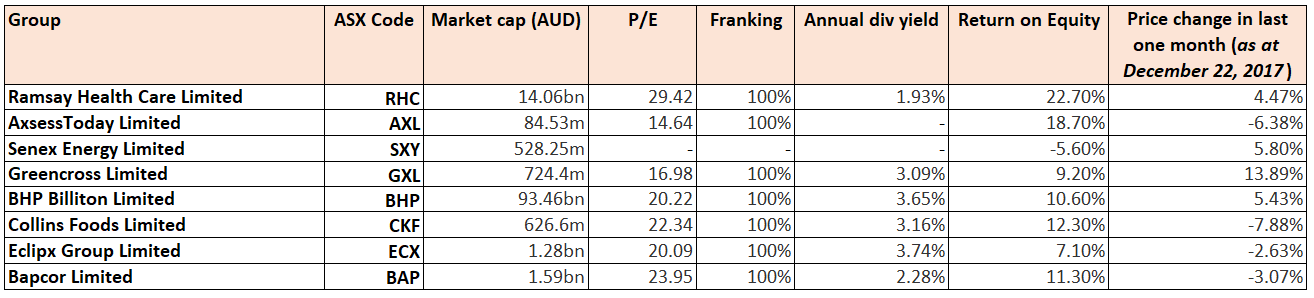

Stocks’ Details

Ramsay Health Care Limited (ASX: RHC)

Long-Term Potential: In Australia, Ramsay’s volume growth continues to be driven by increase in ageing population. Operational efficiencies have been driving the margin improvements. The group is also expected to get a boost from the latest Federal Health Minister, Greg Hunt’s announcement for new Reforms which will provide support to private health system (PHI) so RHC expects some recovery in PHI participation rates and opportunities from expanded mental health care. Some of the reforms relate to patients with limited health cover having the ability to upgrade their cover to access in-hospital mental health services without serving a waiting period. On the other hand, RHC continues to face challenges in France, whereas it remains a leader in UK as its cost restructured program is delivering operational efficiencies. During 2017, there were few developments like 500 beds were in operation along with 27 operation theatres and 3 private emergency centres. Due to regulatory delays, the expansion has not been in line as expected; however, the group is progressing with its integrated care opportunities which will broaden RHC’s business beyond hospitals. The Company’s strong balance sheet provides it with the opportunity to accelerate growth through expansions and acquisitions. Though there are concerns about falling private health insurance numbers but the demand for the service due to ageing population and increased chronic disease burden will offset the limitations.Meanwhile, RHC stock has risen 12.59% in three months as on December 22, 2017. Given the potential, we put a “Buy” recommendation on the stock at the current price of $69.82

Achievements in Patient Outcomes (Source: Company Reports)

AxsessToday Limited (ASX: AXL)

Strong growth in loan book: AxsessToday aims to deliver an FY18 NPAT of at least $6.5m (81% rise over FY17), and has demonstrated strong growth in all key operating metrics during the quarter ended 30 September 2017 (Q1 FY18). The equipment funding solutions provider has reported continued strong growth in the loan book to $212m as at 30 September 2017, an increase of 27% over 30 June 2017 and 215% over prior corresponding period. The group finds support from expanded distribution network and product offering and IT systems related investment with a good capital accessibility through a healthy funding mix. Given the growth prospects, roll-out of next generation upgrades, and favourable market conditions in hospitality and transport segments, we put a “Speculative Buy” recommendation on the stock at the current price of $$1.52

Senex Energy Limited (ASX: SXY)

Sale of raw gas from Western Surat Gas Project: Senex seems to be positioned well to leverage the impact on the east coast gas market with its two gas projects transforming into earnings over the next couple of years. The group’s leverage to rising oil prices and longer-term potential through its oil linked Western Surat Gas Project’s sales agreement with GLNG are expected to maintain momentum. Lately, the group reached an agreement with GLNG for the sale of raw gas from Phase 2 of the Western Surat Gas Project. The Phase 2 program is the Company’s first major investment in the Western Surat Gas Project, and involved 30 appraisal wells on the Eos and Glenora blocks, located directly north of GLNG’s producing Roma field. Further, full sanction in the coming months will see the facility online in late 2018, in readiness for the next phase of wells to be brought online. Given the development updates and potential to be unveiled, we put a “Buy” on the stock at the current price of $0.37

Greencross Limited (ASX: GXL)

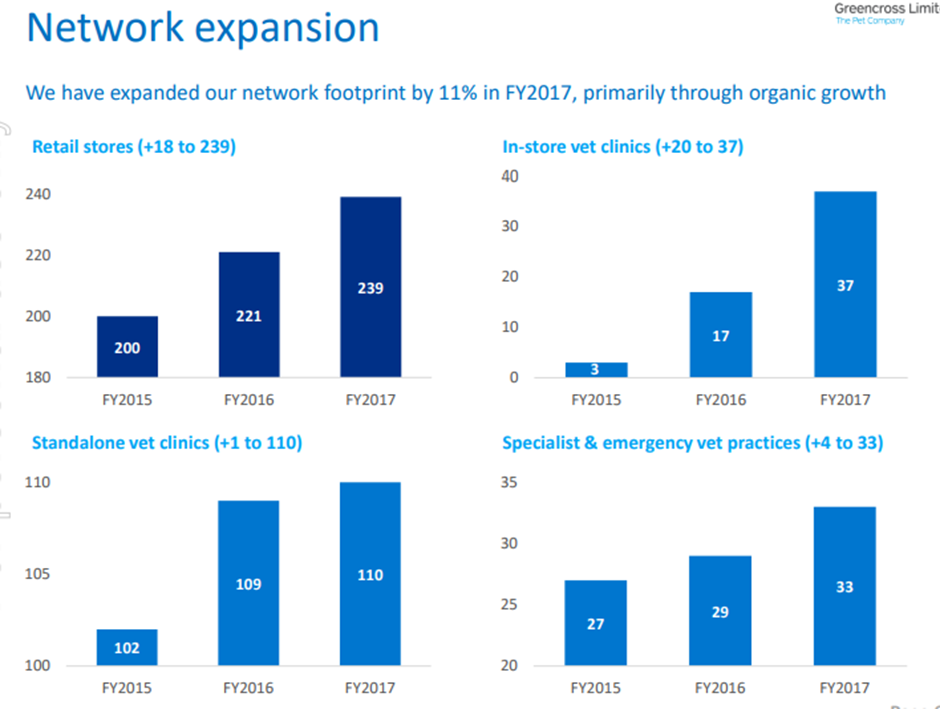

Ongoing Sales Growth: In FY17, Greencross continued to be the leading specialist pet care company as the Group Revenue and Gross Margin were up by 11%. Underlying EBIDTA and NPAT were up by 9% and 21%, respectively. The group continued to expand their network with the addition of 43 new stores and clinics, and also opened 2 specialist and emergency hospitals in Brisbane and acquired 2 specialist and emergency practices in Adelaide. The group saved the lives of over 7000 animals and raised more than $2.8 million for RSPCA. It has a wide customer base and is committed to reward for their loyalty. GXL continued its expansion in Retail segment as well with Private label reaching 21% of the sales and the Online Revenue growing by 55%. Greencross isn’t just growing through expansion, the like-for-like (LFL) sales growth is also impressive. Australian retail LFL sales growth was 4.3%, Australian vet LFL growth was 4.8% and group LFL growth was 4.5%. The group’s click and collect strategy is also working well. On the other hand, Chief Financial Officer, Warwick Thresher, will leave the company in the first half of CY 18. The search for a new Chief Financial Officer in partnership with Heidrick & Struggles is underway. The group is trading in line with the management expectations with FY18 year to date total sales growth of 8.5%.Meanwhile, GXL stock has risen 13.89% in one month as on December 27, 2017. Looking at the catalysts for the next year with footprint expansion continuing and pipeline of in-store clinics and roll out of retail stores as seen in FY18 year to date, we give a “Buy” recommendation on the stock at the current price of $6.00

Network Expansion (Source: Company Reports)

BHP Billiton Limited (ASX: BHP)

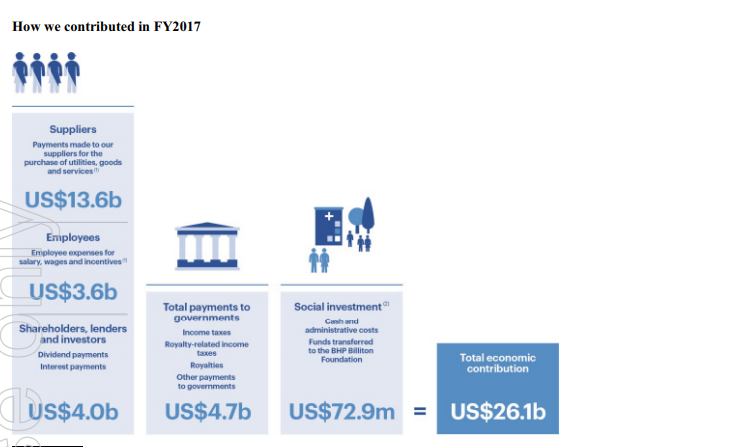

Improved growth prospects: In the recent update, BHP has agreed to fund a total of up US$181 million for financial support for the Renova Foundation and Samarco Mineracao S.A (Samacro) till 30 June 2018 with US$133 million to be used to fund the Renova Foundation so that it can undertake remediation and compensation programs which were identified under the agreement between Samarco and Brazilian Authorities. An amount of US$48 will be made available to Samarco as it will be used to carry out ongoing repair work and will help in supporting the restart plan. The group lately provided Minerals Australia Update and Olympic Dam Briefing wherein productivity gains of US$1.6bn have been identified to be delivered over the next two years. The group will seek Board’s approval for the South Flank project with submission to be made in mid of 2018 and first ore targeted for 2021.The company has made numerous changes to its business model in recent years that seem to have improved its sustainability and profit growth potential. This has helped BHP Billiton to become more focused on its low-cost asset base, where it could have a competitive advantage over many of its industry peers. The group has also benefitted from the commodity price movement, which is expected to continue in the near-term. We recommend a “Buy” at the current price of $29.35

FY17 Contribution (Source: Company Reports)

Collins Foods Limited (ASX: CKF)

Footprint Expansion: Recently, Collins appointed Kevin Perkins as its Non-Executive Director as he retired from his executive role of managing the Sizzler business.Collins Foods’ subsidiary, Collins Restaurants South completed 14 KFC restaurants’ acquisitions in Tasmania from a subsidiary of Yum! Brands Inc. After this, the group needs to acquire four more restaurants as per their plan announced in June 2017. Their Western Australia acquisition and three restaurants in South Australia have been forecasted to finish shortly. CKF’s half year 2018 performance has been mixed with 14% revenue growth and 17.5% fall in statutory net profit while underlying net profit was up 3.7%. On the other hand, the group launched KFC app which is processing over 13,000 transactions each week, while the trial of home delivery has been successful, and the group intends to expand this service soon.They launched the first Taco Bell Restaurant in Queensland whose early trading has been above expectations, and further store openings have been flagged for near and medium term.It has a pay-out ratio of 58.7%, which indicates that the business is re-investing over 40% of its profit to grow future earnings and this is a food for thought. We believe that the subdued levels of the stock can be leveraged given the potential to grow in the coming months. Trading at a decent dividend yield, we give a “Buy” recommendation on the stock at the current price of $5.38

Eclipx Group Limited (ASX: ECX)

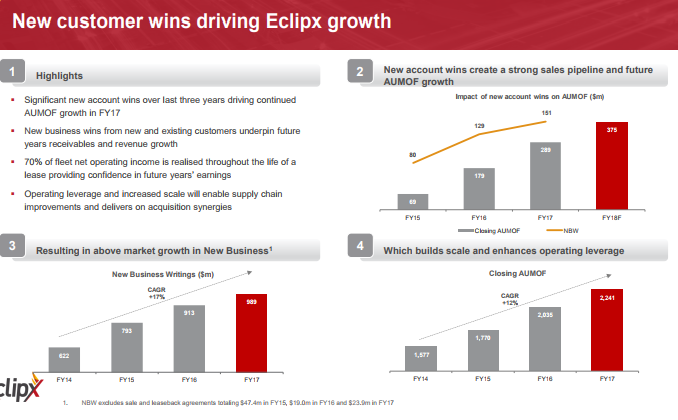

Optimistic Outlook: Recently, Commonwealth Bank of Australia ceased to be a substantial holder of Eclipx Group Limited while Bennelong Funds Management Group Pty Ltd became a substantial holder by grasping 22,766,751 shares and 7.250% of voting power of the Company.In terms of its peers, Eclipx Group produces a yield of 3.7%, which is slightly on the low-side for consumer finance stocks; however, the group is showcasing many catalysts for growth that are expected to provide some boost.The group had paid a total of $29.8 million dividend throughout the year after adjusting for the dividend re-investment plan. The integration of GraysOnline is on track, with the cost rationalization program substantially complete and expected $1 million NPATA contribution to ECX for the period of Eclipx ownership (11 August 2017 to 30 September 2017). ECX has priced its fourth Asset Backed Securities (ABS) issue, the Eclipx Turbo Series 2017-1 Trust; and the transaction has issued a total of A$351.5 million of bonds. The Net Operating Income (NOI) reached 255.3 million, which is a 30% growth rate and it reflects diversification of the business. ECX expects a continuous increase in NOI and NPATA margins due to an increased contribution from Right2Drive and GraysOnline, and has now targeted 27-30% growth over 2017. We give a “Speculative Buy” recommendation on the stock at the current price of $4.23

New Account Wins (Source: Company Reports)

Bapcor Limited (ASX: BAP)

Excellent Growth in key metrics: Bapcor’s performance has exceeded the expectations with FY17 revenue increase to 1,013.6 m from 685.6 m which is up by 47.8%. 23 new stores were in operations across Australia; while the group successfully acquired Hellaby Holdings in New Zealand and post-acquisition it performed well in the second half and also developed Retail franchisee loyalty program and Warehouse Evolution program. As 80% of the business is of trading and wholesale so it involves high service levels and deep specialised product knowledge, and Bapcor also has an option to join Amazon marketplace as it has online capabilities. It has a good track record of delivering earnings growth and total shareholders return; and the group is progressing well on every aspect of its five-year strategic plan.Additionally, BAP will consolidate the recent acquisitions in 2018. The company is on track for FY18 forecast of 30% NPAT growth on continuing operations. Looking at the positive outlook, we put a “Speculative Buy” recommendation on the stock at the current price of $5.68

.png)

Trading Update (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...