Whitehaven Coal Limited

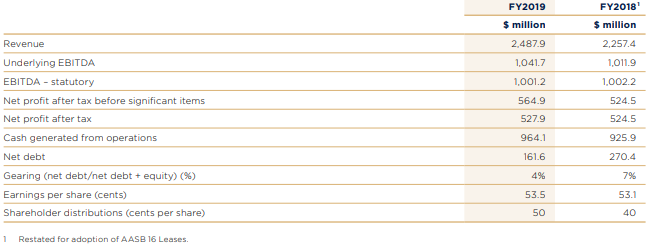

A Quick Look at FY19 Financial Performance: Whitehaven Coal Limited (ASX: WHC) is engaged in the business of the development and operation of coal mines in New South Wales. The company reported a record ROM coal production of 18.4Mt in FY19, an increase of 4% on year-on-year basis. Underlying EBITDA grew by 3% to $1,041.7 million in FY19 from $1,011.9 million in FY18, which was driven by increased EBITDA margin on sales of produced coal to $66/t in FY19, up on the $63/t margin (restated) achieved in FY18. Decline in net debt to $161.6 Mn in FY19 as a result of strong operating cash flow performance. Gearing fell to 4% in FY19 from 7% as on FY18. The strength and resilience of Whitehaven’s cash flow generation have resulted in dividends of 50 cents per share. Shareholders were paid a dividend of $464,854,000 in FY19, which was higher than the prior year.

FY19 Financial Highlights (Source: Company Reports)

Net profit after tax increased to $527.9 Mn in FY19 from $524.5 Mn in FY18. It was impacted by the pre-tax charge to the income statement of $40.5 Mn and accelerated depreciation adjustment to write down the carrying value of existing longwall roof support legs. Operating cash flows of $916.4 Mn in FY19 increased by 3% compared to FY18, this was mainly due to an increase in underlying EBITDA, and higher realised coal prices in FY19 as compared to FY18. Loans and borrowings were reduced to $415.3 Mn in FY19 from $588.1 Mn in FY18, which further resulted in lower interest payments. Investing cash outflows took a dive from $384.9 Mn in FY18 to $193.8 Mn at the year ended 30 June 2019.

The Fall of TRIFR from 6.9 to 6.2 in FY19 led in the improvement of the safety outcome. WHC is in a good position to expand operations from the current opportunities. Growth in EPS from 53.1 cents per share in FY18 to 53.5 cents per share in FY19 was observed.

In another update on ASX, the company announced that the company has entered into a binding agreement to acquire EDF Trading Australia Pty Limited, which owns a 7.5% interest in the Whitehaven-operated Narrabri Mine. Following completion, WHC will own 77.5% of the mine, which is subject to other joint venture partners in the mine not exercising their pre-emptive rights. The consideration for the acquisition is US$72 million, with US$17 million payable on the completion and US$55 million is payable over the five years.

Outlook: Low seaborne LNG prices, Chinese import restrictions and the negative impact upon global GDP from trade tensions between the United States and China resulted in the softening of the thermal coal markets and prices. With softening of prices in the first half of 2019, the market is expected to rebalance as high cost producers moderate production. The high coal inventories at Maules Creek and Narrabri would support sales during September quarter of FY 2020.

Stock Recommendation:The company recorded decent margins in FY19. Gross margin for FY19 stood at 54.6%, higher than the industry median of 50.4%. EBITDA and net margin for FY19 stood at 59.1% and 21.2%, which were also higher than the industry median of 38.4% and 16.7%, respectively. Additionally, return on equity stood at 15.1% in FY19 as compared to the industry median of 13.4%.FY19 was also marked by record distribution of payout ratio of 88%. Currently, the stock is trading closer to its 52-week low levels of $2.99 with PE multiple of 5.89x and an annual dividend yield of 8.89%. Hence, considering the aforesaid factors and current trading levels, we give a “Hold” recommendation on the stock at the current market price of A$3.190 per share (up 1.27% on 2 October 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...