Stocks’ Details

Domino's Pizza Enterprises Ltd

Forecasting a weaker scenario: Domino's Pizza Enterprises Ltd (ASX: DMP) reported that they expect a weaker than expected first half of 2018 performance at the back of the rollover of last year’s strong Same Store Sales growth in ANZ and foreign exchange weakness in Japan and New Zealand. For ANZ, the group expects a Same Store Sales growth of 7 to 9% for FY18. However, they forecast a limited of +0-2% Same Store Sales Growth in Japan for the full year. Overall, DMP slightly upgraded their Same Store Sales growth guidance at 6-8% for FY18 while forecasts underlying NPAT to rise about 20% for the year. DMP stock corrected over 22.6% in the last six months (as of November 08, 2017) and lost 3.5% on November 09, 2017; and still trades at a very high P/E. It is also noted that the Fair Work Commission has terminated Domino’s agreements which were paying staff wages below the stipulated amount, and settled on a 12-week transition indicating that in absence of a new agreement, the employees will be paid according to the award from 24 January 2018. We give an “Expensive” recommendation on the stock at the current price of $46.43

Santos Ltd

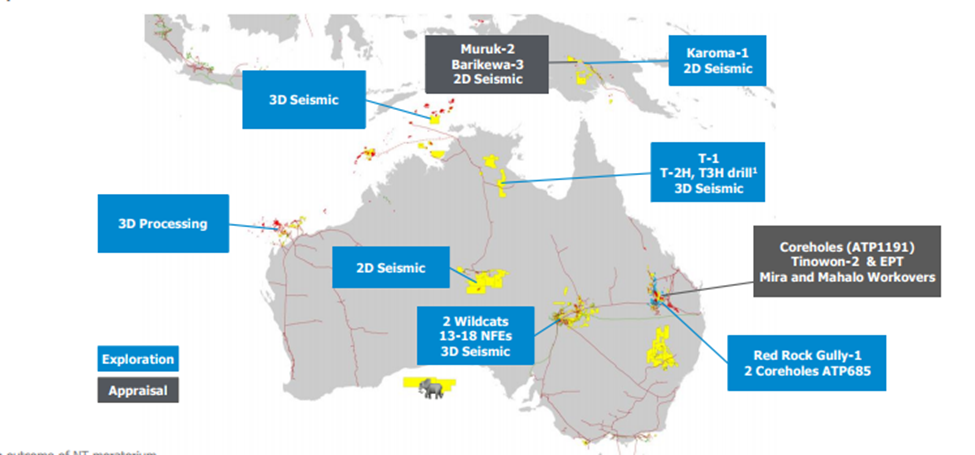

Cost control efforts paying well: Santos Ltd.’s (ASX: STO) stock plunged 2.7% on November 09, 2017 while the company is aiming for a free cash flow breakeven at US$32/bbl for 2017 which is a significant decrease from US$47/bbl, as discussed during the Investor Day. STO controlled upstream unit production costs by 22% with support from its Transform-build-grow strategy. They also cut 42% and 72% in Cooper Basin and GLNG average well costs, respectively. STO decreased net debt by 40% to US$2.8 billion while targeting $2 billion by the end of 2019. The 2017 production and sales volumes are expected to be towards the upper end of the 58-60 mmboe and 79-82 mmboe guidance ranges, respectively. The stock rallied over 39.4% in the last three months (as of November 08, 2017) and we believe there is still some room for growth. Specifically, stable base production for the next decade can lead to major growth opportunities. We give a “Hold” recommendation on the stock at the current price of $4.65

2018 Exploration & appraisal program (Source: Company reports)

James Hardie Industries Plc

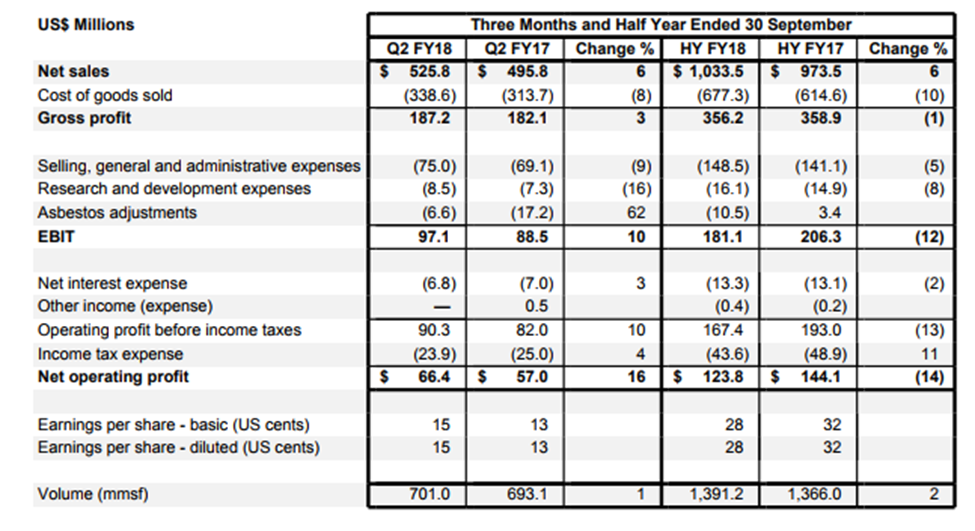

Mixed result: Building material supplier, James Hardie Industries Plc (ASX: JHX) reported an adjusted net operating profit of US$73.9 million for the second quarter of FY18 and US$135.6 million for the half year, which is a fall of 1% and 4%, respectively on a yoy basis. The group’s first half-net profit fell by 14% owing to manufacturing inefficiencies and higher productions costs. JHX otherwise reported a net sales rise of 6% year on year (yoy) to US$525.8 million for the quarter. North America Fiber Cement Segment volume fell 2% for the quarter and was flat during the half year against prior corresponding period. On the other hand, the North America Fiber Cement Segment net sales rose 4% yoy to US$398.1 million during the quarter and EBIT margin reached 24.5% while International Fiber Cement Segment EBIT margin reached 24.9% during the quarter. JHC stock rallied over 6.8% in the last four weeks (as of November 08, 2017) and was up 7.6% on November 09, 2017. We believe it would be better to look for more prospects given the purchase of German-based Fermacell for the fibre cement products business in Europe. We give an “Expensive” recommendation on the stock at the current price of $20.39

Second quarter of FY18 performance (Source: Company reports)

Nufarm Ltd

Acquiring European herbicide product portfolio from FMC: Nufarm Ltd (ASX: NUF) is acquiring a European cereal broadleaf herbicide portfolio from FMC Corporation for US$85 million in cash, plus over US$5 million for inventory. This deal would complement Nufarm’s existing European portfolio and the Century Portfolio (which Nufarm is in the process of acquiring). The Portfolio is forecasted to contribute net sales of over A$30 million and EBITDA of over A$15 million in the 2019 financial year. NUF stock rose over 5.3% on November 09, 2017 and we believe the stock is trading at slightly high levels. It is also uncertain whether the recent acquisitions will be dilutive to the earnings profile. We rate the stock “Expensive” at the current price of $9.17

Orocobre Ltd

Positive drilling results: Orocobre Ltd (ASX: ORE) has 35% stake in Advantage Lithium that has announced for positive results at Cauchari. The Brine body has been discovered to have high Lithium concentrations in NW Sector, while initial samples from CAU07 returned an average of 635 mg/l Lithium and 4,772 mg/l Potassium at a depth of 236m. The initial samples from CAU16 between 169 and 199m averaged 619 mg/l Lithium and 4,878 mg/l Potassium. The group delivered a production of 2,135 tonnes of lithium carbonate in the September quarter with consecutive increases month on month as brine concentration and evaporation rates have been rising. ORE has maintained their guidance for the full year of 14,000 tonnes of lithium carbonate with production split approximately 45/55 between the first and second halves with record production expected in the December quarter at a production cost of <US$4,000/tonne. Given the lithium industry trends and ongoing momentum (including a 5% rise in stock price on November 09, 2017), we maintain a “Hold” recommendation on the stock at the current price of $6.09

Infigen Energy Ltd

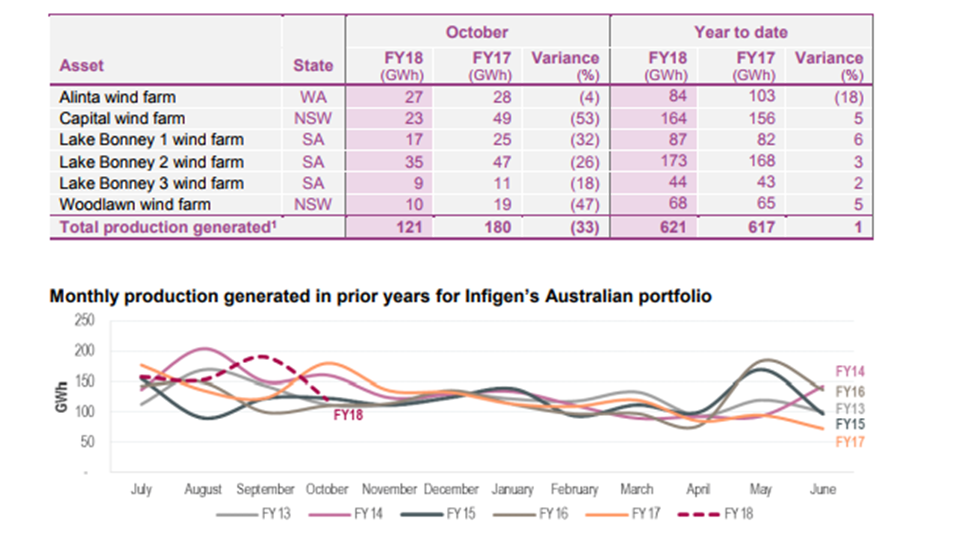

Rise in total year to date production: Infigen Energy Ltd (ASX: IFN) has recently reported that its total production generated for October 2017 in FY2018 is 121GWh and for FY17 production was 180GWh, while production on year to date basis for FY18 was 621GWh against FY17 figure of 617GWh. Lately, the group delivered a revenue rise of 14% yoy to $196.7 million driven by better electricity prices and higher LGC (Large-scale Generation Certificates) prices while underlying EBITDA rose 16% yoy to $139.3 million for FY17. The group’s net profit after tax surged 618% yoy to $32.3 million. The group expects their FY18 to be in line with FY17 but wind conditions might lead to uncertainty. The FY18 Marginal Loss Factors would be slightly more favorable than FY17. The group is set to have its AGM on 22 November 2017, which will provide insights on debt refinancing and other strategies. Any energy policy changes relating to Federal Government’s proposed National Energy Guarantee might fall in support of the stock. While IFN stock lost over 25% in the last six months (as of November 08, 2017); given the LNG prospects, we put a “Buy” recommendation at the current price of $0.71

October performance (Source: Company reports)

Goodman Group

Positive first quarter update: Goodman Group (ASX: GMG) delivered overall assets under management (AUM) of $33.9 billion concentrated in quality locations in major urban centers with $1.25 billion in asset sales during the first quarter of FY18. The occupancy across the portfolio enhanced to 98% driven by better quality properties and locations in core markets with + 0.9 million sqm of new leasing across the global platform reflecting $116 million of property income per annum and positive rental reversions of 3.2%. The Development work in progress (WIP) was maintained at $3.5 billion across 76 projects. The group also maintained their forecast FY18 full year operating earnings per security (EPS) of 45.71 cents, which is a rise of 6% against FY17. While the group is transitioning towards e-commerce for growth, GMG stock is trading at a higher P/E (compared to peers such as Scentre) and surged 2.6% on November 09, 2017. We believe that the stock is still “Expensive” at the current price of $8.72

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...