VOCUS GROUP LTD (ASX: VOC)

Banking on sale of New Zealand asset: Vocus has been beaten down a lot in the past one year (down 48.7% as at March 29, 2018) at the back of integration issues on its acquisitions, and other broader level changing landscape of the telecom sector. VOC was also removed from S&P/ASX 100 Index effective March 19, 2018. The group has not paid any dividends lately. The group has a balance sheet debt of about $1 billion and this can be turned around to some extent with a potential New Zealand asset sale given VOC’s asset base. In fact, the group has also responded to media speculation in the above regard and confirmed that the sale process is progressing to the planned timeline with target completion by June 2018 (subject to regulatory approvals, if required). The group has been discussing this with a number of parties and has made no comment on the value of the assets; and expects to sell the asset only if it achieves an appropriate return for shareholders. In view of this, the group is on track with regards to facility refinance plans and expects to complete its refinance by the end of the current financial year. The group intends to record about $2 billion in revenues for FY18. While the group is on the look-out of a new CEO, Michael Simmons was appointed as Interim CEO. On the other hand, Vocus Australia Singapore Cable is on track for “Ready For Service” in Q1 FY19 and growth continues in NBN market share, while earnings guidance for the full year has been revised with underlying EBITDA now expected to be in the range of $365-380 million (previously $370 - $390 million) on revenue in the range of $1.9-2 billion (unchanged) given the challenging Australian Consumer division. Nonetheless, catalysts that might turn the tables are being looked for while we have a “Hold” on the stock at the current price of $2.25

ISENTIA GROUP LTD (ASX: ISD)

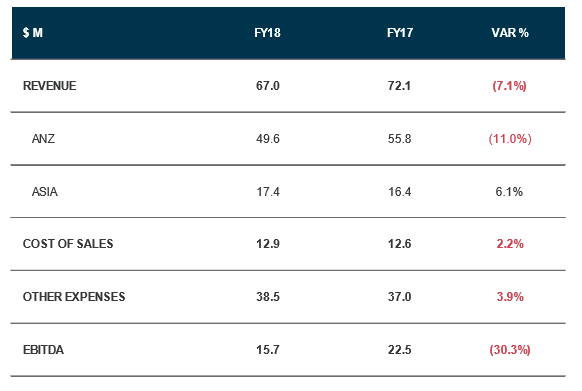

Challenging environment: With a year to date stock price fall of 40.9%, as at March 29, 2018, iSentia seems to be paying in terms of stock performance for the $50 million acquisition of King Content made in 2015. The stock has been smitten by the profit downgrades and exit of their Managing Director. The stock has also been removed from S&P/ASX All Australian 200 Index effective March 19, 2018. The net debt of $50 million is high. On the other hand, Credit Suisse Holdings Ltd has become a substantial holder with 6.48% interest, in March 2018. It is still worth noting that 72% of revenue is recurring that leads to decent cash flow generation and net debt reduction. The group now aims to achieve annualised gross cost savings of $5-7m and realise the benefit of associated actions as it exits FY18. The group is also aiming to develop its share of social listening spend through the rollout of product enhancements through Mediaportal platform. While Asian revenue has risen by 6.1% on prior year due to growth in VAS revenue in 1H FY18, ANZ operating environment was challenging. The group updated its FY18 revenue guidance to $133-136m for the media intelligence business while EBITDA guidance of $32-36m is unchanged. Further, FY18 Loss after income tax (expense)/benefit from exited content marketing has been pointed to be $11.9m. Given the mixed bag, we put a “Hold” on the stock at the current price of $0.84

Group Performance (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...