Stocks’ Details

Clinuvel Pharmaceuticals Limited

Cash Receipts up 43% Year over Year: Clinuvel Pharmaceuticals Limited (ASX: CUV) is engaged in a photoprotective drug for the treatment of a range of severe skin illnesses pertaining to the exposure to light and harmful UV radiation. Recently, the company stated that it has requested the US Food and Drug Administration (FDA) for a meeting relating to Type C Guidance in order to avail approval on the layout of a multicentre Phase IIb vitiligo clinical study (CUV104). Additionally, the meeting was called to consider the necessary data package to help the filing for a supplemental New Drug Application CUV’s SCENESSE drug in vitiligo.

December Quarter 2019 Update: During the quarter ended 31st December 2019, the company’s cash receipts from customers stood at $3.73 million, up 43% year over year. Annual receipts from customers increased by 19% as compared to the prior corresponding period. At the end of the quarter, cash and cash equivalents stood at $57.44 million. Operating cash outflow for the quarter stood at $635K. For the coming quarter, the company expects cash outflow to be $5.02 million, after making major payments for staff costs and product manufacturing and operating costs of $2.2 million and $1.6 million, respectively.

.png)

Annual Receipts & Operating Payments (Source: Company Reports)

Valuation Methodology:P/BV Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has a market capitalisation of ~$1.23 billion and ~49.41 million outstanding shares. Currently, the stock is trading below the average of its 52-week high and low of $45.88 and $21.00, respectively, proffering an opportunity for share accumulation. As per the most recent quarterly update, the company has been continuously engaged in expanding itself into the USA after receiving approval for marketing SCENESSE. We have valued the stock using Price to Book Value based relative valuation method and have arrived at a target price offering an upside of lower double-digit (in % terms). Considering the recent developments with respect to the key product SCENESSE, strong cash position, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $25.06, down 0.723% on 21 February 2020.

Japara Healthcare Limited

Higher Investments & Portfolio Development are Key Positives: Japara Healthcare Limited (ASX: JHC) is Australia’s top aged care provider, which owns, operates and develops residential aged care homes. As on 21 February 2020, the market capitalisation of JHC stood at $244.53 million. The company will report its 31st December 2019 half-year financial results on 28th February 2020.

FY19 Results’ Key Highlights for the Period Ended 30 June 2019: For FY19, the company reported revenues of ~$399.9 million, increasing 7.1% year over year. Average underlying occupancy in FY19 was ~93%. In FY19, net profit after tax (NPAT) stood at $16.4 million, as compared to $23.3 million reported in FY18, primarily due to higher depreciation and net interest expense. Diluted earnings per share for the period stood at 6.16 cents per share, down from 8.76 cents per share in FY18. The company declared a final dividend of 3.35 cps (50% franked) along with an interim dividend of 2.8 cps, which brought the full-year dividends to 6.15 cents per share.

.png)

FY19 Key Highlights (Source: Company Reports)

Outlook:The company expects its FY20 EBITDA to be in the ambit of 5%-10%, lesser than FY19, on the back of removal of the Government’s temporary subsidy increase that applied from 20 March 2019 to 30 June 2019, challenges in the funding environment along with low occupancy. In FY20, total operational beds are likely to be ~4,627, whereas, the company expects total operational beds to be 4,961 in FY21. The company’s balanced approach with respect to growth coupled with expansion of its existing portfolio reflects the improvement towards sustainable future growth.

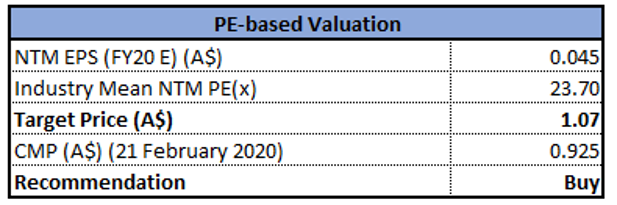

Valuation Methodology:P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company is currently trading close to its 52-week low level of $0.90. The stock has a market cap of ~$244.53 million with an annual dividend yield of 6.72% and a P/E multiple of 14.85x, depicting a decent opportunity for accumulation. Considering the above factors, we have valued the stock using P/E based relative valuation method, and for that purpose, we have considered Regis Healthcare Ltd (ASX: REG), Pacific Smiles Group Ltd (ASX: PSQ) and National Veterinary Care Ltd (ASX: NVL), as peer group which come under healthcare facilities & services category. As a result, we have arrived at a target price of lower double-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $0.925, up 1.093% on 21 February 2020.

Mayne Pharma Group Limited

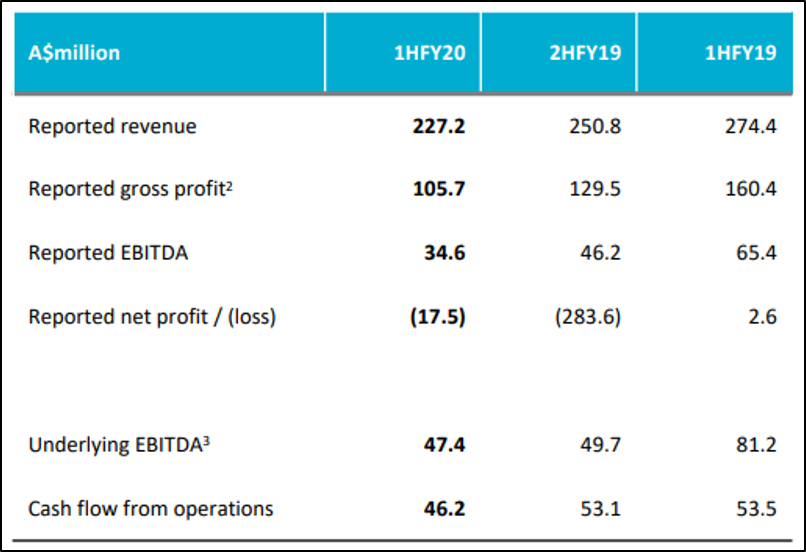

1HFY20 Key Highlights for the Period Ended 31st December 2019: Mayne Pharma Group Limited (ASX: MYX) is a pharmaceutical company focused on applying its drug delivery expertise to commercialise branded and generic pharmaceuticals. During the period, the company’s reported sales stood at $227.2 million, down by 17% from 1HFY19. Reported Gross profit decreased by ~34.1% on a YoY basis. Revenue and gross margin declined primarily due to further competition on key generic products. The company’s reported EBITDA came in at $34.6 million, down by 47% due to higher investments. Reported net loss after tax for the period came in at $17.5 million owing to lower earnings and restructuring expenses. The following picture provides an idea of the key financial numbers:

Financial Highlights (Source: Company Reports)

Balance Sheet & Cash Flow Details: The company has net operating cashflow of $46.2 million, down by 14% as compared to the previous year. As at 31 December 2019, the company’s net debt came in at $290.2 million, cash on hand stood at $98.5 million, with a leverage of 2.5x and shareholders’ funds of approximately $1.1 billion.

What to Expect: The company’s effective commercialisation of E4/DRSP oral contraceptive, generic NUVARING and TOLSURA is likely to boost the financial position of MYX, going forward.Additionally, the company expects contract services to benefit from the expansion of the technical team and the expanding pipeline.

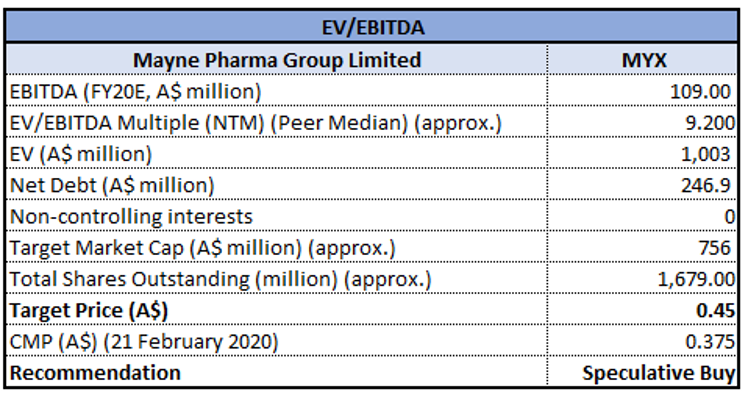

Valuation Methodology:EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company is currently trading close to its 52-week low of $0.365. The stock has a market cap of ~$671.63 million as on 21 February 2020. Several initiatives at the company’s manufacturing sites in Greenville as well as Salisbury are expected to improve overall operational efficiencies and financial performance throughout FY2020 and beyond. Considering the above factors, we have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price of lower double-digit growth (in % terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.375, down 6.25% on 21 February 2020, on tepid 1HFY20 results.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...