QBE Insurance Group Limited

.png)

QBE Details

Improving Outlook: QBE Insurance Group Limited (ASX: QBE) has recently announced the result of the tender offer for senior notes due 2022 for purchase by QBE for cash of up to US$ 100 Mn wherein the group has accepted Offers made at the Purchase Price on a pro-rata basis subject to a Scaling Factor of 18.035%. The purpose of the Tender Offer is to acquire up to all outstanding Notes. Besides this, the company has a strong market position that is engaged in underwriting general insurance and reinsurance risks and is undergoing a transformation which will generate positive results in terms of significant savings, supply chain management, and recovery initiatives. On the financial front, the group has recorded an adjusted combined operating ratio of 104.1 per cent for FY17 as compared with 93.7 per cent in 2016 which is above the target (95.0 per cent - 97.5 per cent); however, the group aims to take control of the operational efficiencies to bring down the ratio in FY18. Further, the company has set the target of investment return in the range of 2.5 per cent - 3.0 per cent based on undertakingvarious initiatives.

.png)

Investment Performance (Source: Company Reports)

During the year, the company has launched a program called “Brilliant Basics” which will improve the underwriting quality, pricing, and claims in the market in which it operates its every product that it underwrites. Meanwhile, the stock price has been declining in the last one year (down by 17.35 per cent) and is trading close to 52-week low level ($9.280). Further, the challenges of the year 2017 have now been left behind. Considering the improved financials, its business operations, and continuous efforts to achieve improvement in underwriting quality, pricing, and claims, we give a “Buy” recommendation at the current market price of $9.74.

.png)

QBE Daily Chart (Source: Thomson Reuters)

Scentre Group

.png)

SCG Details

Scope for growth in customer visitation and retailer demand:Since the establishment of the Group, the company has grown the value of its portfolio by more than 30% to $36.2 billion. With growing population and rise in need of having shopping centres with SCG having a majority of top shopping centres in Australia, the group seems to be well-positioned. The company has a solid financial position with total assets of $37.5 Bn, gearing of 32.1% and liquidity of $2.7 Bn as at 31 December 2017. During the year, the group completed lease deal across all categories including 31 major stores with the average tenure of 15 years, and 2,466 specialty lease deal covering an aggregated of more than 345,000 square metres of space. Comparable net operating income grew by 2.75% for the 12 months, driven primarily by contracted annual rent escalation. The group has a bright outlook at the back of positive market sentiment and current retail landscape. Based on that, theGroup confirmed its guidance for full-year growth in funds from operations (FFO) of approximately 4 per cent and confirmed a distribution guidance of 22.16 cents per security. Moreover, the company is maintaining its occupancy rate at 99.5% in the past three years.

.png)

Operating Performance as at 31 March 2018 (Source: Company Reports)

Recently, the group updated the market about the share cancellation after buy-back wherein it cancelled 1,53,93,44 shares, at an aggregate cost of $2,370,64.54. RoE and RoIC stood at 13.1% and 8.4%, respectively in 1HFY18 which is above the industry median. Meanwhile, the share has risen 14.62 per cent in the past three months and is trading at a low PE level among its peer group. Hence, we maintain our “Buy” recommendation on the stock at the current market price of $4.390, considering the aforesaid facts and robust fundamentals along with consistent returns.

.png)

SCG Daily Chart (Source: Thomson Reuters)

Westpac Banking Corporation

.png)

WBC Details

Decent Financial Performance: Over the past few years, Westpac Banking Corporation (ASX: WBC) has benefitted from the consumer and business banking units while cash earnings have been as expected. WBC recently announced the distribution of $1.0173 per security for SFI (Self-Funding Instalments) over securities in Vanguard Australian Shares Index as mentioned in PDS (Product Disclosure Statement) that dividends will be applied to reduce the Completion Payment of the SFIs and will be paid on or about 17 July 2018. The oldest bank of Australia highlights a decent first half year performance wherein statutory net profit rose by 7% and amounted to $4,198 Mn in 1HFY18 as compared to prior corresponding period. Resultantly, the reported net interest margin (NIM) expanded by 11 basis points to 2.16% in 1HFY18 which was driven by mortgage lending and deposit spreads throughout the same period. The Group also maintained the strength of its balance sheet with CET1 capital ratio of 10.5% which is in line with the benchmark set by Australian Prudential Regulation Authority (APRA). Liquidity Coverage Ratio (LCR) came at 134% which is well above the regulatory minimum.

.png)

Mortgage Portfolio (Source: Company Reports)

Based on aforesaid facts, the group’s credit portfolio is fundamentally sound, and it continues to be well positioned. With underlying demand in respect to the supply, the Australian housing market scenario may also start to work in favour of the bank in some time. We give a “Buy” recommendation on the stock at the current market price of $ 29.300.

.png)

WBC Daily Chart (Source: Thomson Reuters)

Technology One Limited

.png)

TNE Details

Positive outlook for Software as a Service (SaaS) business: Technology One Limited (ASX: TNE) has recently presented its business prospects at the UBS Emerging Companies Conference and highlighted about long-term outlook. According to the presentation, the company has the vision to take complete responsibility for building, marketing, selling, implementing, supporting and running its enterprise solution for each customer to guarantee long-term success. Currently, the company focuses on eight markets i.e., Government, Local Government, Financial Services, Health & Community Services, Asset Intensive Industries, Project Intensive Industries, Education, and Corporates to ensure long-term sustainability in the market. The company has now 280 large-scale enterprise customers, with many tens of thousands of users, making it the largest single instance ERP SaaS offering in Australia.

.png)

Net Profit Margin Before Tax (Source: Company Reports)

The company has a plan to substantially improve PBT margins by 25% in the next few years, and then continue to 30% thereafter, through controlled R&D growth and product maturity. Moreover, Jane Elizabeth Andrews who had an Indirect interest in the company acquired 2,300 ordinary shares through the on-market sale with the total consideration of $9,955.95. Meanwhile, the share price has fallen 17.92 per cent in the past three months and trading near to 52-week low level. Given the positive outlook of Software as a Service (SaaS) business, guidance for the full year to record profit growth of 10% to 15%, and availability at a low price, we give a “Buy” recommendation on the stock at the current market price of $4.250.

.png)

TNE Daily Chart (Source: Thomson Reuters)

Cooper Energy Ltd

.png)

COE Details

Moving up despite a delay to flow back operation of the Sole-3 gas by 1 week: While Cooper Energy Ltd. (ASX: COE) has suffered a delay with regards to its Sole Project, the oil and commodity prices are pulling the stock up. There has been a delay with regards to clean-up and flow back of the Sole-3 gas well pending re-installation of the upper completion as the section got anomalies after testing, which prevented verification of the pressure integrity of the annulus above the production packer. Therefore, the company had to take decision to re-run the upper completion with a new packer. It is anticipated that the operation to pull and re-run the upper completion will take approximately one week, to resume the preparations for the flow back. However, the operation to re-run the upper completion has no significance for the reservoir completion, that has been tested and its integrity being confirmed. Meanwhile, COE stock has risen 24.59% in three months as on June 28, 2018. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $ 0.385, which moved up 1.316% on June 29, 2018.

.png)

COE Daily Chart (Source: Thomson Reuters)

OceanaGold Corporation

.png)

OGC Details

Updated 2018 Guidance: OceanaGold Corporation’s (ASX: OGC) stock rose 1.613% on June 29, 2018 after the presentation at Macquarie Mining Forum, as the group touched upon its updated 2018 guidance and the company’s 2018 priorities. The company has revised upwards its 2018 consolidated gold production forecasts due to the strong operating performance and improvements to the mine plan at the Didipio Operation. Didipio is expected to outperform and is having opportunities for further optimisation while the company is progressing with the ramp-up of the underground. Therefore, the company now expects the 2018 gold production to be in the range of 500,000 to 540,000 ounces. Moreover, the operating performance at Haile is encouraging with recent solid plant performance while the mining activities are gradually improving. Further, in New Zealand, Waihi is back on track after a slow start while Macraes is exceeding expectations with improved plant performance and a steady feed of higher grade ore from Coronation North. Additionally, OGC’s 2018 priorities are to achieve the updated 2018 guidance, generate strong cashflows and deliver on organic growth initiatives.

Updated 2018 Guidance (Source: Company Reports)

Meanwhile, OGC stock has risen 4.49% in three months as on June 28, 2018 and is trading at a low P/E of 10.36x. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $ 3.780.

.png)

OGC Daily Chart (Source: Thomson Reuters)

Cann Group Ltd

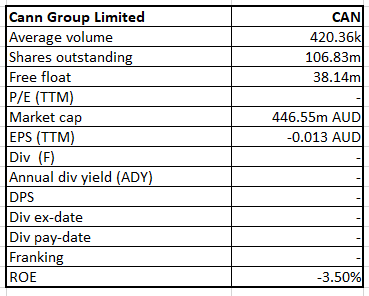

CAN Details

Signed a heads of agreement with Australia Pacific Airports: Cann Group Ltd.’s (ASX: CAN) stock surged 9.375% on June 29, 2018 while the group lately signed a heads of agreement with Australia Pacific Airports (Melbourne) Pty Ltd (APAM), and secured the site of CAN’s proposed Stage 3 medicinal cannabis cultivation and GMP manufacturing facility. The relationship can be of support from export purposes. CAN’s total investment for the project is estimated at circa $100 million. Australia Pacific Airports (Melbourne) will fund and conduct primary build of the facility. Moreover, the lease agreement for site will allow for substantially larger facility than previously scoped through expansion options. CAN with this agreement will be in a strong position for its Stage 3 expansion and the commissioning of the facility is expected 12 months from design completion. Meanwhile, CAN stock that has risen 20.75% in last six months fell by 8.57% in last one month. The latest developments in cannabis sector can help the stock like the Federal Government’s decision on exports of medicinal cannabis uplifted it in the past few months. As of now, we give a “Speculative Buy” recommendation on the stock at the current price of $ 3.500.

CAN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...