.png)

Stocks’ Details

NOVONIX Limited

Three-Phased PUREgraphite Growth Plan:NOVONIX Limited (ASX: NVX) is engaged in the development of a strategy to transform itself into a supplier of advanced battery materials, equipment and services to the global Lithium-ion Battery (LIB) market.

Shareholding Update:In a recent announcement, the company notified that St Baker Energy Holdings Pty Ltd became a shareholder with a voting power of 18.1%. On the other hand, Brickworks Limited and Washington H. Soul Pattinson and Company Limited, ceased to be shareholders in the company.

Capital Raising:On 30th June 2020, the company notified about the completion of the Equity Raising announced in May 2020, raising a total of $63 million and restructuring the balance sheet to execute its strategy to become a leading producer of high performance and competitively priced battery anode materials for lithium-ion batteries for electric vehicles and energy storage systems.

.png)

Updated Capital Structure (Source: Company Reports)

Growth Plan for PUREgraphite: In Phase 1 of the PUREgraphite Growth Plan during 2020-2021, the company expects to ramp up the capacity to 2K tons a year. In Phase 2 (2022-2025) and Phase 3 (2026-2030), capacity is targeted at 25K tons and 100K tons per year, respectively.The company has agreements with the two largest battery makers across the globe, including the SAMSUNG Supply Agreement and R&D Collaboration and SANYO Commercial Collaboration.

.png)

Phased Growth Plan for PUREgraphite (Source: Company Reports)

Market Outlook:Renewablesand green energy demand is expected to drive a ten-fold increase in battery materials demand by 2030. In the next 5-10 years, the total addressable market of anode and cathode materials is expected to be between US$50 billion – US$100 billion, from US$10 billion currently. In the recent update on its Technology Roadmap, the company outlined the impact of an increase in electric vehicles (EV) demand on the demand for battery materials. Annual passenger EV sales per year are expected to be around 56 million by 2040, which, in turn, will drive a substantial increase in the demand for high performance battery materials. The company’s first sales of NOVONIX anode will start with SAMSUNG SDI in 2020.

Key Risks: The company is exposed to interest rate risk arising from its long-term borrowings with variable rates. Cash and cash equivalents and deposits with banks and financial instruments expose the company to credit risk. Risk of liquidity arises from any failure in accurately forecasting the cash flows for the business.

Stock Recommendation: The stock of the company gave returns of 461.24% in the last three months and is currently inclined towards its 52-week high of $1.54. As on 31st March 2020, the company reported cash and cash equivalents amounting to $3.316 million. As on 31st December 2019, total debt of the company amounted to $20.93 million, and cash and short-term investments came in at $0.56 million. On a trailing twelve months (TTM) basis, the stock has a price to book value multiple of 11.6x as compared to the industry median of 1.4x. Considering the above factors, along with the proposed growth plan for PUREgraphite, recent capital raising, and long-term market outlook and recent price appreciation, we advise investors to wait for better entry levels and, thus, have a watch stance on the stock at the current market price of $0.950, down 7.767% on 7th July 2020.

Adacel Technologies Limited

New Orders from US Army:Adacel Technologies Limited (ASX: ADA) is a leading developer of operational air traffic management systems, speech recognition applications and advanced air traffic control simulation and training solutions.

Market Update: The company issued guidance for before tax of ~$4.8 million for the financial year ended 30 June 2020, on account of strong operational execution.The guidance, however, excludes the effect of one-off items relating to litigation and the impact of the adoption of AASB 16 Leases and represents a 20% increase on the previous guidance. Key factors contributing to the guidance include progress in critical infrastructure installations and two Aurora air traffic management projects in Fiji and Portugal. As at 30th June 2020, the company expects a cash balance of ~$5 million.

Litigation Update: In May, the company received an adverse ruling in its arbitration with the former Chief Executive Officer in the State of Florida and consequently updated the estimated FY2020 one-time, non-recurring costs to be in the range of $1.9 million to $2.2 million, as compared to $1.1 million to $1.4 million earlier.

Orders from US Army: The company recently notified regarding orders received for 60 Adacel simulators to further support its Air Traffic Control Common Simulator (ACS) Program for the US Army, with a contract value of ~USD$2.8 million to offer software and hardware support. Completion of the order is expected during H1FY21. During H1FY20, the company reported revenue and EBITDA amounting to $19.7 million and $3.2 million. PBT for the period came in at $2.1 million.

H1FY20 Results (Source: Company Reports)

Key Risks: First and foremost, uncertainty regarding the ongoing litigation with the former CEO seems to be a potential threat to the business. The new PBT guidance does not take into account the impact of the litigation, which may impact the company’s financial performance. In addition, factors such as lengthy tender and decision-making processes from the aviation authorities and funding constraints faced by them can be a challenge while forecasting accurate timing and quantum of both new and ongoing business activity. Moreover, risk pertaining to the renewal of contracts should also be looked upon.

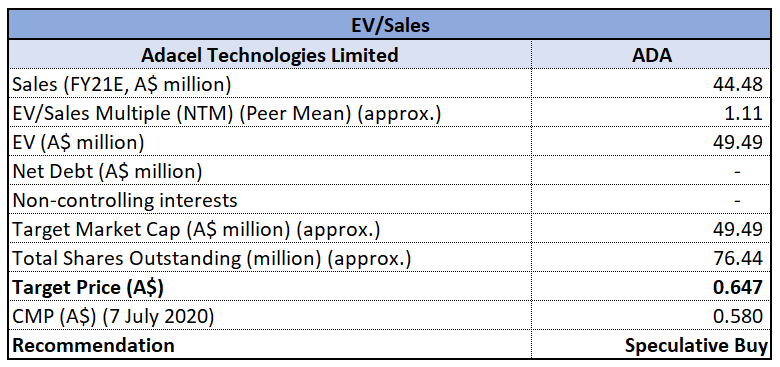

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave returns of 22.47% in the last one month. The revised PBT guidance provided by the company and new orders from the US Army has boosted investor confidence. On the other hand, risks pertaining to litigation, renewal of contracts and difficulty in forecasting, should not be ruled out. In 1HFY20, the company had a gross margin of 87.2%, as compared to 1HFY19 gross margin of 82.9%. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price of low double-digit upside (in percentage terms). Considering the backdrop of the above factors, we give a “Speculative Buy” rating on the stock at the current market price of $0.580, up 6.422% on 7th July 2020.

XREF Limited

Strong Sales Performance Despite COVID-19 Outbreak:XREF Limited (ASX: XF1) is primarily engaged in the development of human resources technology that automates the candidate reference process for employers.

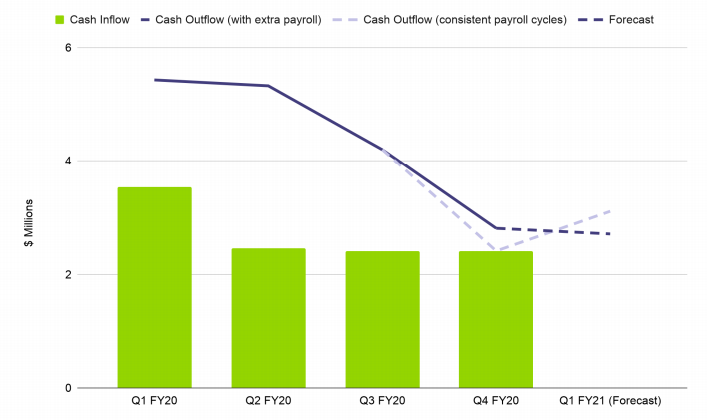

Business Update: The company recently updated that unaudited sales for Q4FY19 reached $2.7 million, despite the impact of COVID-19. Cash receipts for the quarter stood at $2.4 million. During the quarter, the company introduced new clients on the platform, including Laureate International Universities, Frucor Suntory, NSW Public Service Commission, etc.The company captured the growing market demand for improved ways to perform candidate verification as businesses switched to remote working. Of the total $2.7 million credits sold during the quarter, 63% were from clients deemed essential services during COVID-19, 14% came from international offices in Europe and North America and 14% from new clients.

Cash Position: As a result of COVID-19 outbreak, the company witnessed accelerated adoption and took advantage of this opportunity to lessen cash expenses. Since December 2019, the company has scaled back event costs, travel, development costs, office leases and has reduced headcount from 98 to 61 people. Cash outflows in the June quarter stood at $2.8 million, down 47% from Q2FY20. The company has decided to change the payroll calendar for FY21 from the current 13 periods a year to the more traditional 12 months per year. As a result, in Q1FY21, the company expects cash outflows of $2.7 million, representing a decline of 50% on the prior corresponding quarter.

Cashflows (Source: Company Reports)

Key Risks: The company’s usage of financial instruments exposes it to currency risk, interest rate risk and certain other price risks, resulting from its operating and investing activities. Credit risk pertaining to third party default on its obligation to the group can result in a loss for the business. Failure to manage cash flows through cost control gives rise to the risk of liquidity.

Stock Recommendation: The stock of the company gave positive returns of 59.09% in the last 3 months. Currently, the stock is trading at the lower band of its 52-week trading rangeof $0.080 - $0.535, offering an opportunity for accumulation. The company has continued to witness growth in credit sales, despite the current challenging environment. In addition, it has continued to keep a regular check on costs and has been successful in substantially reducing outflows to promote cash conservation.Over the period covering FY15 – FY20, the company has reported an approximate CAGR of 71% in credit sales. Considering the price movement, business continuity despite COVID-19, cash conservation initiatives, CAGR in credit sales, and current trading levels, we give a “Speculative Buy” rating on the stock at the current market price of $0.17, down 2.857% on 7th July 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...