JB HI-FI Limited

.png)

JBH Details

Re-Appointment of Managing Director: JB HI-FI Limited (ASX: JBH) is a retailer of home consumer products with a major focus on consumer electronics, software, etc. The market capitalisation of the company stood at ~A$3.49 Bn as on 29th July 2019. Recently, the company, via a release announced that Airlie Funds Management Pty Ltd on its own behalf and on behalf of Magellan Financial Group Limited and its related bodies corporate have ceased to be a substantial holder in the company from 22nd July 2019. The company further announced the re-appointment of Cameron Trainor as Managing Director of the JB Hi-Fi business, and it also appointed Lynda Blakely as Group HR Director with the responsibility forHuman Resources throughout the JB Hi-Fi and The Good Guys businesses. It added that JB HI-FI Australia had reported growth in total sales of 2.6% in Q3 FY19 as compared to 7.5% in Q3 FY 2018. The following picture provides a broader idea of the group’s 1H FY19 performance:

.png)

Group’s Performance for 1H FY19 (Source: Company Reports).

What to Expect: The company is anticipating the group NPAT to be in the ambit of $237 Mn - $245 Mn in FY19, reflecting a rise of 1.6% to 5.1% on a pcp basis. The group’s key focus areas for FY20 includes implementation of wide entry level Television offer, enhancing supplier engagement, build brand awareness and strengthen supplier partnerships, etc.

Stock Recommendation:The company reported a gross margin of 21.5% in 1H FY19 against the industry median of 25.1%. It posted a return on equity of 16.0% in 1H FY19 in comparison to the industry median of 8.5%. This implies that the company is providing better returns to its shareholders against the broader industry. As per ASIC report dated 23rd July 2019, the stock of JB HI-FI Limited has been shorted 13.14% of total product in issue. Coming to the stock’s past performance, it generated returns of 16.51% and 18.55% in the time span of one month and three months, respectively. As per ASX, the stock is trading closer to 52-week higher level of $29.96. Hence, considering the above-stated facts and current trading levels, we give an “Expensive” rating on the stock at the current market price of A$29.960 per share (down 1.285% on 29th July 2019).

JBH Daily Chart (Source: Thomson Reuters)

Collins Foods Limited

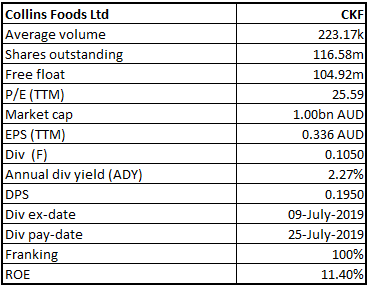

CKF Details

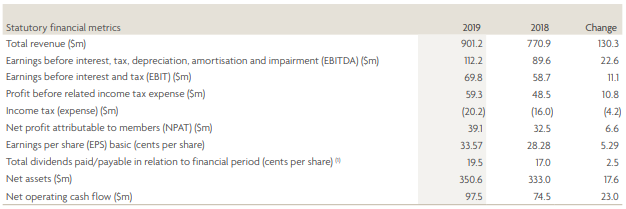

Profit Booking: Collins Foods Limited (ASX: CKF) is into the management, administration and operation of restaurants in Europe, Australia, and Asia with the market capitalisation of ~A$1 Bn as on 29th July 2019. As per the Annual Report 2019, the company stated that the Taco Bell, which is located in Australia, has continued to trade in line with anticipations, with great value products and contemporary restaurant designs resonating well with its customers. The company reported revenue of $901.2 Mn in FY19, reflecting a rise of 16.9% in comparison to $770.9 Mn in FY18 and delivered statutory NPAT of $39.1 Mn in FY19.

Group’s Financial Performance (Source: Company Reports)

Future Prospects: The company is enacting initiatives in order to support a platform for continued sustainable growth throughout the Group. CKF’s continuous focus on delivery, digital and operations would be ensuring that the company is capable to provide its customers with the highest levels of service and satisfaction, while still offering good value. Adding to that, Collins Foods Limited would maintain its disciplined approach to operational management while continuing to invest in new and innovative products that taste great and customers enjoy.

Stock Recommendation: The company reported a net margin of 4.3% in FY19 against the industry median of 9.8% and posted EBITDA margin of 12.7% for the same period as compared to the industry median of 23.5%. The company’s current ratio was 0.90x in FY19 in comparison to the industry median of 1.14x. On the stock’s performance front, it produced returns of 10.75% and 12.95% in the time span of one month and three months, respectively. From the valuation standpoint, its EV/EBITDA, EV/Sales, and PE multiple for TTM stand at 10.1x, 1.3x, and 25.59x, which are higher than the peer median of 9.5x, 1.8x, and 16.9x, respectively, indicating overvalued position of the stock at the current juncture. Currently, the stock is trading closer towards 52-week higher level of $8.850. Hence, considering the stretched valuations and current trading level, we advise the investors to book the profit at the current level and, therefore, recommend a “Sell” rating on the stock at the current market price of A$8.790 per share (up 2.328% on 29th July 2019).

CKF Daily Chart (Source: Thomson Reuters)

Washington H Soul Pattinson & Company Limited

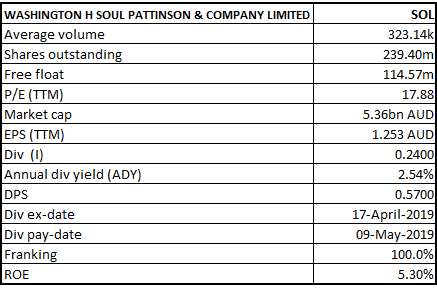

SOL Details

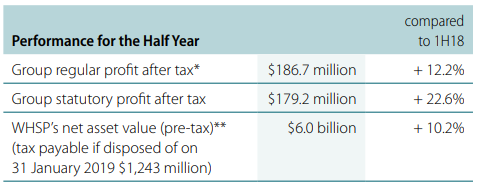

A Look at Chairman’s Letter: Washington H Soul Pattinson & Company Limited (ASX: SOL) is involved into the ownership of shares, coal mining, gold and copper mining and refining, property investment and consulting. The market capitalisation of the company stood at ~A$5.36 Bn as on 29thJuly 2019. Recently, via a release, the company announced that it had changed its substantial holding in Novonix Limited with the voting power of 12.51% in comparison to the previous voting power of 13.89%. The change in substantial holding was made on 24th June 2019. The company delivered regular profit after tax of $186.7 Mn for the half-year ended 31 January 2019, reflecting a rise of 12.2% in comparison to 1H FY18. The company has declared an interim dividend of 24 cents per share in 1H FY19.

Half Year Performance (Source: Company Reports)

Future Aspects:The company is cautious with the early warning signs of a slowing economy. The company further stated that there are numerous key regulatory events which will be influencing the future performance of the company such as approval of TPG and VHA merger and approval of New Acland Stage 3 mine extension for New Hope. The shorter-term opportunities of the company include B2B credit opportunities as well as opportunities from a slowdown in the property market and tighter lending practices.

Stock Recommendation:The company’s net margin stood at 33.5% in 1H FY19 against the industry median of 20.6%, which represents that SOL is effectively converting its top line into the bottom line as compared to the concerned industry. Its current ratio stood at 1.69x in 1H FY19 as compared to the industry median of 1.28x. This indicates that Washington H Soul Pattinson & Company Limited is in a decent position to address its short-term obligations. On the stock’s performance front, it generated returns of 1.13% and -7.02% in the time span of one month and three months, respectively. This reflects that the stock is quite volatile. Hence, considering the aforesaid facts and volatility in the stock, we give an “Expensive” recommendation on the stock at the current market price of A$22.700 per share (up 1.339% on 29th July 2019).

SOL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...