in-line with CY18 NPAT-SL which was $56.6 million before considering the impact of the equity raising. Despite the trading challenges, it was mentioned that the business fundamentals remain robust.

Stock Recommendation: The stock went down by 15.20% in the past 3 months and also experienced a decline of 4.95% in the past one month. As per the ASX, the company’s stock price is trading close to its 52-week low levels. Whilst results have broadly been in-line with the lower end of the recent guidance and the business model of the company remains robust to generate long-term value to shareholders, the company had highlighted three challenges in the August half year report. Considering the above points, we have a wait and watch stance on the stock at the current price of A$2.630 per share, down by 23.988% on October 30, 2019, taking cues from the recent updates with regards to the completion of institutional entitlement offer and guidance update for CY19.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...