.png)

Stocks’ Details

Reliance Worldwide Corporation Limited

Decent Sales Outlook for FY20:Reliance Worldwide Corporation Limited (ASX: RWC) is a provider of water flow control and monitoring products and solutions for the plumbing and heating industry. The company recently provided appropriate responses to the aware query from Geraldi Mimery of ASX Listings Compliance Pty Ltd. The document issued by the latter comprised of a set of questions with respect to the half yearly results, NPAT forecast, compliance with listing rules, etc.

1HFY20 Performance: During the half year ended 31st December 2019, the company reported a resilient performance with favourable sales results. Net sales for the period stood at $569.3 million, representing an increase of 4.6% on the prior corresponding half. Sales in Americas witnessed a growth of 7%, while sales in Asia remained stable. Core plumbing and heating sales from UK witnessed a rise of 3%, despite a declining market. Cashflow from operating activities rose substantially, up 163% to $112.8 million. The company has invested in product development and commercialisation, that boosted the operating margins. Furthermore, the company also benefited on the back of synergies from John Guest. The Board declared an interim dividend of 4.5 cents per share, up 13% on the prior corresponding half.

.png)

1HFY20 Results (Source: Company Reports)

Outlook: By the end of the year, the company expects to realise annual synergies of $30 million on a run rate basis from John Guest. The company expects a minimal impact of coronavirus and is devising necessary measures to keep the business on track. Adjusted NPAT for FY20 is now expected in the range of $140 million - $150 million, as compared to the previous guidance of $150 million - $165 million, on account of strong sales performance in the Americas and EMEA along with flat results in APAC. Moreover, the above guidance is subject to the external factors impacting the business.

Valuation Methodology: EV/EBITDA Multiple Based Valuation

.png)

EV/EBITDA Multiple Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 7.89% over a period of 6 months. Currently, the stock is inclined towards its 52-week low level of $3.085. We have valued the stock using EV/EBITDA based relative valuation method. For the purpose, we have taken peers like Adelaide Brighton Ltd (ASX: ABC), James Hardie Industries PLC (ASX: JHX) and ALS Ltd (ASX: ALQ). We have arrived at a target price with single digit upside (in % terms). Considering the performance in 1HFY20, continuous check on potential impact of coronavirus, investments in product enhancement, anticipated sales performance, and current trading level, we give a “Buy” recommendation on the stock at the current market price of $3.340, down 4.571% on 4th March 2020.

IPH Limited

Acquisition Synergies to Shape Future Performance: IPH Limited (ASX: IPH) is primarily engaged in filing, enforcement and management of intellectual property in Australia, New Zealand, Asia and other locations.

Half Yearly Highlights: During the six months ended 31st December 2019, the company continued to deliver strong like-for-like revenue and earnings growth, with continued momentum in the Asian market and margin expansion in Australia. During the half, the company completed the acquisition of Xenith IP and is on track to derive synergistic benefits. Statutory NPAT for the half came in at $27.2 million, up 12% on the prior corresponding period. The Board declared a fully franked interim dividend of 13.5 cents per share, up 13% on pcp.

.png)

Financial Summary (Source: Company Reports)

Outlook: Going forward, the company is expected to benefit from a set of factors, including new major client wins in Australia, full year net cost and revenue synergies of ~$3.4 million from Xenith IP, and additional efficiencies out of Watermark’s integration into Griffith Hack, IPH’s subsidiary. As per the management, the integration is expected to deliver net financial benefits in the range of $2 million - $2.5 million for IPH, starting from FY21.

Valuation Methodology: EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave returns of 34.68% over a period of 1 year. However, the stock has corrected 7.08% in the past 1 month. Despite the decrease in patent filings in Australia, the company still enjoys a leading position in the region. The company is focused on establishing a diverse platform to ensure sustainable results for shareholders. We have valued the stock using EV/Sales based relative valuation method and arrived at a target price with higher single-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $8.490, down 1.963% on 4th March 2020.

Qantas Airways Limited

Decent Growth in Dividend Despite External Uncertainties: Qantas Airways Limited (ASX: QAN) operates airlines, providing travel services across domestic and international locations. The company recently updated that a Director named James Todd Sampson, acquired 2,649 rights for a cash equivalent of $15,800. Another director named Paul Ashley Rayner, acquired 6,623 rights for a cash equivalent of $39,500.

1HFY20 Results: During the half year ended 31st December 2019, the company reported underlying profit before tax amounting to $771 million, down slightly on the prior corresponding period. Statutory earnings per share went up by 3.2% to 28.8 cents per share. Despite the impact of foreign exchange related costs, global freight weakness and disruption in Hong Kong, the company managed to deliver a resilient performance in the presence of capacity discipline, business transformation and growth in market share. Interim dividend amounted to 13.5 cents per share, up 12.5% on pcp.

.png)

Key Performance Metrics (Source: Company Reports)

Outlook: EBIT in the second half is expected to see a negative impact in the range of $100m – $150m due to coronavirus. Despite the above impact, the company is still confident about its future performance as it stands at a stronger position in comparison to its peers.

Valuation Methodology: EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve

Stock Recommendation: The stock of the company gave negative returns of 17.90% over a period of 1 month. Currently, the stock is trading close to its 52-week low level of $5.020. In 1HFY20, the company delivered another strong half on both the domestic and international fronts. While demand in the second half is expected to see the impact of coronavirus outbreak, the company is hopeful of a quick rebound and subsequent return to normal performance scenario. We have valued the stock using EV/Sales based relative valuation method and arrived at a target price with low double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $5.070, down 3.059% on 4th March 2020.

Emeco Holdings Limited

Deleveraging to 1.5x Targeted for FY20:Emeco Holdings Limited (ASX: EHL) provides earthmoving equipment services. Recently, the company notified that Fitch Ratings has upgraded its long-term issuer default rating for Emeco to “B+”. In another update, the company confirmed the acquisition of Pit N Portal, which complements its current business model and adds to business value.

1HFY20 Highlights: During the six months ended 31st December 2019, the company delivered strong growth in earnings, with operating EBITDA amounting to $119.1 million, up 16% on prior corresponding period figure of $102.8 million. Growth was driven by strong demand for metallurgical coal along with contribution from growth assets purchased in 2019.The company also improved its balance sheet position by deleveraging to 1.77x, as compared to 2.32x as at 31 December 2018.

.png)

1HFY20 Results (Source: Company Reports)

Valuation Methodology: EV/Sales Based Valuation

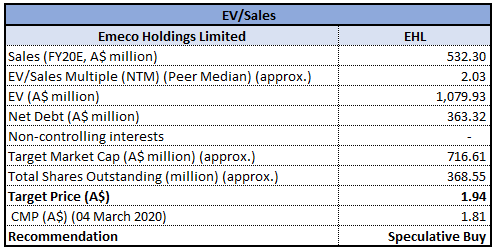

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve

Stock Recommendation: The stock of the company gave negative returns of 12.73% over a period of 1 month. Currently, the stock is inclined towards its 52-week low level of $1.611. During 1HFY20, the company continued to deliver on its strategy of maintaining a highest quality and lowest cost business in the concerned market. Moreover, the company is anticipating significant growth opportunities in the second half and beyond, driven by increase exposure through acquisitions, new projects, continued deleveraging, that will further result in better outcomes from a shareholder perspective. We have valued the stock using EV/Sales based relative valuation method. For the purpose, we have taken peers like Imdex Ltd (ASX: IMD), ALS Ltd (ASX: ALQ) and GR Engineering Services Ltd (ASX: GNG). We have arrived at a target price with single digit upside (in % terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.810, down 5.729% on 4th March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...