.png)

Stocks’ Details

Baby Bunting Group Limited

Strong Growth in Profit: Baby Bunting Group Limited (ASX: BBN) is one of Australia’s largest retailer of baby goods, catering to parents with children from newborn to three years of age. As on 14 February 2020, the market capitalisation of the company stood at ~$484.75 million. The company has recently released its interim results for the period ended 29 December 2019, wherein it reported a decent increase of 8.1% in total sales to $186.4 million. This was driven by comparable sales growth and new store openings. In the same time span, the company witnessed strong growth of 30.6% in Net Profit After Tax which stood at $7.5 million. This resulted the EPS to increase by 29.8% to 5.9 cents. The decent financial performance of the company enabled the Board to declare an interim fully franked dividend of 4.1 cents per share which is to be paid on 13 March 2020.

.png)

Comparable sales growth (Source: Company Reports)

What to Expect: The company is focusing on investment in IT systems and supply chain to support growth. It is also expecting growth from new markets and expects to roll out new stores. BBN has provided FY20-21 capex guidance and expects it to be around $25 million. It also anticipates NPAT to be in the range of $20.0 million to $22.0 million and EBITDA between $34.0 million and $37.0 million. This guidance assumes the opening of 1 new store in 2H FY20 and no significant disruption from Coronavirus.

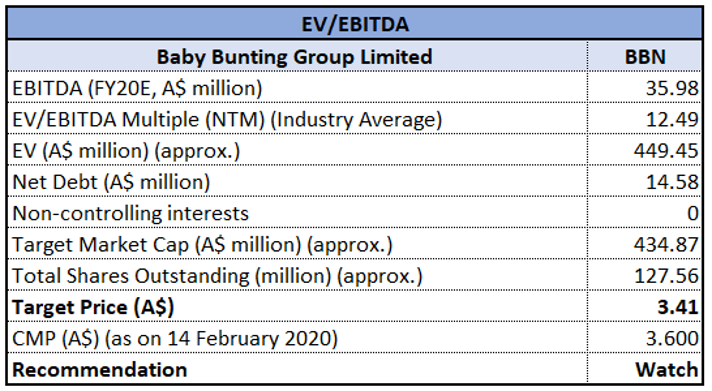

Valuation Methodology: EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of BBN gave a return of 16.56% on YTD basis and a return of 14.11% in the past one month. The stock is trading very close to its 52-weeks’ high level of $4.03. During FY19, gross margin of the company was 34.9%, higher than the industry median 19.8%. In the same time span, ROE of the company stood at 13.5% as compared to the industry median of 14.5%. Considering the returns, trading levels, higher gross margin and decent growth opportunities, we have valued the stock using EV/EBITDA valuation approach and have arrived at a downside of middle single-digit (in percentage terms). Hence, we have a wait and watch stance on the stock at current market price of $3.60, down by 5.263%, owing to release of its financial results.

Bubs Australia Limited

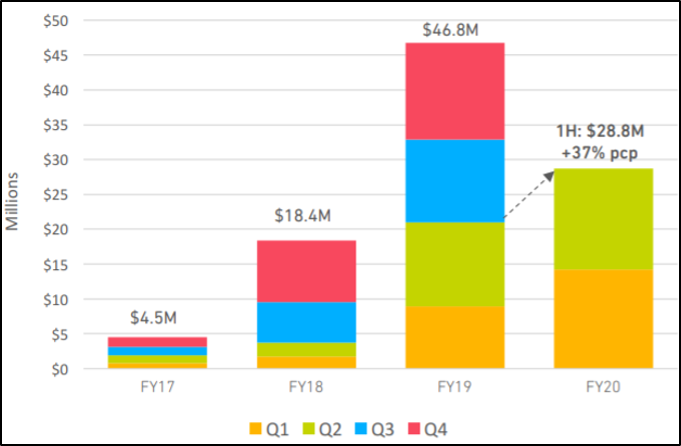

Record Gross Revenue: Bubs Australia Limited (ASX: BUB) is a manufacturer of infant milk formula. As on 14 February 2020, the market capitalization of the company stood at ~$389.41 million. During 1H20, the company reported record gross revenue of $28.8 million, reflecting an increase of 37% on the pcp. In the same time span, domestic sales went up by 30% owing to strong penetration in Coles and Woolworths and launch into Chemist Warehouse.

Quarterly Gross Sales Revenue (Source: Company Reports)

Growth Opportunities and Future Expectations: The company is sustaining growth momentum despite a challenging macro environment and is well placed to cater to Chinese consumers with increased focus on their health, immunity, and food security. The company is focusing on deepening brand connection to drive scale and improved margins.

Stock Recommendation: As per ASX, the stock of BUB is trading close to its 52-weeks’ low level of $0.495, proffering a decent opportunity for accumulation. During FY19, EBITDA margin of the company witnessed a year on year improvement, implying more profitable operations of the company. In the same time span, current ratio of the company stood at 2.03x, higher than the industry median of 1.42x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. On TTM basis, the stock is trading at a Price to book multiple of 3.7x, lower than the industry average (Consumer Non-Cyclicals) of 4x. Considering the current trading levels, improvement in EBITDA margin and decent growth opportunities, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.70, up by 0.719% on 14 February 2020.

Select Harvests Limited

Significant Improvement in Financial Metrics: Select Harvests Limited (ASX: SHV) is engaged in growing, processing, packaging and marketing of almonds and nuts from company and investor owned orchards. As on 14 February 2020, the market capitalization of the company stood at ~$862.73 million. During FY19, EBITDA of the company went up by $43.5 million to $95.2 million and NPAT witnessed an increase of $32.6 million to $53.0 million. This resulted in EPS to increase by 139.7% to 55.5 cps.

FY19 Financial Performance (Source: Company Reports)

What to Expect: The company is expecting an increased demand in key export markets for almonds and is increasing its focus on quality for the food division. SHV is prioritising on cost reduction across all production stages. The company has recently stated that there has been no material short-term impact on its financial performance from the outbreak of Coronavirus. However, it expects near term softening in almond price and demand, the duration of which is dependent on when the supply chains and factories return to normal.

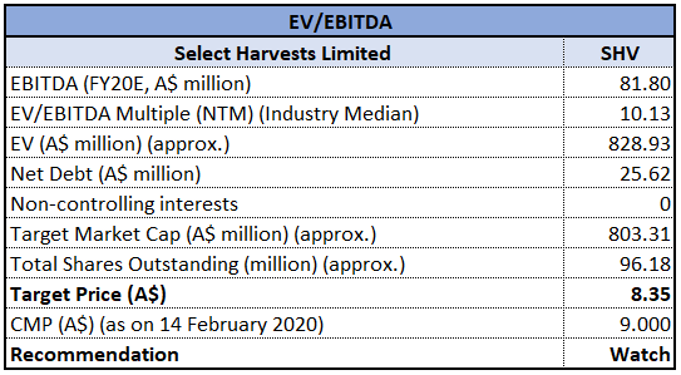

Valuation Methodology: EV/EBITDA Based Valuation

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of SHV gave a return of 21.22% in the past 3 months and a return of 6.03% in the past one month. The stock is also trading very close to its 52-weeks’ high level of $9.430. During FY19, net margin of the company stood at 17.8%, higher than the industry median of 8%. In the same time span, ROE of the company was 13.5% as compared to the industry median of 12.9%. Considering the returns, trading levels, higher net margin and ROE, we have valued the stock using EV/EBITDA based relative valuation method and arrived at a downside of higher single-digit (in percentage terms). Hence, we have a watch stance on the stock at the current market price of $9.0, up by 0.334% on 14 February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...