.png)

Stocks’ Details

Australia and New Zealand Banking Group Limited

Update on Buy-Back Event: Australia and New Zealand Banking Group Limited (ASX: ANZ) updated the market about the progress on several transactions under its ongoing buy-back event. The group intends to buy back remaining shares with an aggregate consideration of A$1,395,212,666 out of A$3 Bn. As of now, the group has bought back a total of 6,49,87,709 shares via on-market trade for the total consideration of A$ 1,83,07,15,583.41. Besides this, the group has recently presented its Basel III disclosure in which Credit Risk Weighted Assets (CRWA) was down by 0.6% from March 2018 to $340.9 billion at June 2018. It was mainly supported by an improved portfolio mix in the Institutional business within the Corporate asset class offsetting portfolio growth. However, exposure at Default (EAD) was moderately up by $12.7 Bn to $943 billion in Q3 FY18 from the previous quarter. This underlying movement was primarily driven by the combination of foreign exchange movements and portfolio growth in AIRB Corporate ($4bn), Sovereign ($5.4bn), and Bank ($3.1bn) asset classes. While Credit Impairment Charge was down by $85 Mn to $121 Mn in Q3FY18 from the previous quarter. It was mainly driven by several one-off recoveries and high level of write-backs in the Institutional business, combined with individual credit upgrades and improved risk mix of the portfolio.

.png)

Movements in Credit Risk Weighted Assets ($Bn) (Source: Company Reports)

ANZ’s level 2 Common Equity Tier 1 (CET1) capital ratio of 11.07 percent as of 30 June 2018 marked a growth of 3 bps from March 2018.It was mainly driven by an organic capital generation of +50bps and receipt of reinsurance proceeds from the One Path Life (OPL) sale of +25bps while offset by the FY18 Interim Dividend of -59bps and the share buyback of -8bps. Meanwhile, the share price has risen 6.17 percent in the past three months at August 29, 2018 and is trading close to the 52-week high level of $30.800. Based on foregoing that the company will maintain Basel III norms going forward, we put “Hold” recommendation on the stock at the current market price of $29.39.

National Australia Bank Limited

Trading at Reasonable Level:National Australia Bank Limited (ASX: NAB) delivered decent Q3FY18 trading update wherein revenue increased by 1% in Q3 FY18 at the back of decent growth in SME lending within Business & Private Banking and a strong contribution from New Zealand Banking. However, the Cash earnings declined by 3% in Q3 FY18 as compared to the prior corresponding period due to the higher investment expenditure and credit impairment charges incurred during the same period. The Group Common Equity Tier 1 (CET1) ratio decreased by 50 bps to 9.7% in Q3 FY18 compared to the previous quarter. It was largely impacted by the interim 2018 dividend declaration of (63bps net of DRP) and seasonally stronger loan growth in the June quarter. However, the group is on track to achieve APRA’s ‘Unquestionably Strong’ CET1 ratio benchmark of 10.5% by January 2020 in an orderly manner, with accommodation of APRA’s proposed revisions to RWAs (risk-weighted assets).

.png)

Capital, Funding & Liquidity (Source: Company Reports)

On the other hand, the group hadannounced the resignation of Mr. Antony Cahill as a Chief Operating Officer (COO), effective from 14 September 2018. However, Ms. Rachel Slade has been appointed as an acting Group Executive Customer Products & Services, effective immediately, to enable a smooth transition – subject to any applicable regulatory approvals and registration requirements. Besides this, the group disclosed its interest payment of AUD 0.80710466 with the Interest rate of 3.202100 % per annum for NABHA - HYBRID 3-BBSW+1.25% PERP SUB EXCH NON-CUM STAP and it will be paid on November 15, 2018 with the record date of October 31, 2018. Meanwhile, the share price has risen 5.36 percent in the past three months and trading at a reasonable PE level of 14.630x. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $28.30, down 0.63 percent on August 30, 2018.

Commonwealth Bank of Australia

Decent trending:Commonwealth Bank of Australia (ASX: CBA) is a large-cap company with the market capitalization of $128.87 Bn as of August 30, 2018. The group has revealed encouraging results lately while the market was expecting them to be quite bleak. The group also disclosed the market about CBA Instalments for IAGIYE series and WESIYE series in which CBA Equity Products Group, is the Issuer of Instalment Warrants over ordinary shares in Insurance Australia Group Limited (IAG) and declared the record date as 22 August 2018 for entitlements to the $0.20, 100% franked dividend for the IAG Commonwealth Bank Instalments. In addition, CBA Equity Products Group, as the Issuer of Instalment Warrants over ordinary shares in Wesfarmers Limited (WES), also declared the record date as 21 August 2018 for entitlements to the $1.20, 100% franked dividend for the WES Commonwealth Bank Instalments. On the other hand, Commonwealth Bank of Australia and its related bodies became the substantial holder of Duluxgroup Limited by holding 5.02 percent voting rights. Meanwhile, the stock has risen 4.09 percent in the past three months as at August 29, 2018 and is trading at a reasonable PE level of 13.71x. By looking its decent fundamentals, wide distribution network, franchise value, and a high and growing share of retail loans in the key market, we put “Buy” recommendation on the stock at the current market price of $72.150.

Bank of Queensland Limited

Net Interest Margin Broadly in line with Industry Median:Bank of Queensland Limited (ASX: BOQ) has lately revealed that the net interest margin (NIM) stood at 1.97% in 1HFY18 which is broadly in line with the industry median (1.98%). Efficiency ratio increased by 140 bps to 52.10% in 1HFY18 against 2HFY17. While the group’s underlying expenses have grown, margin performance was not that bad as expected. The group has already faced many challenges owing to the regulatory scenario, and this seems to have been factored in the price. However, the bank has maintained its strong capital position as the CET1 ratio was up 3 basis points over the 1H 2017 to 9.42 percent in 1HFY18. Besides this, the group disclosed its distribution payment of AUD 1.00770000 with dividend distribution rate of 1.9000 % per annum for BOQPE - CAP NOTE 3-BBSW+3.75% PERP NON-CUM RED T-08-24 which was paid on August 16, 2018 with the record date of July 31, 2018. Meanwhile, the share price rose by 10.77 percent in the past three months as at August 29, 2018 and currently trading close to mid of 52-week high and low levels. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $ 11.550.

MyState Limited

Decent Performance in FY18: MyState Limited (ASX: MYS) for FY18 has reported 3.1% rise in Net interest income, 4.6% rise in Net profit after tax, 0.93 cps growth in Earnings per share to 34.97 cents per share. The group’s balance sheet remains strong. The group’s capital adequacy ratio at 30 June 2018 was 13.5%, up 18 basis points compared to the previous year. Further, the Board had set the Common Equity Tier 1 Capital target range to be between 8.0% and 9.5% and the Total Capital range to be between 11.5% and 14.5%. Of which, the group was able to record a Common Equity Tier 1 Capital Ratio and Total Capital Ratio of 11.1% and 13.47%, respectively as at 30 June 2018. It reflects that the group is well positioned for future growth. The company has declared to pay a final dividend of 14.5 cents per share (fully franked) for its shareholders and it will be payable on September 25, 2018 with the record date of August 24, 2018.

FY18 Financial Highlights (Source: Company Reports)

On the other hand, the group disclosed the market that one of its director Andrea Waters who had an Indirect interest in the company acquired 20,000 shares through the on-market purchase with the total consideration of $93,400. Meanwhile, the share price has fallen 2.64 percent in the past three months (as at August 29, 2018) and traded at a reasonable PE level of 13.70x. Based on decent performance in FY18, we maintain our “Hold” recommendation on the stock at the current market price of $ 4.670.

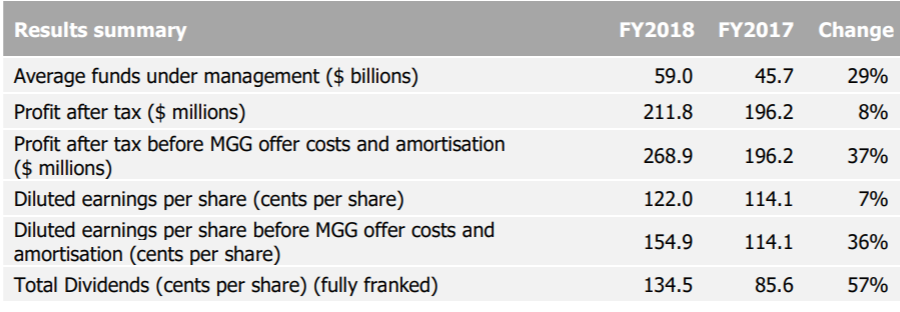

Magellan Financial Group Limited

Upwardly Revised Dividend Payout Policy: Magellan Financial Group Limited (ASX: MFG) delivered a successful financial year with average funds under management (FUM) growth of 29% to $59.0 billion in FY 18 against the prior year. Profit after tax (excluding the one-off Magellan Global Trust net offer costs and noncash amortization) stood at $268.9 million in FY 18, marking 37% growth on the Y-o-Y basis. During the year, the Board of Directors revised the dividend policy to increase the payout ratio in the range of 90% to 95% of the net profit after tax from the previous payout of between 75% and 80%. As of now, the group has a very strong balance sheet and sufficient capital to support the ongoing growth of the business and seed future new initiatives. Meanwhile, the share price has risen 19.84 percent in the past three months as at August 29, 2018 and trading at the higher level. Based on foregoing, we maintain our “Hold” recommendation on the stock at the current market price of $ 28.0.

FY18 Financial Highlights (Source: Company Reports)

Suncorp Group Limited

Capital Management:Suncorp Group Limited (ASX: SUN) has recently disclosed its distribution payment of AUD 1.21110000 with dividend distribution rate of 0.000 % per annum for SUNPD - CAP NOTE 3-BBSW+2.85% 22-11-23 CUM RED which will be paid on November 22, 2018 with the record date of November 14, 2018. Recently, the group announced to issue new Australian dollar floating rate, unsecured, subordinated notes (Wholesale Subordinated Notes) which will be offered to institutional and other wholesale market investors. Apparently, the group has successfully priced an A$600 million issue of floating rate, unsecured, subordinated notes in an offering to institutional and other wholesale market investors. The Wholesale Subordinated Notes are expected to be issued on or about 5 September 2018. No shareholder approval is needed for the issue. As of now, we put “Hold” recommendation on the stock at the current market price of $ 15.480 as it traded at the higher level and has potential to grow further.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...