Telstra Corporation Limited (ASX: TLS)

.png)

TLS Details

Efforts to drive value and growth: Given the long-term perspective on cost management and maintaining dividend levels in view of the recent updates outstripping the challenges of last year, the outlook for Telstra weighs on a slightly positive side. Recently, the group with News Corp announced the completion of the transaction to combine Foxtel and FOX SPORTS Australia. The commercial arrangements were unchanged from those announced on March 6, 2018. Telstra’s investment in the new company will be equity accounted on an ongoing basis. Telstra expects to record a one-off accounting gain because of the fair value of the combined business compared with the book value. The current estimate of this gain was A$263 million and was subject to changes arising from the timing of completion and finalisation of adjustments on completion. There were no changes to Telstra’s previously stated guidance for the financial year 2018 as a result of the completion of this transaction. It released its half-year results for the financial year 2018 and reported an increase in the subscriber numbers on mobile and fixed, a reduction in underlying core fixed costs and progress being made under its strategic investment program.

.png)

Income growth by product (Source: Company Reports)

On a reported basis, including the Ooyala impairment, total income was up 5.9 per cent, Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) was down 2.5 per cent, net profit after tax (NPAT) was down 5.8 per cent and basic earnings per share (EPS) was down 3.4 per cent. The Group is operating within a significant period of change, including migration to the nbn, competitive challenges, accelerating pace of technological change and preparation for the transition to 5G. Within that environment, it tried to deliver a decent result in line with guidance for this half. It reaffirmed its FY18 total dividend guidance to be 22 cents per share fully franked including ordinary and special dividend, in accordance with its dividend policy announced in August 2017. The stock price has declined by 12% in three months, but the stock is recovering slightly as seen in last few days. We give a “Buy” recommendation for the stock at the current market price of $ 3.180.

.png)

TLS Daily Chart (Source: Thomson Reuters)

Spark Infrastructure Group (ASX: SKI)

.png)

SKI Details

Supporting Investment and Growth: SKI is a Utility and infrastructure related stock, which invests in regulated electricity distribution businesses in Australia and globally.Spark Infrastructure announced that Victoria Power Networks (Finance) Pty Ltd (“VPNF”), the Common Funding Vehicle for Victoria Power Networks (CitiPower and Powercor), in which it holds a 49% interest, has reached agreement with investors to place 10-year Norwegian Kroner and 12-year Euro Private Placements, both being inaugural issuances in respective markets. VPNF has raised Nkr550 million of 10-year fixed rate notes. Cross currency swaps were executed at the time of the note placement resulting in total proceeds of approximately A$91 million. The total proceeds raised equate to approximately A$129 million and the funds will be used for the capital works program and further refinancing requirements during the second half of 2018.

.png)

Distribution Network Utilisation Chart (Source: Company Reports)

Spark Infrastructure applies discipline in pursuing acquisition opportunities that are aligned with its strategic vision and are financially compatible with its existing risk profile. Spark Infrastructure’s leading networks are well placed to benefit as the Group entered Australia’s new energy era. Greg Martin, director of the company, having an indirect in the Company (through Jamoca Pty Ltd ATF The Martin Family Trust) acquired 50,000 shares on 24 April 2018 and now he holds 100,000 shares in the Company. The Group reaffirmed the distribution guidance for 2018 of 16.0 cps for 2018, an increase of 4.9% above 2017. During 2017, Spark Infrastructure considered new strategic options to increase the value of the group and improve distributions. Since the start of the year, the share prices were down by 6.8 per cent but rose up by 1.3 per cent in the past one week. We give a “Buy” recommendation at the current market price of $ 2.350.

.png)

SKI Daily Chart (Source: Thomson Reuters)

Transurban Group (ASX: TCL)

.png)

TCL Details

Continued opportunities for growth through development projects: TCL’s main aim is to become a partner of choice, with governments providing effective and innovative urban road infrastructure and services, while utilising core capabilities. It achieved asignificant growth in last 10 years and is consistently growing distributions. The Group lately indicated for $11.4 billion of new developments and asset enhancements and $7.7 billion of acquisitions. It has a proven-ability to continue sourcing new value-accretive opportunities. Transurban will work with partners to advocate on long-term transport policy by supporting multi-modal transport solutions, trialling new technologies to drive asset performance, exploring intersection of technology and transport to provide opportunities for disadvantaged groups. The Group launched Australia’s first real-world trial of user-pays road charging. Majority of existing toll roads were delivered by governments from both major parties, acting on long-term master plans.

.png)

Value creation (Source: Company Reports)

The Group’sConsortium partnerships support the capital requirements and the Capital releases provide a method to ensure that efficient capital structure is maintained. Its Balance Sheet is positioned for rising interest rate environment and minimal refinancing is required until FY20. It took the advantage of few opportunities for partnerships to strategically leverage Transurban core capabilities in non-traditional service arrangements like provision of tolling services to Toowoomba Second Range Crossing. It has been awarded the “Employer of Choice for Gender Equality” citation for four years in a row. The stock was declining since the start of the year that is by 5.8 per cent but the stock price increased by 3.73 per cent in last one month. We maintain a “Buy” recommendation at the current market price of $ 11.600.

.png)

TCL Daily Chart (Source: Thomson Reuters)

Nanosonics Limited (ASX: NAN)

.png)

NAN Details

Product Innovation and Customer Experience: Nanosonics, a leader in infection control solutions, announced receipt of the pivotal FDA 510(k) clearance for its 2nd generation trophon platform device, trophon2. This is excellent news delivering earlier than anticipated FDA clearance for its next-generation trophon device. Further, it delivered the first regulatory approval of its targeted new infection prevention solutions. Building on the success of the original trophon® EPR, Nanosonics’ next generation ultrasound probe High Level Disinfection system, trophon2, reflects a completely new mechanical and software design that delivers a range of new benefits based on input and feedback from its global community of customers. This included input from infection prevention specialists on future trends and requirements in the area of semi-critical device reprocessing. It is anticipated that the commercial release of the new trophon2 in the USA will take place during the first quarter of the 2019 financial year. The product is currently being introduced into manufacturing with a ramp up in production expected to take place over the next 3 months. The original trophon EPR device will remain in the market as an entry level product and it expects a significant proportion of sales to shift from trophon EPR to the new trophon2 system.

.png)

Trophon Installed Base Trend (Source: Company Reports)

This regulatory clearance from the FDA for trophon2 further underpins the Group’s geographical expansion plans and will form the basis for feasibility assessments and potential regulatory submissions for new markets. With the introduction of trophon2, Nanosonics aims to further build on its leadership position delivering to the market the most complete automated point of care solution with full traceability for ultrasound probe reprocessing. The Group announced that the German Society of Ultrasound in Medicine (DEGUM) has published comprehensive recommendations for infection prevention in ultrasound and endoscopic ultrasound and adds to the growing number of European guidelines, all supporting the requirement for High Level Disinfection of all semi critical ultrasound probes. The stock was falling in the last one year that is by 22.47 per cent and after the receipt of the FDA clearance the stock rose up by 4.26 per cent in the past one week. The stock was again down by 1.6 per cent on 30 April 2018 at the back of short selling activity. However, given the potential, we put a “Speculative Buy” recommendation on the stock at the current price of $ 2.410.

.png)

NAN Daily Chart (Source: Thomson Reuters)

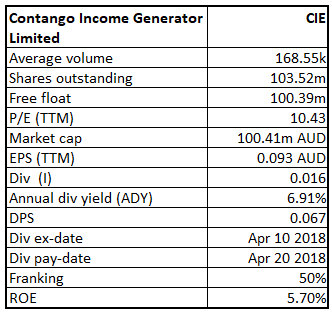

Contango Income Generator Limited (ASX: CIE)

CIE Details

Cash positioning: CIE’s underlying portfolio posted a return of -3.1% for the month of March compared to the market return of -3.6%, an outperformance of 0.5%. While the 12 months return at 2.4% is down on the Index (3.7%), it is a stronger result when compared to the ASX300 Industrials Accumulation Index (the Index more closely aligned with stocks in the portfolio), which has been flat for the last 12 months. Performance since inception remains solid at 8.2%. The Group issued 138,913 fully paid ordinary shares at an issue price of $0.093 per share. One of its Director Donald Ian Clarke, having an indirect interest in the Company acquired 1,736 shares through the Company’s Dividend Reinvestment Plan at $0.93.

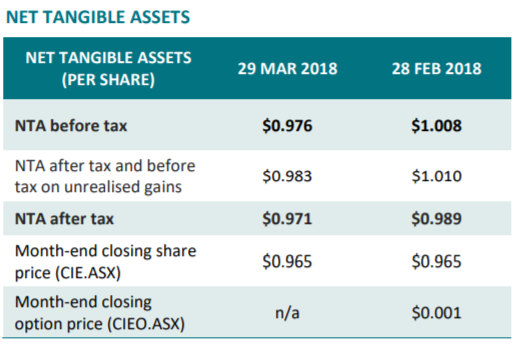

Net Tangible Assets Performance (Source: Company Reports)

Throughout this period, the management of the portfolio maintains a deliberate and focussed strategy. From a macro perspective, the fund will perform best in a low growth and benign inflation environment when bond markets are rallying or stable. It continues to target gross yields 100bp above the market with a portfolio of stocks that achieve this with strong business fundamentals through cash flow and strong balance sheets. The cash weighting in the fund was around 13% which helps it to keep the portfolio’s risk profile below that of the market. The stock price was marginally up by 0.5 per cent in the past three months but increased by 2 per cent in the past one week. We give a “Speculative Buy” recommendation on the stock at the current price of $ 0.965.

.png)

CIE Daily Chart (Source: Thomson Reuters)

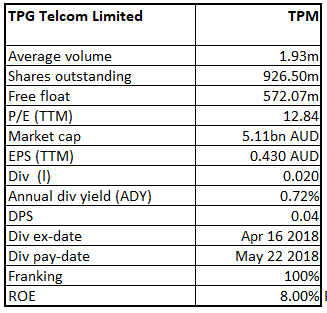

TPG Telcom Limited (ASX: TPM)

TPM Details

Upgraded the guidance for the underlying EBITDA: The Company advised that the issue price for shares to be given to the shareholders who were elected to participate in Dividend Reinvestment Plan in respect of the interim FY18 dividend (2.0 cents per share (fully franked)) will be $5.1529 per share and this will be paid on 22 May 2018. This issue price is inclusive of the 1.5 per cent discount that was announced for the dividend and has been calculated in accordance with the Company’s rules. TPG Telecom Limited in its results for the half year ended 31 January 2018 reported Earnings before interest, tax, depreciation and amortisation (“EBITDA”) for the period of $418.2 million and delivered $198.7 million of Net Profit After Tax attributable to shareholders (“NPAT”) for the period.

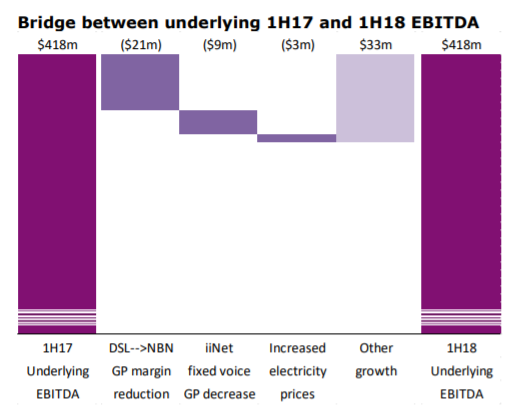

EBITDA Performance (Source: Company Reports)

Although there was $55.2 million of a decrease in reported EBITDA between 1H17 and 1H18, the underlying EBITDA, in fact, increased slightly in 1H18 from $417.6 million to $418.2 million. This small EBITDA increase was achieved despite the significant headwinds that were experienced in 1H18 from the migration of DSL customers to lower margin NBN services, loss of gross profit from home phone services as customers migrated to NBN bundled services and electricity price increased. At the end of 1H18, the Group had bank debt (net of cash) of $1,394.3 million, which represents a leverage ratio of ~1.7x EBITDA and had undrawn headroom of over $900 million in its debt facilities to fund its remaining mobile network investment. In light of the first half performance, the directors have upgraded the guidance for underlying EBITDA for the Group for the full year FY18 to now be in the range of $825-830 million. In the past six months, the stock price was up by 6 per cent and increased by 5 per cent in the last one week. Therefore, by looking at the overall performance and future potential, we give a “Buy” recommendation at the current market price of $ 5.580.

.png)

TPM Daily Chart (Source: Thomson Reuters)

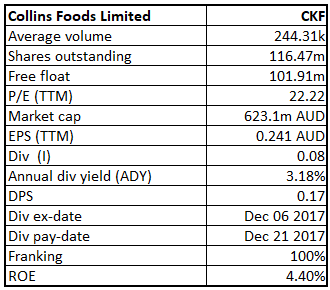

Collins Foods Limited (ASX: CKF)

CKF Details

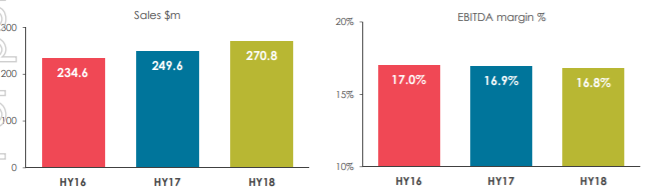

Creating growth opportunities: During the first half of 2018, the group has completed acquiring five out of 28 KFC restaurants from Yum! while the rest of 23 would be finished in the second half. Based on ongoing development related to expanding footprints in Asia region and increased store counts over the period, CKF is expected to witness growth in years to come. It has two other areas of the business where it could create good growth over the coming years.

Sales and EBITDA Margin Performance (Source: Company Reports)

The first exciting part is that it has started acquiring KFC restaurants in Germanyand in the Netherlands and has created a huge new region of potential targets which it could acquire. The Group has opened its first outlet of Taco Bell in Australia and is progressing well. Newman Manion, director of the Company, having an indirect interest in the Company recently disposed of 21,819 shares. The share price was up by 2 per cent in the past one week after a dip of 7.6 per cent in the last six months. We give a “Buy” recommendation at the current market price of $ 5.350.

.png)

CKF Daily Chart (Source: Thomson Reuters)

Note: ROE values are as per latest performance and have been extracted from Thomson Reuters

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...