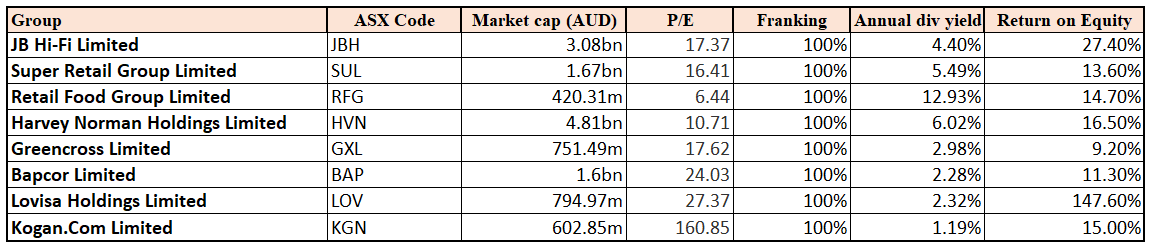

With the release of the healthy retail sales data (1.2% rise in November 2017), many Aussie retailers enjoyed good gains on ASX despite the headwinds or shortcomings seen in the past at sector or company level. Below is a look at 8 stocks relating to the sector and demonstrating some share price movement in the wake of the latest data release.

Stocks’ Summary

JB Hi-Fi Limited (ASX: JBH)

Improving Sentiments: Recently, the Vanguard Group, Inc. became the substantial holder of JB Hi-Fi Limited by holding 5,804,822 shares with 5.04% of the voting power. On the other hand, Challenger Limited ceased its holding since 11 December 2017. Meanwhile, the group has been granted approval for the provision of financial assistance for the acquisition of The Good Guys Discount Warehouses (Australia) Pty Ltd as per Corporations Act 2001. 2017 was a record year as its sales, profits and dividends were all up on the prior year. The group has indicated its ability to bring the brands to life and to create the engagement in various categories. Its business ranked third in the 2017 Australian Market Research Corporate Reputation Index and also has been recognised in the top three in each of the past five years. Market is also expecting the group outperform in its half year results. Though JB Hi-Fi’s operating performance has been healthy and the stock seems to regain the lost momentum as seen last year with the Amazon threat coming into picture, the stock trades at slightly high levels. JBH was up 4.4% on January 11, 2018 with the emanating positive sentiments. Looking at the trading scenario, we give an “Expensive” recommendation at the current price of $27.99

Super Retail Group Limited (ASX: SUL)

Investing in Customer experience: While Macquarie Group ceased to become a substantial holder of SUL group since 14 December 2017, SUL’s financial performance has improved from the prior year. FY17 NPAT increased from $108.6m to $135.8m, which is a 25% change. Its total group sales grew up by 4.1% and its operating cash flow also increased by $75.3 million. Full year dividend of 46.5 cents per share was declared which is up by 12%. Its planned expenditure was $120 million to support the store development program, Amart Sports conversion and also an investment in information systems to support the omni-retailing strategy. SUL has seen a strong growth in digital sector across all the brands, and grew by 75% for the Auto Division, over 150% in the Leisure Division and 73% in the Sports Division. The positive outlook for 2018 and focus on delivering on the strategic pillars and financial targets, seems to reinforce the lost potential. SUL is trying to extend their services to their Supercheap Auto customers to offer solutions and not only products. The stock was up 3.5% on January 11, 2018 along with many other retail stocks at the back of improving sentiments. We give a “Hold” recommendation on the stock at the current price of $8.77

Customer Performance Trends (Source: Company Reports)

Retail Food Group Limited (ASX: RFG)

Slight recovery despite lowering of guidance: RFG also joined the key retailers moving up 3% on January 11, 2018 despite the recent beating at the back of its lowered guidance. The group had lately concluded its new Master Franchise Agreements for the United Kingdom in connection with the Crust Gourmet Pizza and Donut King Brand Systems. Its 1H18 guidance, which was earlier forecasted to demonstrate a statutory NPAT to be circa $22.0 million subject to the timing of the finalisation of new international master license sales and on the risk to franchise earnings. Post finalising certain new master licenses, wherein each of the UK licenses are effective from December 2017, the group has highlighted some variation in the commercial terms to result in a lower NPAT, i.e., below $22.0 million. Amidst these issues, the group had concluded negotiations to extend its three-year debt facilities of $150 million, due to mature in December 2018, into longer dated maturities. We give a “Hold” recommendation on the stock at the current price of $2.37

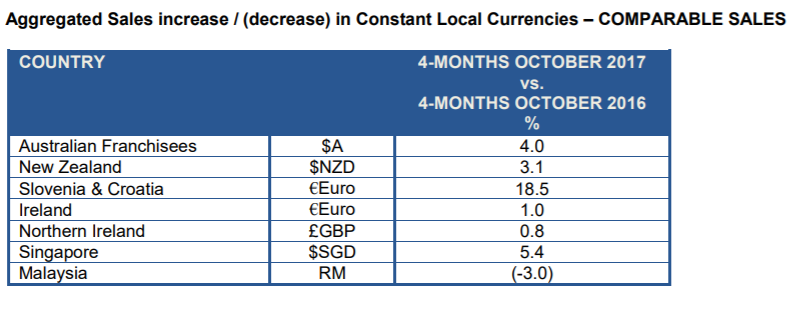

Harvey Norman Holdings Limited (ASX: HVN)

Improving sales trend: Harvey Norman’s stock had slipped by 14.6% in last one year but has been on the uptrend in last three months with a 1.4% rise seen on January 11, 2018. The latest aggregated sales for four months ending October 2017 were boosted by a 1.9% appreciation in the Euro and negatively affected by a 3.2% devaluation in the New Zealand dollar and a 2.2% devaluation in UK Pound for the four months ended 31 October 2017 as compared to the four months ending 31 October 2016. During 2017, the net receipts from the franchisees decreased by $66.77 million as the movement in the aggregate amount of the financial accommodation provided to the franchisees exceeded the movement in the aggregate amount of the financial accommodation provided for 2016. This is aligned with the increase in inventory reserves which are held by purchasing franchisees during the current year in order to drive the franchisee sales revenue and was offset by a $41.40 million increase in the gross revenue from the franchisees. Till we see some more positives with any capability of dominating in the prevailing challenging environment, we give an “Expensive” recommendation on the stock at the current price of $4.38

Sales Performance (Source: Company Reports)

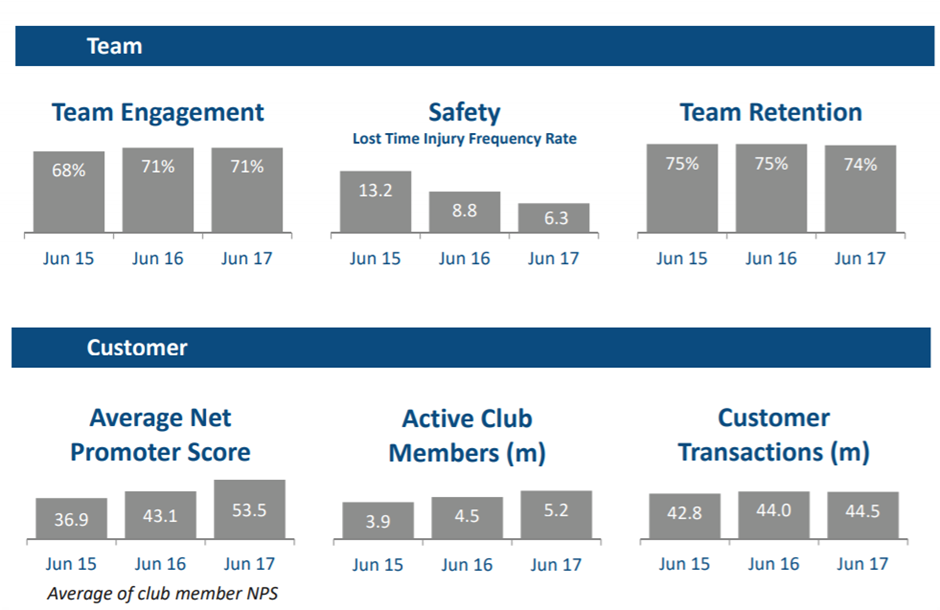

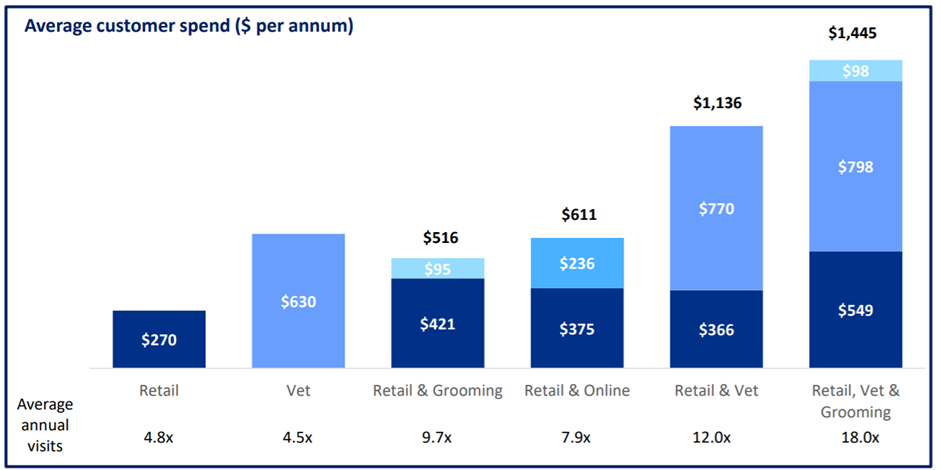

Greencross Limited (ASX: GXL)

Expansion Plans: GXL has been confident on its network runway with a strong pipeline of in-store clinics and continues its focus on online execution and to deliver a seamless omnichannel offering to its customers. Its group revenue for FY17 was up by 11% and the underlying NPAT (post minorities) for FY17 was up by 7% as compared to prior year. The group had added 18 stores and 13 grooming sales in FY17. As of now, it has 1.8 million active customers and over 87% of its purchases were made on its Group Loyalty Program. Its private label sales have reached 21% of its Australian retail product sales. GXL has also sponsored over 7000 pet adoptions and raised over $2.8 million for its charity partners. The group will be adding 15 stores and 20 in-store clinics to the network in FY18, and the growth prospects look decent. We believe that there is some room for upside and give a “Buy” at the current price of $6.40

Customer Spend Trend (Source: Company Reports)

Bapcor Limited (ASX: BAP)

On track to achieve FY18 NPAT guidance: While most of the retailers had a good day on ASX, Bapcor edged lower despite any particular news. On the other hand, BAP’s largest business segment, Aust Trade delivered a FY17 revenue growth of 11% and it increased its EBITDA by 22% on the prior year. The Specialist Wholesale business segment also increased its revenue by 106% while its Retail and Service segment revenue increased by 28%, over FY16. BAP had acquired 100% shares in Hellaby Holdings Limited and post-acquisition it is known as Bapcor New Zealand; and it has planned to deliver between $8million to $11million EBIT of annual benefits per annum by 2020. BAP’s sale of the Footwear and Contract Resources business has been completed by signing a sale agreement for Contract Resources North America and the group is progressing well on the divestment of its remaining non-core businesses.The company is on track to achieve its FY18 forecast of 30% NPAT growth on continuing operations with new company stores driving the retail and Service segment. We put a “Speculative Buy” recommendation on the stock at the current price of $5.62 given the potential.

Lovisa Holdings Limited (ASX: LOV)

Losing some recent gain: Lovisa Holdings announced its first half sales for the six months ending 31 December 2017 entailing a 18.8% growth on last year and up by 7.4% on a comparable store basis. The business enjoyed a strong fashion trends during the first half of FY17-18 and the store network has increased to 319 stores trading at the end of half. It was observed that Lovisa had a disproportionate mix of EBIT weighed to the first half which has also been enhanced by the strong performance of Christmas trade and the Boxing Day sale. The investment in its global rollout continues as it invests in its bench strength while sourcing suitable store locations so as to deliver on-trend products to its customers. Meanwhile, LOV stock still trades at a high level while the investors now seem to be booking some profits (stock down 2.7% on January 11, 2018 post a 12.4% rise in last five days). We give an “Expensive” recommendation at the current price of $7.36

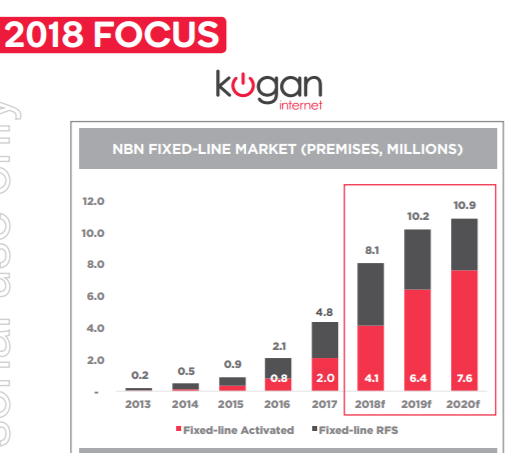

Kogan.Com Limited (ASX: KGN)

Expansion in diverse verticals: Down 3.7% on January 11, 2018, the group lately reported that BlackRock Group ceased to be a substantial holder of Kogan. KGN, on the other hand, entered into an agreement with PetSure (Australia) Pty Ltd which is the wholly owned subsidiary of The Hollard Insurance Company Ltd. It allows to distribute and promote pet insurance policies under a new brand “Kogan Pet Insurance” while focusing on offering a range of affordable pet insurance products. Another agreement has been signed with Medibank Group to offer budget health insurance policies under a new brand “Kogan Health”. We believe that strong FY17 result fundamentals, investment in brands, market opportunity in online retail, and outlook for FY18 with 36.2% growth in revenue for four months from July to October, are still favouring the stock. While some investors might be targeting Kogan for profit booking now, we give a “Hold” on the stock at the current price of $6.21

Fixed-line Market Scenario (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...