The A2 Milk Company Limited

.png)

A2M Details

Significant Rise in EBITDA: The A2 Milk Company Limited (ASX: A2M) is a premium branded dairy nutritional company, focused on products containing the A2 beta-casein protein type. In the recently held AGM, the company reported strong momentum in performance, wherein revenue increased to NZ$1,304.5 million in FY19 from NZ$922.7 million in FY18. During the year, Group EBITDA (Earnings before Interest, Taxes, Depreciation and Amortisation) also went up to NZ$413.6 million from NZ$283 million.This resulted in the EPS to rise from 27 cents in FY18 to 39.3 cents in FY19.

.png)

Financial Performance (Source: Company Reports)

What to Expect: The company expects a strong revenue growth across its key regions. In 1H FY 2020,

the company is anticipating revenue to come between $780 million to $800 million.For FY 2020, it expects a stronger EBITDA margin, which is expected to come between 29%-30% with gross margin benefiting from improved price yield and reduction in COGS (Cost of Goods Sold).For the first half of 2020, the company expects EBITDA margin to come in the range of 31-32%.

Stock Recommendation: During the time span from FY15 to FY19, the company witnessed a CAGR growth of 70.37% in revenue and a CAGR growth of 90.32% in gross profit. As per the ASX, stock of A2M gave a return of 20.73% in the past one month. EBITDA margin of the company stands at 32.3% in FY 2019, higher than the industry median of 12.5%. During the year, ROE stood at 42.8% as compared to the industry median of 12.8%. This indicates that the company is delivering decent returns to its shareholders. Thus, considering higher EBITDA margin, a decent return on equity, CAGR in gross profit and modest outlook, we recommend a “Buy” rating on the stock at the current market price of $14.770 per share, up by 1.862% on November 29, 2019.

A2M Daily Technical Chart (Source: Thomson Reuters)

Bubs Australia Limited

.png)

BUB Details

Record Gross Revenue: Bubs Australia Limited (ASX: BUB) offers organic baby food, goat milk infant formula products, adult goat milk powder products and fresh dairy products. The top management of the company addressed its shareholders in the recently held AGM 2019 and stated that the company has delivered strong growth in revenue, delivering a near tripling of gross revenue to $46.8 million. This was mainly underpinned by growth coming from Bubs® goat milk infant formula range. The domestic sales figure increased to $35.7 million and was mainly supported by marketing initiatives to raise brand awareness and increased store count in Coles and Woolworths.

.png)

Group Revenue Growth (Source: Company Reports)

What to Expect:The company is well placed to pursue its strategic goals towards delivering profitable, scalable and sustainable growth. For FY20, the key focus of the company is to achieve margin improvement to 40% across Bubs® portfolio in the near-term. The Southeast Asia baby food market is growing rapidly and is expected to grow to US$8 billion by 2023.

Stock Recommendation: During the time span from FY16 to FY19, the company saw a CAGR growth of 122.71% in gross profit. In the past 5 years, EBITDA margin and net margin improved significantly, and current ratio of the company stood at 2.03x, higher than the industry median of 1.42x. This indicates that the company is capable of paying its current liabilities using its current assets. Thus, considering decent revenue growth, improving margins and modest outlook, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.080 per share, down by 1.37% on November 29, 2019.

BUB Daily Technical Chart (Source: Thomson Reuters)

Tribune Resources Limited

.png)

TBR Details

Considerable Increase in NPAT: Tribune Resources Limited (ASX: TBR) is primarily engaged in the exploration, development and production activities at the Group’s East Kundana Joint Venture tenements. The company has recently released its quarterly report for September 2019, wherein it stated that 236,766 tonnes of EKJV ore was processed at the Kanowna Plant, 30,454 tonnes of EKJV ore and 0 tonnes of R&T ore were processed at the Greenfields Mill. During the year, revenue of the company went up to $364.67 million from $179.92 million in FY18.This resulted in NPAT (Net Profit After Tax) to increase from $54.4 million in FY18 to $72.26 million in FY19.

.png)

Financial Performance (Source: Company Reports)

Stock Recommendation: The Group intends to continue its exploration, development and production activities on its existing projects and to acquire further suitable projects for exploration as and when opportunities arise. The company’s P/E ratio stood at 9.630x as compared to the industry average (Basic Materials) of 49.6x. As per the ASX, the stock of TBR gave a return of 49.97% in the past six months and has witnessed a CAGR growth of 42.78% in gross profit in the time span of 5 years from FY15 to FY19. During the year, EBITDA margin of the company stood at 43.4%, higher than the industry median of 29.1%. Net margin of the company was 19.8% as compared to the industry median of 11.7%. Thus, in the backdrop of higher returns, high EBITDA and net margins, decent profitability position, and favourable valuation metric, we recommend a “Buy” rating on the stock at the current market price of $6.310 per share, up by 0.478% on November 29, 2019.

TBR Daily Technical Chart (Source: Thomson Reuters)

South32 Limited

.png)

S32 Details

Record Production at Brazil Alumina:South32 Limited (ASX: S32) is a globally diversified mining and metals company. The company has recently announced that it has entered into a binding conditional agreement for the sale of its 91.835% shareholding in South32 SA Coal Holdings Proprietary Limited to Thabong Coal Proprietary Limited and two trusts, a community trust and an employee trust who will respectively acquire 81.835%, 5% and 5% of the shares in SAEC (or South Africa Energy Coal). Seriti Resources Holdings Proprietary Limited will make an up-front cash payment of approximately 100 million South African Rand to acquire S32’s shares in SAEC. As on September 2019, net cash of the company increased by US$163 million to US$527 million, following the allocation of a further US$74 million to its on-market share buy-back. The company has achieved record production at Brazil Alumina and has increased production at Illawarra Metallurgical Coal by 30% as the longwalls continued to perform strongly following the completion of two moves in the prior quarter.

.png)

Production Summary (Source: Company Reports)

What to Expect: The Group’s production volumes are expected to rise by 3% in FY20. Group and unallocated costs are expected to come in at US$90 million, owing to an increase in functional support for its development projects and investment in technology to support operations. Sustaining capital expenditure is expected to rise by US$82 million to US$515 million due to increased underground development rates and expenditure on infrastructure improvements at Illawarra Metallurgical Coal.

Valuation Methodology: EV to Sales based Valuation

.png)

EV /Sales Multiple Valuation (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the stock of S32 gave a return of 3.47% in the last one month and is trading towards its 52-week low level of $2.360.During the time span from FY15 to FY19, the company witnessed a CAGR of 28.43% in gross profit. During the year, gross margin of the company stood at 67.3%, higher than the industry median of 41.1%. Considering the positive returns, CAGR in gross profit and high gross margin, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple and arrived at a target price of lower double-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.70, up 0.746% on 29 November 2019.

S32 Daily Technical Chart (Source: Thomson Reuters)

Amcor Plc

.png)

AMC Details

Decent Performance in FY19:Amcor Plc (ASX: AMC) is in the development and production of rigid and flexible packaging for a variety of food, beverage, pharmaceutical, medical-device, home and personal care etc. As per the 2019 annual report, the company has performed well in the FY19 with momentum building in numerous key metrics. AMC experienced a rise of 5.5% in net sales. Adjusted net income was up by 9% in constant currency terms and compared with last year due to marked improvements in working capital. Its adjusted cash flows after dividends were US$193 million.

.png)

Key Financial Metrics (Source: Company Reports)

What to Expect:The strategies of the company revolve around (1) Focused portfolio, (2) Differentiated capabilities, and (2) Aspiration to be THE leading global packaging company. The additional strategic investments would finance numerous initiatives, which include research and development infrastructure, manufacturing equipment, extensions to the company’s current partnership network, and investments in open innovation.

Stock Recommendation:The company possesses a roadmap of innovative products moving from R&D to commercialisation, which includes a growing range of high-barrier flexible packaging designed to be recyclable and reduce carbon emissions of transportation and the carbon footprint of products. The company will be paying its distribution amount of USD 0.11500000 on 17th December 2019. Current ratio of the company stood at 1.15x in FY19, reflecting YoY growth of 60.2%. This reflects that the company has improved its position to address its short-term obligations against the broader industry. The stock of AMC generated returns of 8.28% and 4.65% in the time span of one month and three months, respectively. Thus, considering the company’s strong financial profile, unique combination of talented people, differentiated capabilities, decent liquidity levels, and scale and global reach which provides powerful competitive advantages, we give a “Buy” recommendation on the stock at the current market price of A$15.250 per share, down 0.327% on 29th November 2019.

AMC Daily Technical Chart (Source: Thomson Reuters)

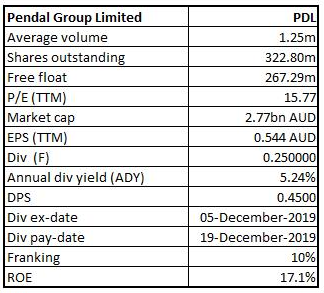

Pendal Group Limited

PDL Details

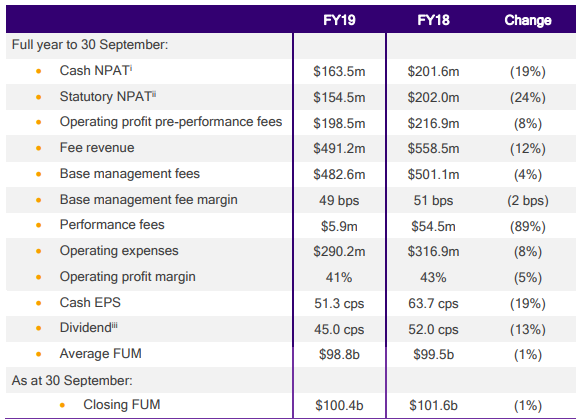

A Quick Look at FY19 Results:Pendal Group Limited (ASX: PDL) is in the business of global asset management with a market capitalisation of A$2.77 Bn as on 29th November 2019. The company has scheduled to conduct its 2019 Annual General Meeting on 13th December 2019. For the 12 months to 30th September 2019, the company reported a statutory net profit after tax amounting to $154.5 million against $202.0 million for the previous year. FY19 result was characterised by significantly lower performance fees, which witnessed a decline of 89% from $54.5 million in the pcp to $5.9 million.

Financial Performance (Source: Company Reports)

Future Aspects:PDL stated that the financial strength and strong cash flow places the company well to invest for growth and take advantage of opportunities, despite a more difficult year, which was influenced by global trade tensions as well as continued uncertainty around Brexit.

Stock Recommendation:The Board of the company declared a final dividend amounting to 25.0 cps. This brought the total dividends for the year to 45.0 cents per share, reflecting a fall of 13% on pcp. The final dividend would be 10% franked, and PDL will pay a dividend on 19th December 2019 at the record date of 6th December 2019. The stock’s EV/Sales multiple stood at 5.6x on TTM basis as compared to industry median (Financials) of 6.1x. PDL’s stock has a P/B multiple of 3.0x while the industry average (Investment banking & Investment Services) is 3.9x. Thus, considering decent outlook, valuation parameters and respectable growth prospects, we give a “Buy” recommendation on the stock at the current market price of A$8.560 per share, down 0.233% on 29th November 2019.

PDL Daily Technical Chart (Source: Thomson Reuters)

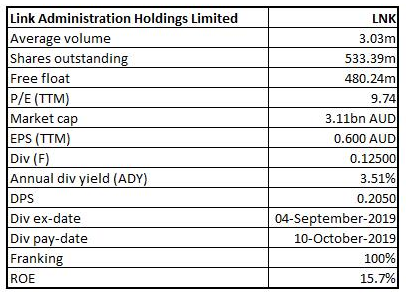

Link Administration Holdings Limited

LNK Details

Update on Share Buyback:Link Administration Holdings Limited (ASX: LNK) is a technology-enabled administrator of financial ownership data. The market capitalisation of the company stood at A$3.11 Bn as on 29th November 2019. Recently, the company announced that it has bought back 1,452,801 shares at the consideration of $8,158,746, pursuant to its daily share buy-back notice. The company would release its 1H FY20 results on 17th February 2020. In FY19, the company’s revenue amounted to $1.4 Bn, with a rise of 17% in comparison to the previous year.

Revenues (Source: Company Reports)

Future Guidance:The company stated that the global transformation program is on track, and it is expected to deliver $50 million of annual cost savings by the end of FY2022. For FY20, Operating EBITDA of the continuing business is anticipated to be stronger in the second half, broadly in-line with FY 2019.

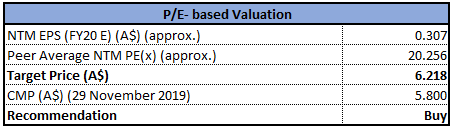

Valuation Methodology:PE-Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation:Gross margin of the company stood at 92.2% in FY19, which is higher than the industry median of 76.2%. Net margin of LNK stood at 22.8% in FY19 as compared to the industry median of 17.8% and, thus, it can be said that its capabilities to convert the top-line into bottom-line are better as compared to the broader industry. Return on equity of LNK stood at 15.7%, reflecting YoY growth of 4.4%. Recently, LNK has also formed a strategic global partnership and a minority investment in Smart Pension. The partnership with Smart Pension gives LNK a decent and credible market entry point into the fast-growing UK pension administration market. The partnership will also boost LNK’s leading presence in Australian and New Zealand superannuation markets.

Considering the aforesaid facts, we have valued the stock using price to earnings multiple and arrived at a target price of lower single-digit growth (in % terms). Therefore, in light of the growth in key margins, partnership with Smart Pension, and with the facts that global transformation program is on track, we give a “Buy” recommendation on the stock at the current market price of A$5.800 per share, down 0.685% on 29th November 2019.

LNK Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...