Stocks’ Details

AUB Group Limited

Strategic Acquisitions to Aid Business Prospects: AUB Group Limited (ASX: AUB) operates insurance broking, underwriting agency and risk management businesses. On 17th February 2020, the company reported 100% and 40% acquisition of MGA Whittles Group and BizCover, respectively. The company also disclosed that its FY20 half-yearly results will be announced on 25th February 2020. As per another release, the company expects to deliver FY20 NPAT growth towards the top end of the guidance range of 8% - 10%.

Details of Acquisitions: MGA is a leading Insurance Broking group across Australia which operates in broking and risk advisory services across a wide variety of industries. Total acquisition consideration for 50.1% of MGA and 100% of Whittles stood at $140 million payable by $29,131,658 in cash on completion and 8,764,996 ordinary shares, issued within AUB’s 15% placement capacity by 31st July 2020 at an issue price of $12.6490 per ordinary share. Acquisition cost for BizCover stands at $132 million, along a working capital adjustment of ~$3 million. AUB will fund this acquisition through available cash and debt facilities. AUB and BizCover will jointly deliver a new quote-to-bind platform named ‘Austbrokers ExpressCover’, exclusive to Austbrokers members, which significantly enhances broking services to clients.

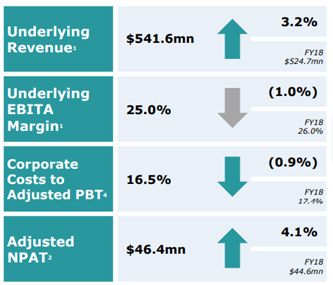

Key FY19 Financial Highlights: AUB declared its full-year results, wherein the company posted an underlying revenue of $541.6 million, up 3.2% on y-o-y basis. Adjusted NPAT came in at $46.4 million, depicting a growth of 4.1% from FY18.

Key Operating Highlights for FY19 (Source: Company Reports)

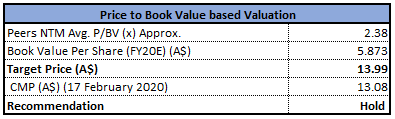

Valuation Methodology: Price to Book Value Based Valuation

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of AUB is quoting at $13.080, with a market capitalisation of ~$943.86 million. The stock is trading towards the upper end of its 52-week trading range of $10.150 and $13.940. The stock has generated returns of 5.53% and 16.38% in the last three months and six months, respectively. Considering the recent acquisitions, price movements and trading levels, we have valued the stock using price to book-based relative valuation method. For the purpose, we have considered peers like PSC Insurance Group Ltd (ASX: PSI), QBE Insurance Group Ltd (ASX: QBE), IOOF Holdings Ltd (ASX: IFL) and arrived at a target price of lower single-digit (in% terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $13.080 per share, up 2.267% as on 17th February 2020, on account of the acquisition news.

Bendigo And Adelaide Bank Limited

Reports $300 million of Capital Raising: Bendigo and Adelaide Bank Limited (ASX: BEN) provides an array of financial services like retail banking, mortgage distribution, business lending, margin lending, business banking and commercial finance. The company also offers invoice discounting, funds management, treasury and foreign exchange services and trustee services. On 17th February 2020, the company reported a fully underwritten $250 million institutional share placement and a non-underwritten share purchase plan of ~$50 million. The shares of BEN have been placed under a trading halt till the placement is completed, with trading expected to recommence on 18 February 2020. The above funding will be utilised to drive the residential mortgage segment and strengthen the company’s balance sheet.

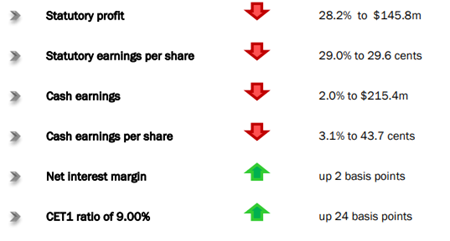

H1FY20 Operational Highlights for the Period ended 31 December 2019: BEN declared its half yearly results, wherein the business reported statutory net profit of $145.8 million, down 28.2% on y-o-y basis, which includes a pre-tax software impairment of $87.1 million and accelerated amortisation of $19.0 million. Net interest margin during the period came in at 2.37%, up 2 bps. Total income on a cash basis came in at $814.7 million, depicting a growth of 1.4% on pcp. Bad and doubtful debts declined by 9% on y-o-y basis and stood at $23.2 million. The business was marked by market leading trust ratings, strong growth, above system lending, margin management, asset quality and growth in new and existing markets. The business reported strong customer growth of 4.9% on pcp terms, despite a challenging environment consisting of low rates, rising regulatory pressure, decrease in consumer and business confidence, etc.

Key H1FY20 Operational Highlights (Source: Company Reports)

The company declared a fully franked dividend of $0.3100 per share, with a payment date of 31st March 2020.

Guidance: The company expects its mortgage lending growth rates to continue to exceed system, with continued growth in the small business portfolio and Commercial Real Estate business.

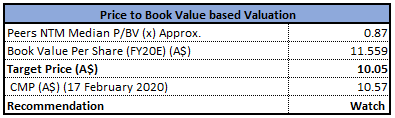

Valuation Methodology: Price to Book Value Based Valuation

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The market capitalisation of BEN stood at ~$5.22 billion. The stock has corrected by 0.66% and 2.13% in the last three months and six months, respectively. In a challenging macro scenario, the company has delivered strong customer growth. The business is looking forward to a $300 million capital infusion to aid business prospects in the coming years. Considering the recent capital infusion, price performance, and customer growth, we have valued the stock using price to book value based relative valuation method. For the purpose, we have considered peers like Bank of Queensland Ltd (ASX: BOQ), Virgin Money UK PLC (ASX: VUK), Challenger Ltd (ASX: IFL), etc., and arrived at a downside of lower single-digit (in% terms). Hence, we have a watch stance on the stock at the current market price of $10.57 per share as on 17th February 2020.

Money3 Corporation Limited

Reported Revenue Grew by 55% on y-o-y basis: Money3 Corporation Limited (ASX: MNY) offers consumer finance required for the purchase and maintenance of a vehicle. On 14th February 2020, the company disclosed the appointment of BDO Audit Pty Ltd as the auditor of the company that follows the resignation of BDO East Coast Partnership.

H1FY20 Business Highlights for the Period ended 31 December 2019: MNY announced its half-yearly results, wherein the company reported revenue of $62.7 million, up 55.0% on pcp. EBITDA and NPAT on normalised basis stood at $30.5 million and $15.7 million, respectively, depicting a growth of 56.4% and 61.9% on pcp terms. The business reported new loan originations of $138.3 million, that surged 58.8% on pcp terms, while cash collections stood at $134.5 million, up by 44.9% on pcp terms. The Loan Book grew by 48.8% to $426.7 million as on 31 December 2019.

Key Operating Highlights for H1FY20 (Source: Company Reports)

The Board of Directors announced a fully franked dividend of $0.0500 per ordinary share, payable on 20 April 2020.

Outlook: The company expects FY20 NPAT from continuing operations to be higher than $30 million and statutory NPAT in excess of $32 million. The loan book is expected to grow over $475 million in H2FY20.

Stock Recommendation: The stock of MNY is trading at $2.900, with a market capitalisation of ~$499.19 million. At the current market price, the stock is quoting at the upper band of its 52 weeks trading range of $1.775 and $2.930. The stock has delivered stellar returns of 33.50% and 27.83% in the last three months and six months, respectively. The stock is available at a price to book of 2.1 as compared to the industry average (Financial) of 4.4x on TTM basis. The business is expected to deliver business growth from increasing consumer vehicle financing and vehicle sales markets across Australia and New Zealand. Considering the business performance, trading levels, and a favourable market scenario, we recommend a “Hold” rating on the stock at the current market price of $2.90 per share, up 7.011% as on 17th February 2020, on account of robust 1HFY20 results.

QBE Insurance Group Limited

Statutory NPAT Soared 41% on y-o-y basis: QBE Insurance Group Limited (ASX: QBE) operates in underwriting general and reinsurance risks, investment management and administration of the economic entity's share of the NSW and Victorian workers' compensation scheme.

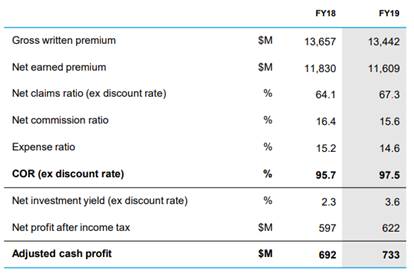

Key FY19 Business highlights for the Period ended 31 December 2019: QBE declared its full year results, wherein the company reported revenue from ordinary activities from continuing operations of US$15,190 million, down 1% from FY18. Statutory net profit after tax stood at US$550 million, up 41% on y-o-y basis. The quarter witnessed positive pricing momentum across all the regions, while average rates increased by 8.3% in H2FY19. At the end of FY19, the business outperformed the index and reported a net return on Investment of 4.6%. Probability of adequacy of outstanding claims stood at 90.0% as compared to 90.1% in FY18. Debt to equity ratio stood unchanged at 38.0%, while the business reported financing and other costs of US$257 million as compared to US$305 million in FY18.

Key FY19 Operating Highlights (Source: Company Reports)

The Board of Directors declared a dividend of $0.2700 per ordinary share with a payment date of 9th April 2020. The percentage of franking was announced at 30%.

Guidance: As per the FY20 outlook, the business expects combined operating ratio within the range of 93.5% to 95.5%. Net investment return is expected within the range of 2.5% to 3.0%.

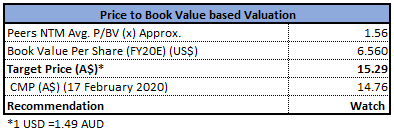

Valuation Methodology: Price to Book Value Based Valuation

Price to Book Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of QBE is trading at $14.760, with a market capitalisation of ~$18.47 billion. At the current market price, the stock is quoting at the upper band of its 52 weeks trading range of $11.010 and $14.790. The stock has delivered positive returns of 12.84% and 17.14% in the last three months and six months, respectively. The business reported a strong capital position when measured against both regulatory and rating agency capital requirements. During FY19, the expense ratio improved to 14.6% from 15.2% in FY18, driven by early benefits from the three-year operational efficiency program. Considering the business performance, trading levels, and improved operational efficiency, we have valued the stock using price to book based relative valuation method. For the purpose, we have taken peers like Insurance Australia Group Ltd (ASX: IAG), Suncorp Group Ltd (ASX: SUN), Challenger Ltd (ASX: CGF), etc., and arrived at a target price of lower single-digit upside (in% terms). Hence, we have a watch stance on the stock at the current market price of $14.760 per share, up 4.311% as on 17th February 2020, taking cues from the recent release related to financial results.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...