.png)

Stocks’ Details

Spark New Zealand Limited

Revenues Up 4% Year Over Year: Spark New Zealand Limited (ASX: SPK) is involved in the business of telecommunication services. The market capitalisation of the company stood at $8.38 Bn as on 19 February 2019. Recently, the company announced that it will distribute a dividend of $0.14154412per share on the security, SPK - ORDINARY FULLY PAID FOREIGN EXEMPT NZX, with an ex-date of March 12, 2020 and payment date of April 3, 2020.

1HFY20 Key Highlights for the Period Ended 31st December 2019: Operating revenues for the period increased by 4% to NZ$1,824 Mn, primarily due to increase in cloud, security and service management business, the launch of Spark Sport coupled with moderation in declines in legacy voice. It was also stated that 1HFY19 has been a successful year for its mobile business. Reported EBITDAI for the period stood at NZ$500 Mn, up 2.2% year over year, on the back of higher revenue base and cost management initiatives. NPAT for the period increased by 9.2% to NZ$167 Mn. An interim dividend of 12.5 cents per share (75% imputed) has been declared.

.png)

1HFY20 Key Metrics (Source: Company Reports)

What to expect: The company is expecting EBITDAI in the range of NZ$1.1 Bn to NZ$1.12 Bn and has given the dividend guidance of 25 cps (at least 75% imputed) for FY20. Capital expenditure is expected to be approximately NZ$370 Mn.

Other Recent Updates: On 3 February 2020, the company announced that it has completed the sale of its entertainment streaming business, Lightbox to Sky Network Television Limited (Sky).

Valuation Methodology: EV/EBITDA Based Valuation

.png)

EV/EBITDA based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated a positive return of 20.4% in the past six months. As per the ASX, the stock is currently trading close to its 52-week high level of $4.64 with a price to earnings multiple of 21.39x, and an annual dividend yield of 4.39%. The business of SPK is likely to improve on the back of strong balance sheet and a disciplined approach to capital expenditure and cost control initiatives. We have valued the stock using P/E based relative valuation method, and for the said purpose, we have considered peers like TPG Telecom Ltd (ASX: TPM), Vocus Group Ltd (ASX: VOC) and Macquarie Telecom Group Ltd (ASX: MAQ), to name few. Therefore, we have arrived at a target price offering an upside of single-digit (in percentage terms). Hence, considering the aforesaid facts and current trading levels, we give a “Hold” rating on the stock at the current market price of $4.58 per share, up 0.439% on 19 February 2020.

Seven Group Holdings Limited

Operational Focus & Higher Revenue Base are Key Positives: Seven Group Holdings Limited (ASX: SVW) is a diversified investment group which includes wholly owned industrial operating businesses along with key strategic investments in media and industrial equipment hire.Recently, the company announced that it will distribute a dividend of $0.21000000per share on the security, SVW - ORDINARY FULLY PAID, with an ex-date of March 25, 2020 and payment date of April 20, 2020.

1HFY20 Key Highlights for the Period Ended 31st December 2019: The company’s trading revenue increased by 12% on pcp to $2,262.8 Bn. The robust results can be attributed to operational focus, along with growth achieved in all Industrial Services business. Its underlying earnings before interest and tax (EBIT) increased by 7% on pcp to $417.6 million. Its underlying net profit after tax (NPAT) increased by 3.2% on pcp to $254.7 million. Underlying earnings per share (EPS) was almost flat year over year and came in at 75 cents per share. The company declared an interim dividend of 21 cents per share (full franked).

.png)

1HFY20 Key Metrics (Source: Company Reports)

What to expect: The company expects opportunities for growth in Industrial Services and Energy businesses, on the back of robust mining production, infrastructure investment and East Coast gas demand. For FY20, the company expects underlying EBIT to grow in the high single digits against FY19 underlying EBIT, which includes any impact of AASB 16.

Valuation Methodology: Price to Earnings Based Valuation

.png)

Price to Earnings based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated a positive return of 20.86% in the past six months. As per the ASX, the stock is currently trading close to its 52-week high level of $21.960 with a price to earnings multiple of 30.31x, and an annual dividend yield of 2.13%. We have valued the stock using P/E based relative valuation method, and for the said purpose, we have considered peers like Monadelphous Group Ltd (ASX: MND), ALS Ltd (ASX: ALQ) and Emeco Holdings Ltd (ASX: EHL), to name few. Therefore, we have arrived at a target price offering a downside of single-digit (in percentage terms). Hence, considering the aforesaid facts and current trading levels, we give an “Expensive” rating on the stock at the current market price of $21.47 per share, up 8.985% on 19 February 2020, on the back of stellar 1HFY20 results.

Fletcher Building Limited

Higher Investments & Enhancing Shareholder’s Value are Key Positives: Fletcher Building Limited (ASX: FBU) is engaged in building products, distribution, laminates & panels, concrete, construction and steel and has a market capitalisation of $4.07 Bn as on 19 February 2019.Recently, the company announced that it will distribute a dividend of $0.11000000per share on the security, FBU - ORDINARY FULLY PAID FOREIGN EXEMPT NZX, with an ex-date of March 19, 2020 and payment date of April 9, 2020.

1HFY20 Key Highlights for the Period Ended 31st December 2019: Total revenues for the period decreased by 5% to NZ$3,961 Mn, owing to tough market conditions in Australia. EBIT from continuing operation for the period stood at NZ$184 Mn, down 26% year over year. Net earnings came in at NZ$82 million, down 8% year over year. An interim dividend of 11 cents per share has been declared in 1HFY20. Cash outflow from operating activities for the period stood at NZ$5 million, as compared to cash out flow of NZ$114 million in the prior corresponding period.

.png)

1HFY20 Key Metrics (Source: Company Reports)

What to expect: For FY20, the company anticipates EBIT before significant items in the ambit of $515 million to $565 million. In second half of FY20, the company expects improved performance from steel along with robust pipeline of residential house sales, which is due for settlement.

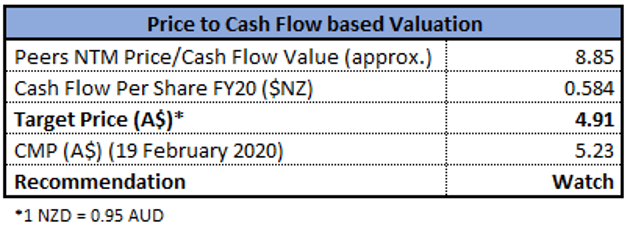

Valuation Methodology: Price to Cash Flow Based Valuation

Price to Cash Flow based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per the ASX, the stock is currently trading close to its 52-week high of $5.51 with a price to earnings multiple of 26.82x, and an annual dividend yield of 3.75%. The company remains on track to enhance shareholder’s interest and invests higher to drive ongoing improvements and growth. We have valued the stock using P/CF based relative valuation method, and for the said purpose, we have considered peers like Boral Ltd (ASX: BLD), James Hardie Industries PLC (ASX: JHX) and CSR Ltd (ASX: CSR), to name few. Therefore, we have arrived at a target price offering a downside of single-digit (in percentage terms). Hence, considering the aforesaid facts and current trading levels, we have a watch stance on the stock at the current market price of $5.23 per share, up 6.085% on 19 February 2020, taking cues from the recent release related to financial results.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...