The Star Entertainment Group Limited

.png)

SGR Details

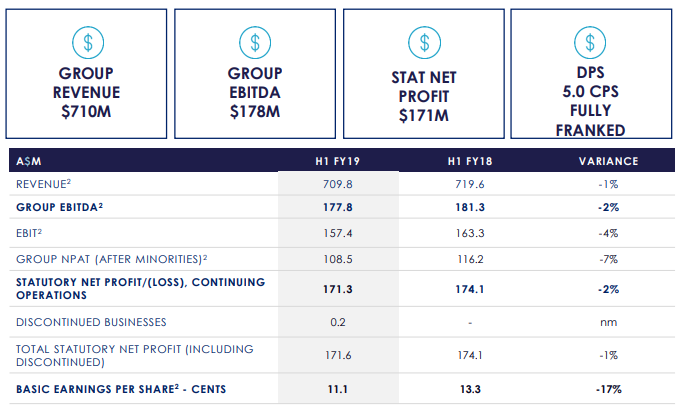

Trading and Earnings Update: The Star Entertainment Group (ASX: SGR) recently provided an update with regards to the trading and expected FY19 earnings by the issuance of the press release. The company added that the domestic revenue growth trends throughout The Star properties have softened since the release of the company’s 1H FY19 results, and the domestic revenue between January 1 and June 8, 2019 witnessed a rise of 0.3% on pcp basis. The total domestic revenue in FY 2019 YTD (till June 8, 2019) encountered a rise of 3.1% on pcp basis. Considering the revenue growth rates, The Star is expecting FY19 normalised EBITDA to be in the ambit of $550-560 million. However, it was also mentioned that all the financials and the final result will be subject to the end of year finalisation processes and external audit of FY19 financial statements. Below picture provides a broader overview of the company’s performance in 1H FY19:

.png)

Highlights (Source: Company Reports)

The company also stated that the announced creation of the centres of excellence in Gaming and Marketing enables it to improve the capability, processes and decision-making.Considering the current revenue environment, the initiatives to deliver the cost savings have been brought forward, the company has been targeting $40-50 million per annum cost savings run rate to be achieved by 1Q FY 2020 end.

Respectable Position of Key Margins: The company is having respectable position in its key margins as its net margin stood at 12.9% in 1H FY19, which is higher than the industry median of 10.4%. The company’s EBITDA margin stood at 28.8% while the industry median stood at 26.3%. The company’s Debt/Equity ratio stood at 0.26x, which is lower than the industry median of 0.47x and, thus, it looks like that the company has less exposure towards debt component as compared to the broader industry.

Stock Recommendation: The stock of SGR has delivered the return of 24.10% in the span of previous five years. As per the ASX, the company’s stock is trading towards the 52-week lower levels and, thus, it can be said that the stock is providing a good opportunity for accumulation. Hence, considering the respectable position of the margins and the annual dividend yield, lesser exposure towards debt (as mentioned) and current trading levels, we give a “Buy” rating on the stock at the current market price of A$4.140 per share (up 0.485% on 31 July 2019).

SGR Daily Chart (Source: Thomson Reuters)

BlueScope Steel Limited

.png)

BSL Details

Market Update on Earnings:BlueScope Steel Limited (ASX: BSL) recently made an announcement that it is expecting its FY19 underlying EBIT approaching towards $1,350 million, which happens to be an increase of around 6% on FY18 as well as it implies 2H FY 2019 underlying EBIT approaching towards $500 million. The company stated that key changes since the prior guidance is associated with the North Star, Building Products Asia, and North America as well as Buildings North America. The company added that the other businesses have been performing generally in-line with expectations and Australian Steel Products is witnessing stronger realised steel spreads which are being offset by the weaker than anticipated domestic volumes. The company happens to be committed towards its stated financial principles and disciplined approach to capital allocation. The following picture provides a brief overview of 1H FY19 performance:

.png)

1H FY19 Headlines (Source: Company Reports)

Buy-Back Event Update: As per the release dated 15 July 2019, the company has bought back a total of 2,30,35,561 shares via on-market trade for the total consideration of A$ 28,89,67,832.56 and intends to buy back remaining shares with an aggregate consideration of A$211,032,167.44 out of A$500 Mn. As per the release of buy back share, dated 31 July 2019, the company lodged Form 484 with ASIC for cancellation of 2,440,317 shares acquired under Share Buyback event announced on 3 December 2018.

YoY Improvement in Key Margins: The company’s key margins witnessed a YoY improvement in 1H FY19, which reflects that the company has been improving its financial standing. The net margin of 1H FY19 stood at 10%, reflecting an improvement of 2% on YoY basis. However, EBITDA margin stood at 15.5% in 1H FY19, which implies YoY improvement of 3.8%. The company’s current ratio stood at 1.89x, which is an improvement of 4.2% on YoY basis and reflects improved liquidity position.

Stock Recommendation: In the span of previous one month, the company’s stock has delivered the return of 7.35% while, in the time span of past six months, the stock’s return stood at 6.39% which can be considered at respectable levels. Currently, the company’s stock is trading below the average of 52 weeks high and low price of $10.305 and $18.830, respectively, indicating a decent opportunity for accumulation. Hence, considering the improvement in the key margins, respectable liquidity levels, annual dividend yield and current trading levels, we give a “Buy” rating on the stock at the current market price of A$13.090 per share (down 0.456% on 31 July 2019).

BSL Daily Chart (Source: Thomson Reuters)

Super Retail Group Limited

.png)

SUL Details

Appointment of Managing Director, BCF: Super Retail Group (ASX: SUL) has recently made an announcement about the appointment of an experienced retail leader named Paul Bradshaw as the Managing Director of outdoor business, BCF. The company added that he would be commencing on November 25, 2019 and he would be sitting on the company’s Executive Leadership Team.In the Macquarie Conference 2019 presentation, the company provided information about the trading update and stated that its Auto retailing business witnessed like for like sales growth of 4.2% in first 17 weeks of the H2 FY19 while on a YTD basis (i.e., to April 27, 2019), the growth was of 2.7%.

The overall group witnessed a like for like sales growth of 3.3% on a YTD basis to April 27, 2019. The following picture provides a brief overview of the sales by channel and customers by channel (with respect to Omni-retail platform) for the 12 months to April 2019:

.png)

Omni-retail platform (Source: Company Reports)

What Could Support SUL Moving Forward: The company’s 3 core brands have been enjoying the market-leading customer loyalty performance, and it also stated that the Macpac happens to be an emerging and credible brand in high growth segment. The company’s RoE stood at 9.1% at the end of December 2018, which is higher than the industry median of 8.5% and, thus, it can be said the company is providing higher returns to its shareholders, which might help it in gaining traction among the market participants.

Stock Recommendation: In the span of previous six months, the company’s stock has delivered the return of 27.38% while, in the time frame of past one month, the return stood at 11.44% which can be considered at respectable levels. As per ASX, the company’s annual dividend yield stood at 5.24%, which is higher than the industry average of 4.6%, thus, the stock can be considered for the dividend-seeking investors. Hence, considering the decent fundamentals and business prospects, we give a “Buy” recommendation on the stock at the current market price of A$9.000 per share (down 3.743% on 31 July 2019).

SUL Daily Chart (Source: Thomson Reuters)

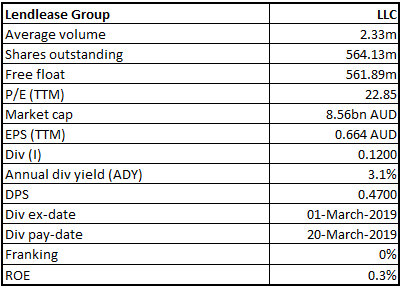

Lendlease Group

LLC Details

Agreement with Google: Lendlease Group (ASX: LLC) recently made an announcement that it entered into the agreement with Google in the United States in order to develop the company’s landholdings in San Jose, Sunnyvale and Mountain View into the mixed-use communities. LLC estimates that it would be developing up to 15 million square feet of the residential, retail, hospitality, and other associated community uses in new neighborhoods. It was also stated that Google would be focusing on developing its office space within these mixed communities.

Not so long ago, the company has also provided information on the global trends which are influencing its strategy. These include urbanisation, infrastructure, ageing population, funds growth, etc. The company added that its globally diverse pipeline provides long-term earnings visibility. The following picture provides an overview of the construction segment:

Construction Segment (Source: Company Reports)

What Could Help LLC Moving Forward: The company stated that it is laying the foundations for future growth. The company has been focusing towardsleveraging its competitive advantage through the integrated model, urbanisation projects as well as investments platform. Additionally, it was added that the diversification throughout segment, sector and geography provide resilience which could help the company’s performance moving forward.

Stock Recommendation: The company’s stock has delivered the return of 14.06% in the span of previous one month, while in the time frame of past six months, the stock’s return stood at 23.23% which can be considered at respectable levels. The company’s current ratio stood at 1.02x, which reflects a marginal rise of 0.2% on a YoY basis and, thus, it can be said that the company’s liquidity levels have been improved which might help the company to make deployments towards strategic objectives. Considering that the company is focusing on leveraging competitive advantage and respectable liquidity levels (as can be seen from the current ratio), we expect the company holds potential for further growth. Thus, we give a “Buy” recommendation on the stock at the current market price of A$14.550 per share (down 4.087% on 31 July 2019).

LLC Daily Chart (Source: Thomson Reuters)

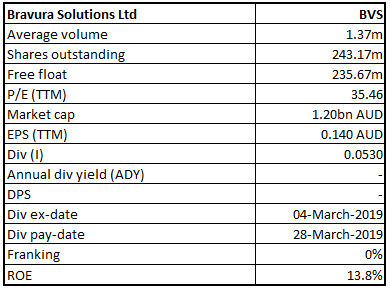

Bravura Solutions Limited

BVS Details

Update Related to GBST: Bravura Solutions Limited (ASX: BVS) has recently referred to the announcement related to the updated proposal announcement and confirms that as at 4 pm on June 28, 2019 it had not executed Process and Exclusivity Deed with GBST Holdings Limited. Bravura did not make and has withdrawn the preparedness to make, the updated proposal. Also, not so long ago, the company made an announcement about the completion of A$165 million fully underwritten institutional placement of around 28.7 million shares involving final issue price of A$5.75 per new share. The following picture provides an overview of the company’s revenue and EBITDA:

Revenue and EBITDA (Source: Company Reports)

Fall in Debt/Equity Ratio: The company’s EBITDA margin stood at 19.5% in 1H FY19, which reflects a rise of 0.8% on a YoY basis. Also, the company’s liquidity levels have witnessed an improvement and its current ratio stood at 0.94x, which reflects a rise of 10.4% on a YoY basis and, thus, it can be said that the company would be able to meet its short-term obligations. Also, respectable liquidity levels can help BVS in making deployments towards strategic business activities. The company’s Debt/Equity ratio stood at 0.10x, which reflects a fall of 24.1% on a YoY basis.

Outlook and Stock Recommendation: The company’s stock has delivered the return of 19.57% in the span of previous six months while, in the time frame of past one month, the stock’s return stood at 3.56%, which can be considered at respectable levels. The company stated that it is well-positioned to take advantage of robust demand in the UK, Australia, New Zealand, South Africa and Asia. Additionally, it was mentioned that the robust growth, increasing scale and greater efficiency have been driving the increased operating leverage, which could help the company over the long-term. Considering the above-stated facts, we presume that the company is possessing the potential for growth in the long-run. Hence, we give a “Buy” rating on the stock at the current market price of A$4.920 per share (down 0.606% on 31 July 2019).

BVS Daily Chart (Source: Thomson Reuters)

Oil Search Limited

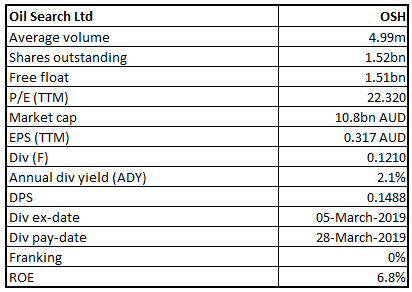

OSH Details

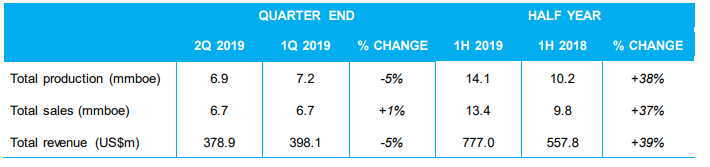

Announcement of Results for Second Quarter: Oil Search Limited (ASX: OSH) recently released its results for the second quarter report for the period ended June 30, 2019 in which it stated that PNG LNG project records robust performance despite the scheduled downtime for the maintenance. The company added that the total production for Q2 FY19 stood at 6.9 mmboe. It was also stated that in June, Hon James Marape was sworn in as new Prime Minister of PNG, after the resignation of Peter O’Neill. During the second quarter, the commercial agreements that govern Papua LNG Project’s access to the PNG LNG Project site and infrastructure were wrapped up and are ready for the execution.

Second Quarter (Source: Company Reports)

The company also has decent financial position and, as at June 30, 2019, the company had liquidity of US$1.44 billion, which is comprised of US$538.3 million in cash and US$900 million in the credit facilities.

What To Expect From OSH Moving Forward: As per the reports, 1H FY19 results have been scheduled to be out August 20, 2019. The company added that the production costs are anticipated to be in the ambit of US$12 - 13 per boe for 1H FY19 and US$11 - 12 per boe for 2019 full year. However, the full year normalised unit production costs, excluding the financial impact of earthquake, are expected to be in the range of US$9 - 10 per boe.

Stock Recommendation: The company’s stock has witnessed an increase of 2.02% on a YTD basis. However, in the span of the previous one month and three months, the company’s stock has witnessed a fall of 0.98% and 9%, respectively. As per ASX, the company’s stock is trading towards its 52-week lower levels and, thus, it looks like that the current trading levels are offering respectable opportunity to buy the stock. Hence, considering the aforesaid facts coupled with current trading levels and keeping an eye on the company’s 1H FY19 results (which are due to be out on August 20, 2019), we give a “Buy” rating on the stock at the current market price of A$7.110 per share (up 0.424% on 31 July 2019).

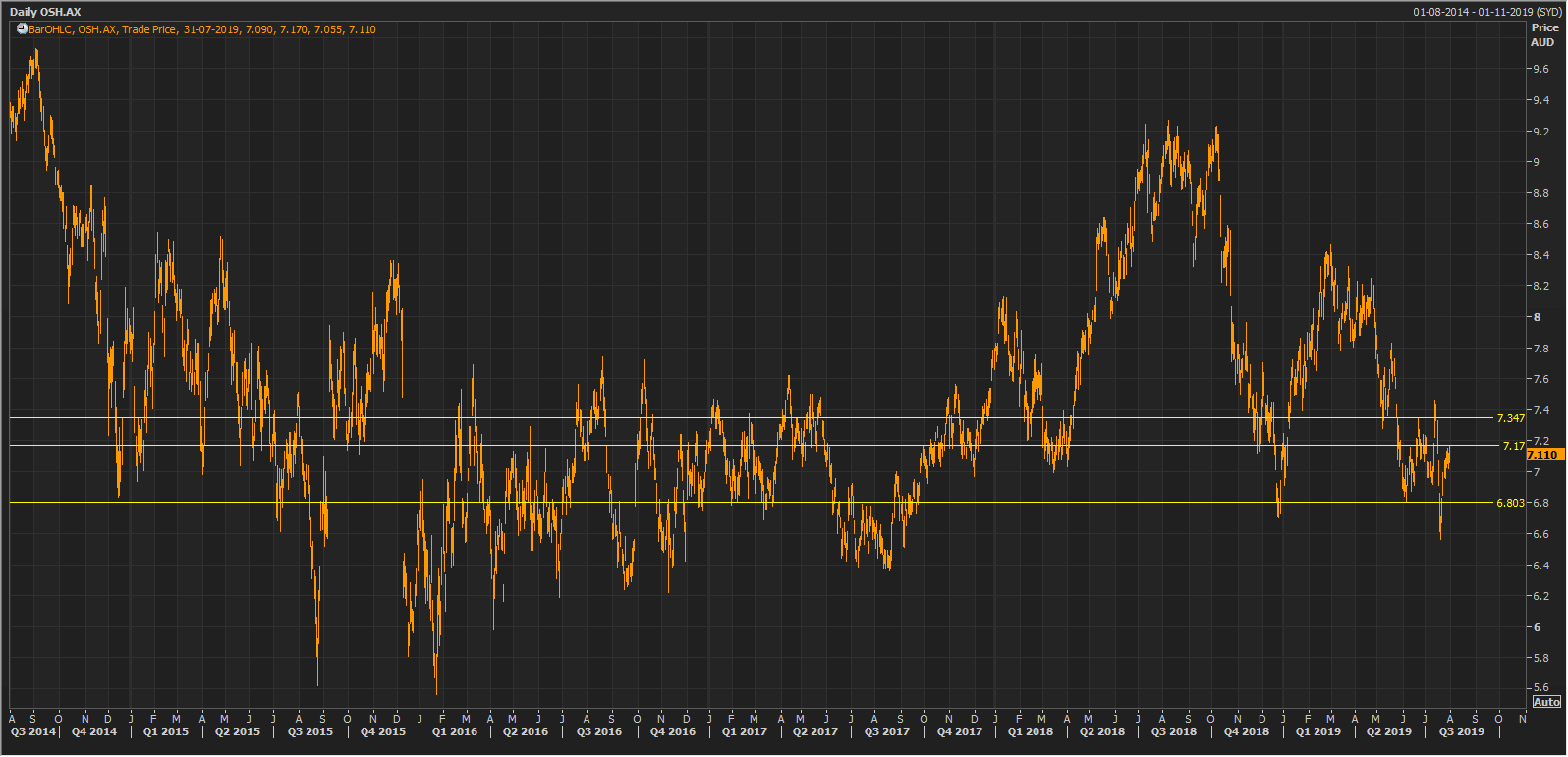

OSH Daily Chart (Source: Thomson Reuters)

Nine Entertainment Co. Holdings Limited

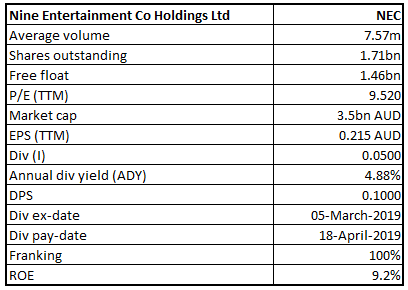

NEC Details

Announcement About Completion of ACM Sale: Nine Entertainment Co. Holdings Limited (ASX: NEC) has recently announced that it has wrapped up the sale of Australian Community Media and Printing (or ACM) to the company controlled by the interests associated with Antony Catalano and Thorney Investment Group.The company got cash proceeds of $105 million, with the further $10 million to be received in the twelve months. The company added that there is an intention that these funds would be deployed towards the reduction of group indebtedness. The following picture provides a broader overview of the company’s 1H FY19 results:

Reported Results (Source: Company Reports)

What Could Support NEC Moving Forward: The company’s key margins have witnessed a YoY improvement in 1H FY19, which builds further confidence in the company’s core business activities. The company’s EBITDA margin stood at 50.8% at the end of December 2018, which reflects a YoY rise of 27.4%. Also, the company’s operating margin stood at 29.9%, which reflects a rise of 9% on a YoY basis. The company’s current ratio stood at 1.78x, which can be considered at respectable levels and looks like that the company would able to meet its short-term obligations moving forward. Also, respectable liquidity levels provide sufficient headroom to make deployments towards growth initiatives.

Stock Recommendation: The company’s stock has delivered the return of 38.98% in the span of previous six months, while in the time frame of past three months, the stock’s return stood at 17.14% which can be considered at respectable levels. Additionally, the company would bereleasing the FY19 results on August 22, 2019 and we advise the investors to track the same. Additionally, it can be said that the company is focusing on reducing the group indebtedness (as mentioned above).

Hence, considering the above-states facts coupled with respectable annual dividend yield as compared to the border industry and current trading levels, we give a “Buy” rating on the stock at the current market price of A$2.020 per share (down 1.463% on 31 July 2019).

.png)

NEC Daily Chart (Source: Thomson Reuters)

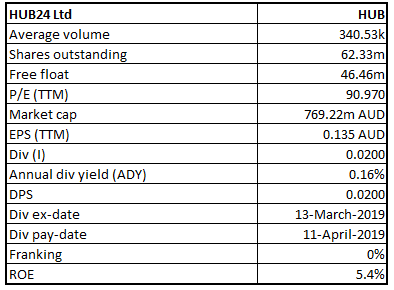

HUB24 Limited

HUB Details

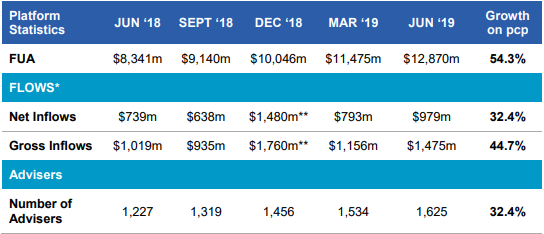

June ’19 Quarter Net Inflows increased by 32.4% on pcp: HUB24 Limited (ASX: HUB) recently announced the issuance of 260,000 Fully Paid Ordinary shares (FPO) on the same terms as existing issued FPO of HUB24 Limited and are subject to sales restrictions of 12 months except to fund exercise cost or tax associated with the options.The FPO shares are issued as the result of the exercise of 160,000 options at $0.98 per option, 50,000 options at $2.46 per option and 50,000 options at $3.98 per option. In another update, HUB announced that its substantial holder, ECP Asset Management Pty Ltd (and its associated entities) increased its voting power from 5.38% to 6.60%.

June ’19 Quarter Key Highlights: The net inflows for the quarter was reported at $979 Mn, which is 32.4% up as compared to the previous corresponding period. The Funds under administration for the quarter increased by 54.3% on pcp to $12.9 Bn. During the quarter, HUB24 platform continued to grow at the fastest rate in the industry and was ranked second place for both quarterly and annual net inflows in the latest available Strategic Insights data. It secured new agreements with two large national advice groups, Madison Financial Group and Centrepoint Alliance.

June ’19 Quarter Fund Inflows Data (Source: Company Reports)

What to expect: HUB continues to broaden its managed portfolio menu to support the needs of its clients. In the June quarter, it launched 21 new portfolios on the platform, 6 of which were tailored for specific advice groups. It launched Sargon Small APRA Fund Service utilising HUB24’s platform technology, in order to provide investment solutions for all segments of the market. All these developments are expected to help the company is delivering sustainable value for its shareholders.

Stock Recommendation: Its ROE for H1FY19 stood at 5.4%, better than the industry median of 2.5%, which implies the company delivered a decent return to its shareholders than its peer group. Its current ratio for H1FY19 stood at 2.76x, better than the industry median of 1.50x, which implies the company is in a better position to address its short-term obligations than its peer group. Currently, the stock is trading slightly below the average of 52 weeks high and low price of $9.855 and $15.550, respectively, proffering a decent opportunity for accumulation.Hence, considering the aforesaid facts and current trading level, we recommend a “Buy” rating on the stock at the current market price of $12.440 per share (up 1.221% on 31 July 2019).

HUB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...