Insurance Australia Group Limited

.png)

IAG Details

GWP up 1.4% Year over Year in 1HFY20: Insurance Australia Group Limited (ASX: IAG) is engaged in providing general insurance services, which incorporates a wide range of personal and commercial insurance products. Recently, the company announced that it will distribute a dividend of $1.073 per share on the security, (IAGPD - CAP NOTE 3-BBSW+4.70% PERP NON-CUM RED T-06-23 securities)with an ex-date of March 5, 2020 and Payment Date of March 16, 2020.

Key Highlights for 1HFY20:During the year ended 31 December 2019, the company reported gross written premium (GWP) of 5,962 million, an increase of 1.4% on a year over year basis. GWP was mainly driven by higher rates and favourable foreign exchange effect along with solid performance in Australia and New Zealand. Insurance profit for the period stood at $501 million, up 1% on a year over year basis. Net profit after tax amounted to $283 million, down 43.4% on pcp NPAT of $500 million.

.png)

1HFY20 Performance (Source: Company Reports)

Other Recent Updates: Recently, the company announced the appointment of Julie Batch as Chief Strategy & Innovation Officer of the company. Julie Batch will be responsible to lead a recently established Strategy & Innovation division which merges IAG’s existing strategy function with its Customer Labs division. In another update, the company informed the market that Group Executive David Harrington has stepped down from his role, effective from March-end 2020.

Outlook: The company expects reported insurance margin to be between 12.5-14.5% in FY20. The company expects FY20 to contain gross written premium (GWP) growth of lower single-digit. It further anticipates net losses from natural perils to be approximately $850 million in FY20.

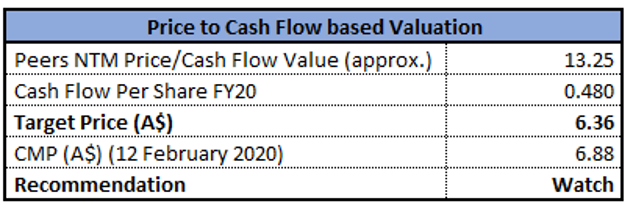

Valuation Methodology:P/CF Based Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:As per ASX, the stock is trading close to its 52-week low of $6.810. The stock gave a negative return of 9.61% in the past one year. As per ASX, the stock has a market cap of ~$15.88 billion with a PE multiple of 14.85x and an annual dividend yield of 4.66%. We have valued the stock using P/CF based relative valuation method, and for the said purpose, we have considered peers like NIB Holdings Ltd (ASX: NHF), QBE Insurance Group Ltd (ASX: QBE) and Suncorp Group Ltd (ASX: SUN), to name few. Therefore, we have arrived at a target price with a downside of single-digit (in percentage terms). Considering the revised guidance, valuation, and current trading levels, we have a watch view on the stock at the current market price of $6.88 per share, up 0.146% as on 12 February 2020.

IAG Daily Technical Chart (Source: Thomson Reuters)

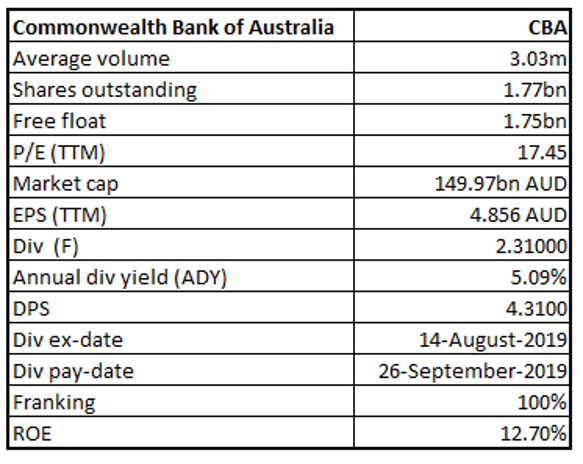

Commonwealth Bank of Australia

CBA Details

Statutory NPAT up 34% Year over Year in 1HFY20: Commonwealth Bank of Australia (ASX: CBA) is a well-known bank in Australia, which offers banking, financial and related services. The market capitalisation of the bank stood at $149.97 Bn as on 12th February 2020. Recently, the company stated that NZX Limited and Skycity Entertainment Group Limited, a substantial holder of the company, has increased its voting power from 7.047% to 8.161%.

Key Highlights for 1HFY20 Results: During the period, the company reported statutory net profit after tax amounting to around $6,161 million, up 34% year over year. Cash net profit stood at $4,477 million. Earnings per share came in at 253 cents for the period. Total assets stood at $980 billion. Common Equity Tier 1 (or CET1) capital was 11.7% on an APRA basis, which expanded 90 bps year over year. During the same period, the group’s leverage ratio stood at 6.1% on an APRA basis. The strength of the bank’s operating and capital performance enabled the Board to declare a final fully franked dividend of $2 per share.

1HFY20 Highlights (Source: Company Reports)

Other Recent Updates: On 12 February 2020, the company issued a report providing an update on actions taken by CBA to deliver the Remedial Action Plan (RAP). The reviewer opines that the company has made robust progress and remains on track to implement its plan.

What to Expect: The company remains well placed in a difficult operating environment due to global macroeconomic uncertainty as well as historically low-interest rates. Further, it is well-positioned to address the needs of its customers, demonstrated by good volume growth in its core markets of home lending, business lending and household deposit, on the back of solid capital position and healthy balance sheet.

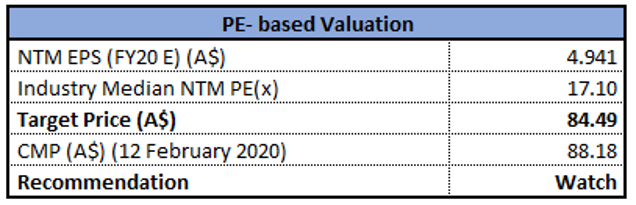

Valuation Methodology:P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week high of $88.560. The stock gave a positive return of 14.77% in the past one year. As per ASX, the stock has a PE multiple of 17.45x and an annual dividend yield of 5.09%. We have valued the stock using a P/E-based relative valuation method and arrived at a target price, which is offering marginal corrections of single-digit (in percentage terms). Hence, considering the above factors, we have a watch view on the stock at the current market price of $88.18 per share, up 4.084% on 12th February 2020, on the back of decent 1HFY20 results.

CBA Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...