QBE Insurance Group

.png)

QBE Details

Update on Buy-Back Event: QBE Insurance Group Limited (ASX: QBE) updated the market about the progress on several transactions under its ongoing buy-back event. The group indicated to buy back shares with an aggregate consideration of up to A$190 million. As of now, the group has bought back a total of 1,43,13,799 shares via on-market trade for the total consideration of A$ 2,29,40,995.28. Besides this, QBE delivered decent performance in the first half of the year wherein statutory net profit after tax grew by 4% to $358 Mn in 1HFY18 as compared to the prior corresponding period. Moreover, the group recorded a Combined operating ratio (COR) of 95.1% and 95.8% (excluding discount rate) which is in line with the target range of 95% to 97.5% for the full year. Based on the performance, the Board of Director has declared an interim dividend of 22 cents per share, franked at 30% which is in line with the 2017 interim dividend payment. Moreover, the company has taken several steps to simplify its historically complicated business. For that matter, the group has disposed its operation in Thailand, Latin American, Argentina, and Brazil. Additionally, the group also sold its Australian and New Zealand travel insurance business to nib during the period.Further, the group has a comprehensive beneficial strategy for its Asia Pacific business that includes disposing of unprofitable business division and reducing costs. We expect that once the simplification program is done, the business will be in a more reasonable position over the long term.

.png)

1H18 results update (Source: Company Reports)

Meanwhile, the stock has risen 16.72 percent in the past three months and up by 3.06 percent in the past one week as at August 30, 2018. Based on the aforesaid fact, we maintain our “Buy” recommendation on the stock at the current price of $ 11.010.

.png)

QBE Daily Chart (Source: Thomson Reuters)

The Citadel Group

.png)

CGL Details

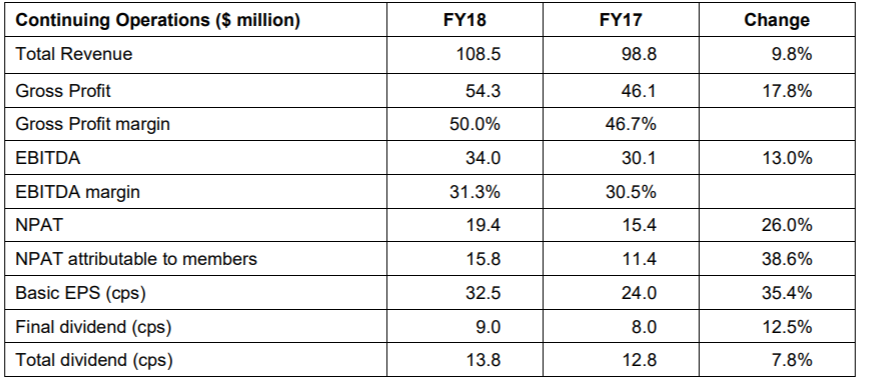

Brighter Outlook:The Citadel Group Limited (ASX: CGL) has brighter outlook ahead as the group recorded the number of contracts wins in FY18 along with improving SaaS client and user base in the key market. However, there are many opportunities to continue its growth of its core business in both public and private markets, particularly with its unique technology and health offerings. On the margin front, Gross margin, EBITDA margin and NPAT margin expanded by 330 bps, 350 bps, and 229 bps to 50.0%, 34.0%, and 17.9%, respectively in FY18 against the previous year. It reflects strong growth across overall businesses along with lower finance cost during the year.

FY18 Financial Highlights (Source: Company Reports)

Recently, the company announced that they will release 180,755 fully paid ordinary shares to the shareholders of the Citadel Group Limited from voluntary escrow on September 15, 2018 as per the appropriate Listing Rule. Moreover, PJA Australia Pty Ltd., a substantial holder of the Group changed its holding from 8.28% of interest to 7.24% of the voting power. Meanwhile, the stock has risen 15.37 percent in the past three months as at August 30, 2018 and is trading at a reasonable PE level of 20.58x. By looking at its stellar performance in FY18 and growing share of its core business in the key market, we put “Speculative Buy” recommendation on the stock at the current market price of $7.580 as it traded at the higher level.

.png)

CGL Daily Chart (Source: Thomson Reuters)

Tabcorp Holdings

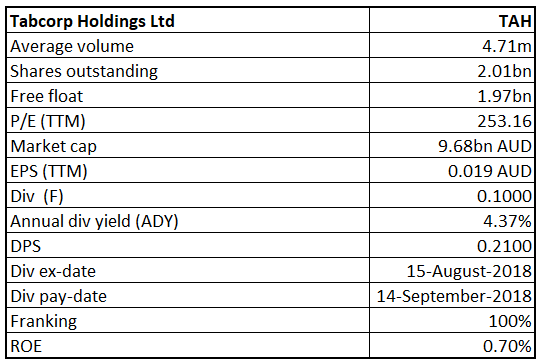

TAH Details

Growth momentum to be continued:Tabcorp Holdings Limited (ASX: TAH) has a positive business prospect as the group focuses on renewed licenses, new product launches, and strategical investment in the product mix i.e., retail, digital channels, and product initiatives. Besides this, the company will continue to embed the highest standards of regulatory compliance across the Group and maintain a disciplined approach to operating expenditure, capital investment, and balance sheet management. The company is on track to deliver $50 Mn of EBITDA synergies and business improvements in FY19; and has already delivered EBITDA synergies of $8 Mn in FY18 and has set a target to achieve at least $130 Mn in FY21. Meanwhile, the share price climbed up 8.82 percent in the past three months as at August 30, 2018. Hence, we maintain our “Buy” recommendation on the stock at the current market price of $4.80 by looking at positive industry trend and decent fundamentals while there is upside momentum in the stock.

.png)

TAH Daily Chart (Source: Thomson Reuters)

Cann Group

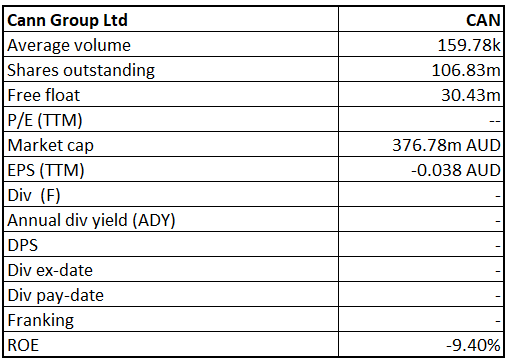

CAN Details

Well Positioned in Cannabis Market: Cann Group Limited (ASX: CAN) is a small-cap company with the market capitalization of circa $376.78 Mn as of August 31, 2018. The company is well positioned to capitalize on the growing medicinal cannabis market. Besides this, the group is aggressive to expand its program to secure future opportunities on the back of investing in clinical trials and other development activities. On the financial front, gross margin stood at 215.5% in FY18 which is higher than the industry median of 67.1%. The group had cash and cash equivalent of $ 49,566,890 as at 30 June 2018. The current ratio substantially increased from 28.66x to 89.32x in FY18 from the prior year. We expect that the company will see a positive growth momentum in 2019 as the group continues to strengthen the capabilities of its core team and secured partnerships. While the share price has fallen 16.15 % in the past three months (as at August 30, 2018) and traded at an average price of the 52-week high and low levels; we maintain our “Speculative Buy” recommendation on the stock at the current price of $2.780.

.png)

CAN Daily Chart (Source: Thomson Reuters)

Orocobre

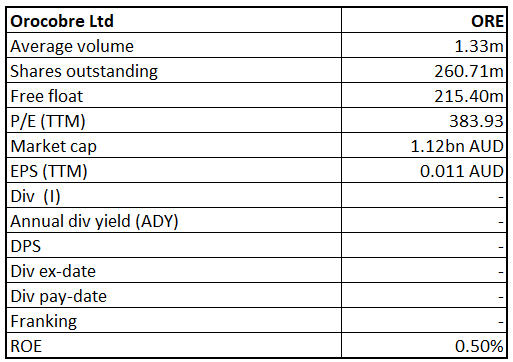

ORE Details

Fundamentals to fuel growth: Orocobre Limited (ASX: ORE) witnessed FY18 profit from continuing operations at US$1.9 Mn, a drop from the FY17 profit of US$4.6 Mn while total production was 12,470t of lithium carbonate, up 5% on FY17. Total sales revenue amounted to US$148.9m, up 24% from US$120.1m in FY17. Impairment write down of Borax assets to the tune of US$8 million negatively impacted the profit in FY18. However, Orocobre is in a unique position in terms of producing high-grade lithium chemicals for the surging battery demand across the globe and technical markets. Its Olaroz Lithium facility witnessed 20,000 tonnes of lithium carbonate production since the operation started in 2015. For its Borax S.A. division, the company adopted the strategy of shifting to the product mix to fuel the average pricing. During the 1HFY18, production rate for both Boric acid plant and Tincalayu increased. Meanwhile, the stock has generated a negative YTD return of 38.32% with price declining for multiple sessions now. However, the stock has respected its crucial support level around $3.8 and rebounded from there. At current levels, ORE could be a value play for the investors, given the risk-reward ratio. We recommend a ‘BUY’ on the stock at the current market price of $4.25.

.png)

ORE Daily Chart (Source: Thomson Reuters)

Boral

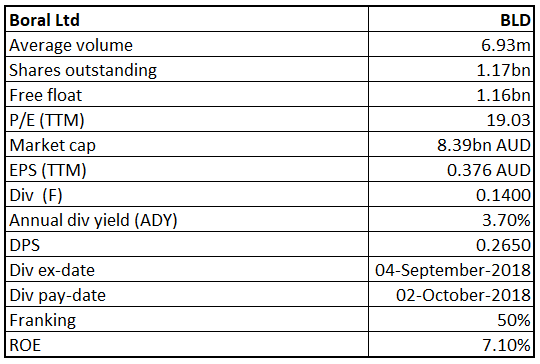

BLD Details

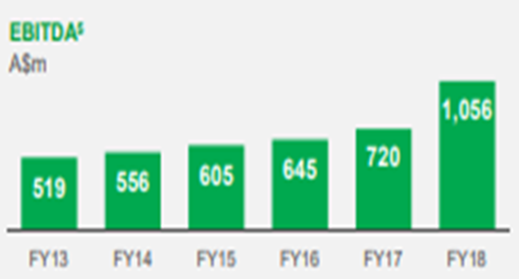

Sound Financials:Boral Limited (ASX: BLD) has posted a strong number for FY18 with revenue coming in at AUD$5,869 Mn, up 34% compared to AUD$4,388 Mn in FY17. The growth of 47% was witnessed in the NPATA at AUD$514 Mn in FY18, compared to AUD$350 Mn in FY17. Boral North America and Boral Australia contributed significantly to the earnings in the FY18. Operating cash flow remained strong and grew 40% to $578 Mn in the FY18 compared to $413 Mn in FY17.

EBITDA Growth (Source: Company Reports)

For FY19, the company is expecting growth to continue in Boral Australia, Boral North America and better outcomes in USG Boral. The company estimates high single-digit EBITDA growth or more in Boral Australia and 10% growth or more in Profit in USG Boral during FY19. Boral North America is estimated to post EBITDA growth of around 20% or more. Based on foregoing, we recommend a “Buy”’ on the stock at the current market price of $7.00 expecting the price movement to continue northwards, while there has been a slight dip of over 2.2% that was noted on August 31, 2018.

.png)

BLD Daily Chart (Source: Thomson Reuters)

OceanaGold Corporation

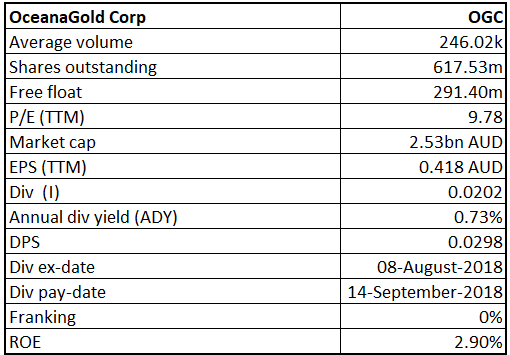

OGC Details

Rise in Organic Growth Opportunities: Oceanagold Corporation (ASX: OGC) posted an increase of 45% in the Net Profit after tax at $89.1 million for the first half 2018. Revenue from the ordinary activities for the company came in at US$402 Mn, up 21% compared to the FY17 corresponding period.Good results were largely driven by growth in exploration program and organic growth opportunities. The company is in a good position to continue posting good numbers, given their Martha Project at Waihi and the Haile expansion performing well. Based on the performance, the company has announced a semi-annual dividend payment of $0.02 per common share. The record date has been set at 9th August 2018 and would receive the payment of the dividend on 14th September 2018. The stock has generated a YTD return of 21.01% and is looking good at current levels. After a minor correction, pertaining to profit booking at higher levels, the stock has taken support at over $3.8 and rebounded from that level. Overall structure and price momentum look positive with the stock trading above its near-term Exponential moving averages. We recommend a “Buy” rating on the stock at the current market price of $4.15.

.png)

OGC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...