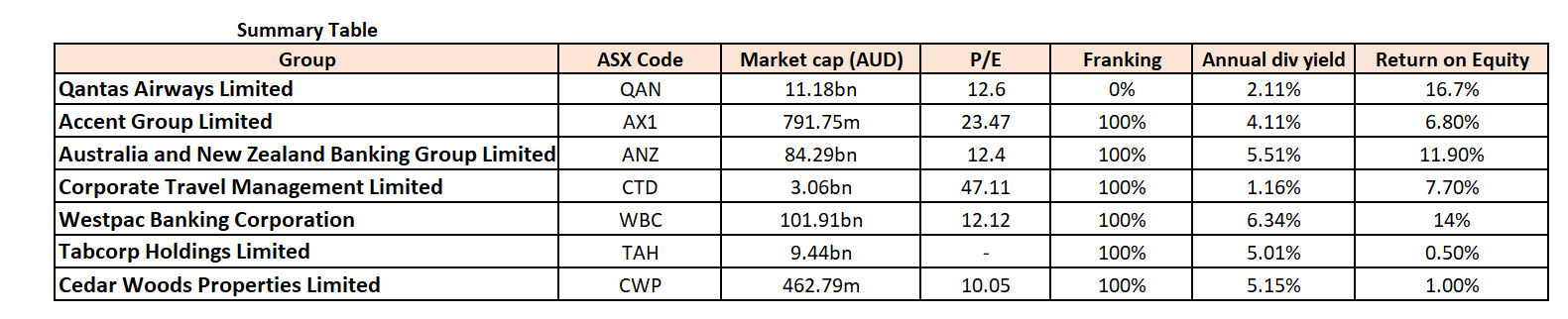

Stocks’ Details

Qantas Airways Limited (ASX:QAN)

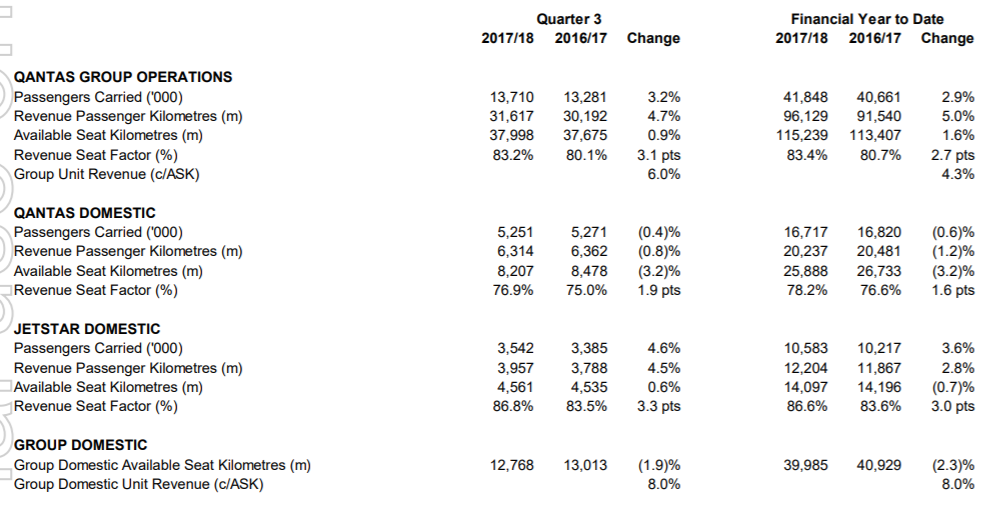

Benefit of ongoing network adjustments - Recently, Qantas came out with its market update with regards to performance during the third quarter of FY18 and reported an increase of 7.5 per cent in total revenue ($4.25 billion) over prior corresponding period, owing to improved domestic and international markets’ performance. Combined, Qantas and Jetstar have around 90% of the domestic profit pool and have a widening margin advantage over their competitors. The Growth of the airline depends upon the global growth and traffic. Recently, there was a speculation in the market that institutional investors were slashing their expectations for corporate earnings over the next year which will impact the overseas growth and so can impact this national carrier. However, the group still stands strong on the fundamentals and efforts that can be undertaken to mitigate risks. Qantas three-years’ $2 billion turnaround program, which started in 2014 to make Qantas Group sustainably profitable got over now and has delivered good outcome. ROE improved from 9.3 per cent in June 2017 to 16.7 per cent in December 2017 which was more than the industry median (5.5 per cent). The stock price was up by 1.65 per cent as on 19 July 2018 (risen up by 12.16 per cent in last three months as on 18 July 2018). The Group will release its financials around 23 August 2018. We give a “Buy” recommendation at the current market price of $6.75 as the Group focuses on its continuous improvement which will drive cost and revenue benefits from new technology and will help in creating more efficient operations.

Quarterly Market Update (Source: Company Reports)

Accent Group Limited (ASX:AX1)

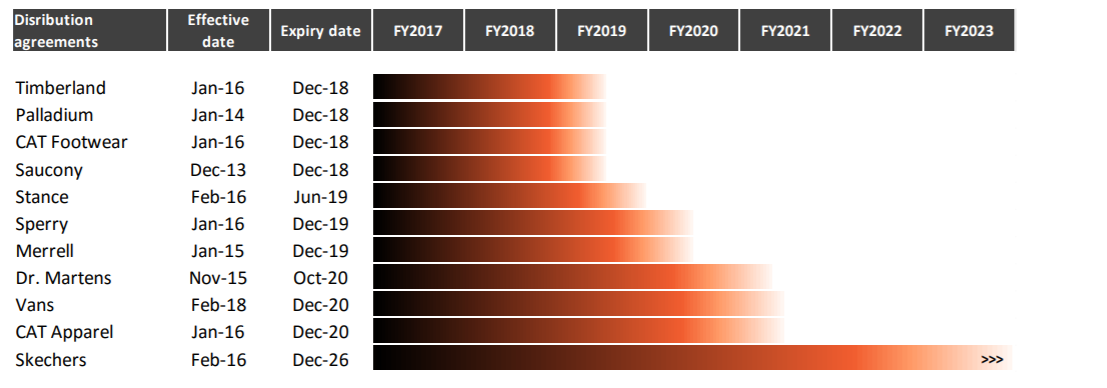

Rising competition - Accent Group Limited, formerly RCG Corporation Limited, is an investment holding company. The Group owns, operates and manages a range of footwear and apparel businesses in the performance and active lifestyle sectors. The group’s performance relies on same-store sales trend and market share. However, Amazon’s entry in the Australian market is already a threat to the Group and has raised a red flag and is creating an overseas competition. The group declared a fully franked interim dividend of 3.0 cents per share and expects its dividend pay-out ratio to be between 75% to 80% of underlying earnings per share for the full year. ROE improved from 2.1 per cent in June 2017 to 6.8 per cent in December 2017. The stock price was up by 2.39 per cent as on 19 July 2018 (down by 9.32 per cent in last one month as on 18 July 2018). We give a “Hold” recommendation at the current market price of $1.49 by looking at the Group, which is positioned well to defend against new market entrants and capitalise on growth opportunities.

Growth of Distribution Agreements (Source: Company Reports)

Australia and New Zealand Banking Group Limited (ASX:ANZ)

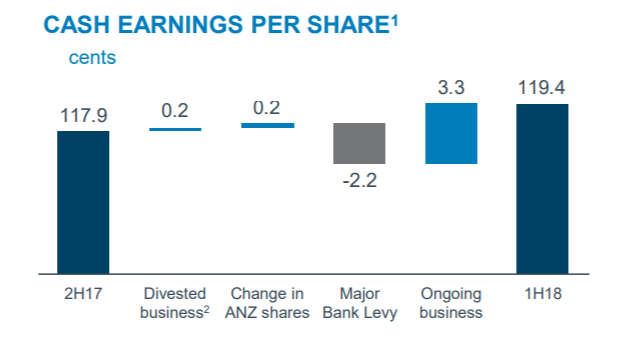

Branch Closure - Australia and New Zealand Banking Group Limited (ANZ) provides a range of banking and financial products and services to retail, small business, corporate and institutional clients. The Company recently appointed Adrian Went as Group Treasurer with effect from the start of July who will be based in Melbourne. Recently, the Banking Group entered into an agreement to sell its Retail, Commercial and Small-Medium Sized Enterprise (SME) banking businesses to Kina Bank with the objective to focus on Institutionaland Large Corporate banking services in the Papua New Guinea (PNG) and the Group will sell 15 ANZ retail branch premises, 72 ANZ ATMs and over 1,800 ANZ EFTPOS terminals across PNG and it is expected that the transaction will be completed by the third quarter of 2019. There were speculations in the market that Bank is planning to close its regional Corowa branch in October. The Group will release its full year financials on 31 October 2018. ROE increased by 32bps in 1HFY18 as compared to 1HFY17. NTA per share increased by 6 per cent in 1HFY18 as compared to 1HFY17. As of now the Group is trading at a decent annual dividend yield of 5.51 per cent. We give a “Hold” recommendation at the current market price of $29.21 as it is moving close to its 52-week high price that is $30.80. It’s better to “Hold” the stock looking at the interest-rate scenario and pressure in the banking sector.

Cash Earnings per share Performance (Source: Company Reports)

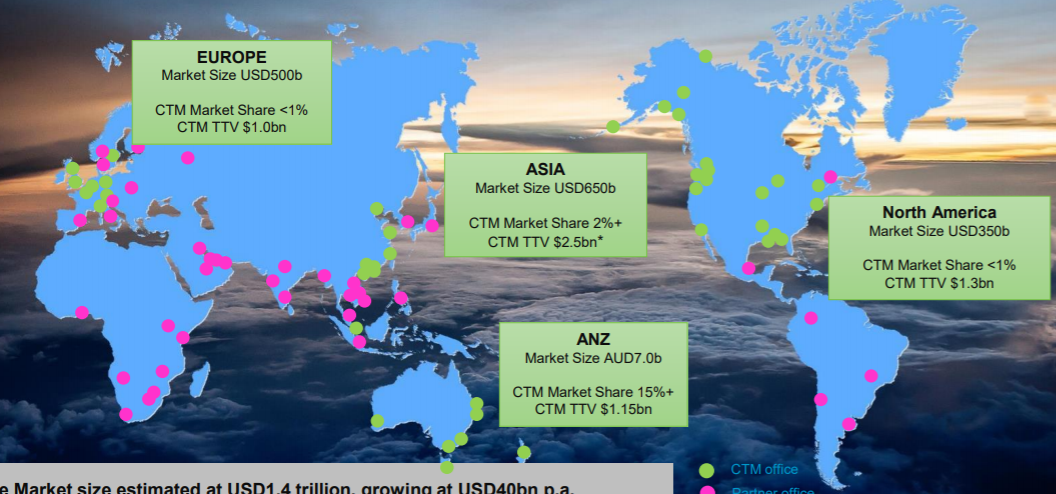

Corporate Travel Management Limited (ASX:CTD)

Strategic Acquisition in the pipeline - Corporate Travel Management Limited is an Australia-based travel management company, which along with its subsidiaries, is engaged in the purchase and delivery of corporate travel solutions. The Company recently announced a strategic acquisition and will be acquiring 75.1 per cent of the Lotus Travel Group Limitedshare and the Group’s CTM Asian partners Ever Prestige Investments Limited will be acquiring the remaining 24.9 per cent of the share. This will be effective from 2nd October 2018. ROE in December 2017 was 7.7 per cent which is more than the industry median that is 6.3 per cent. It is expected that the Group will deliver full year results at or slightly above the top end of the Guidance. The Group is expected to release its financials on 22 August 2018 along with its updated Profit Guidance. We recommend to “Hold” the stock at the current market price of $28.55 (very near to its 52-week high price that is $29.99) by looking at the growing market share through its organic route and one can wait and watch the impact of the acquisition in the market.

Diversified Business (Source: Company Reports)

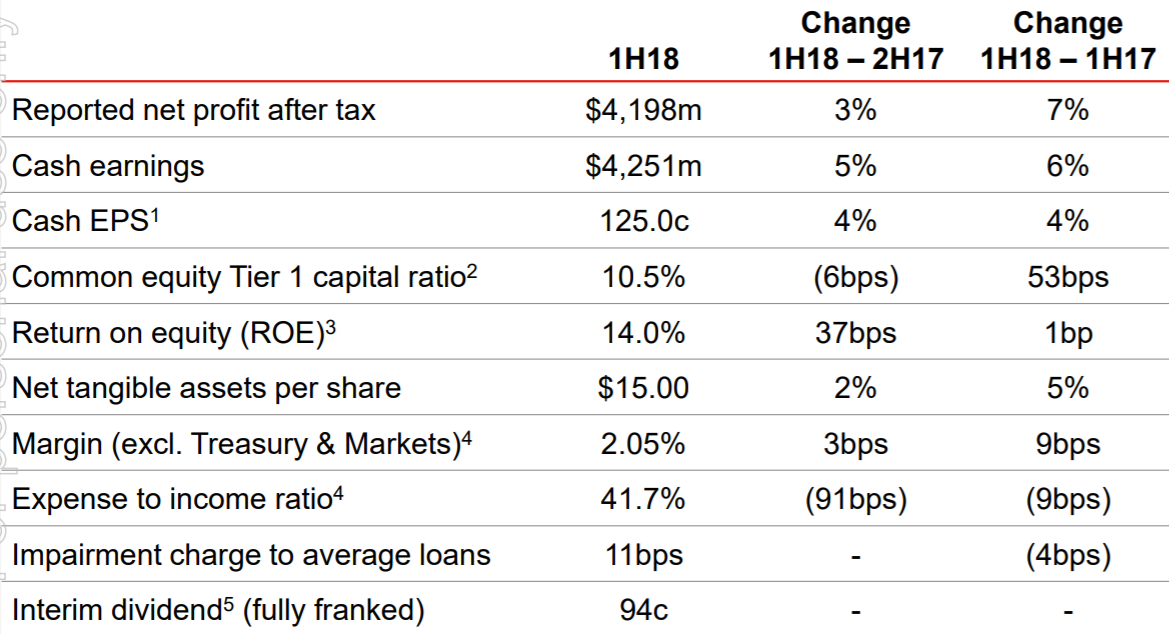

Westpac Banking Corporation (ASX:WBC)

Improvement in Returns - Westpac is Australia's first financial entity to start a service revolution and is the first bank and oldest amongst the big four major banking organisations in Australia. The Group reported a profit of $4,198 million (an increase of 7 per cent as compared to 1HFY17) for 1HFY18 (ended March 2018) and it delivered a CET-1 ratio of 10.5 per cent which is in line with APRA’s ‘unquestionably strong’ benchmark. Royal Commission’s pressure on the Banking Group made the Bank more conscious of its lending transactions which provided a critical opportunity to restore customer trust across the sector. ROE increased by 2 per cent for 1HFY18 as compared to 2HFY17. According to the experts the Banking Group’s first-half cash earnings were in line with expectations and the stock has a lot of potential to grow which leads to the positive sentiments in the market. We give a “Buy” recommendation at the current market price of $29.70 by looking at the system lending growth and at an annual dividend yield that is 6.34%.

Financial Performance (Source: Company Reports)

Tabcorp Holdings Limited(ASX:TAH)

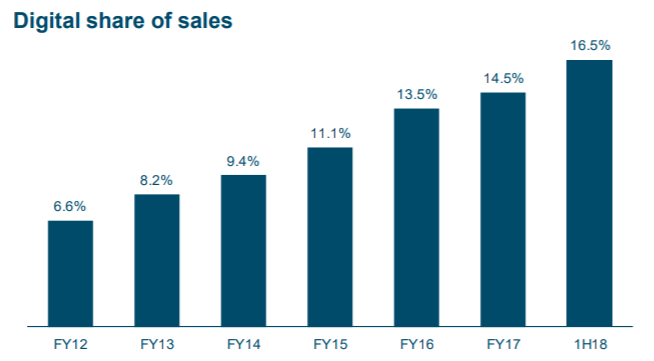

Improvement in Digital Turnover - Tabcorp Holdings Limited is engaged in the provision of gambling and entertainment services. The Company’s aim is to drive commercial success through championing social and sustainable ways to play and further it supports its shareholders, customers and the community. ROE improved from (5.1 per cent) in June 2017 to 0.5 per cent in December 2017. Lately, Tabcorp sold about 2.85 million Jumbo shares to institutional investors for $4.26 per share because of which there was a drop in Jumbo’s share price but did not impact the market sentiments. The Group is trading at an annual yield of 5.01 per cent. The group announced a fully franked interim dividend of 11.0 cents per share with a dividend target of 90 per cent of NPAT in FY18 and is targeting gross Debt/EBITDA ratio of 3.0-3.5x and intends to maintain an investment-grade credit rating. The stock has been rising since last three months and was up by 7.82 per cent and by 49.66 per cent in the last 5 years as on 18 July 2018. We give a “Buy” recommendation at the current market price of $4.66 (inching closer to the average of 52 week high and low prices).

Trend of Digital share of sales (Source: Company Reports)

Cedar Woods Properties Limited (ASX:CWP)

Strong Pre-sales for FY19 - Cedar Woods Properties Limited is a property development company. The Company’s principal interests are in urban land subdivision and built form development for residential, commercial and industrial purposes. The Group recently signed an agreement to sell a third office building in Williams Landing, Victoria and the Group has twenty additional sitesin the Williams Landing Town Centre that can accommodate commercial, residential or mixed-use developments. The Company expects FY18 net profit after tax to be around $40 million. The settlements that were not completed in FY18 will boost FY19 earnings and the group entered into FY19 with presales of more than $320 million which will de-risk earnings for FY19 and are expected to drive a strong uplift in net profit. We would recommend to “Hold” the stock at the current market price of $5.80 as the Company is positioned to perform well in FY19 and has a positive outlook.

NPAT/Total Dividend Performance (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...