Stocks’ Details

Telstra Corporation Ltd (ASX: TLS)

Long Term Growth Plan: Telstra recently highlighted about the Australian Competition and Consumer Commission’s decision to clear the combination of Foxtel and Fox Sports into a new company, but this is subject to the conclusion of definitive agreements and fulfilment of certain other conditions. Foxtel and Fox Sports have a close and long-standing relationships, operating within the ownership of News and Telstra and as a result of this merger, Telstra was appointed as the exclusive telecommunications agent for Foxtel’s digital products. They are also reframing their 2018 dividend which is expected to be 22 cents per share (fully franked). As per the revised guidance, TLS’ FY18 total income is expected to be $27.6b to $29.5b after $0.7b reduction, EBITDA to be $10.1b to $10.6b after $0.6b reduction, and free cash flow to be $4.2b to $4.7b after $0.2b reduction at the back of the delay in nbn co.’s hybrid fibre co-axial technology for six to nine months from December 2017 and nbn’s Corporate Plan 2018. On the other hand, TLS might benefit from the delay over the full roll-out. In the past one year, the stock price decreased by 27% but rose over 5.48% in the last one month (as at December 20, 2017). Keeping the dividend in view along with expectation of a better performance in long-term, we maintain a “Hold” on Telstra at the current price of $3.65

TLS Objectives (Source: Company Reports)

Wesfarmers Ltd (ASX: WES)

Slowdown in Coles Food and Liquor Business: Wesfarmers’ market share has been down tremendously in this year and the group has designed a new strategy to focus on its Australian Food division. During this year, the group particularly flagged about the weakness of the Coles division many a times. The lack of growth was seen to be compounded by almost 60 basis points of margin compression as margins decreased from 4.7% to 4.1% which made 2017 as the least profitable year for Coles since 2013. In 2017, the company declared a fully-franked final dividend of $1.20 per share taking full year dividend to $2.23 against $1.86 per share in 2016. On the other hand, underlying net profit after tax increased by 22.1% to $2,873 million and earnings per share also increased by 21.6% to a record to $2.55 per share. The major significant highlight was a jump of operating cash flow which increased from $861 million to $4,226 million.As per the first quarter of FY18, headline food and liquor sales were up 1.5% while total Coles Express sales, including fuel, for the quarter slipped by 9.5% over prior corresponding period. While the dividend yield might look exciting, losses are expected to increase in 2018 as trading remains a challenge. We maintain an “Expensive” recommendation on the stock at the current price of $44.65

WAM Capital Ltd (ASX: WAM)

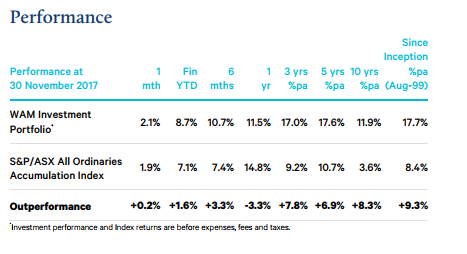

Great dividend paying LIC: WAM’s main objective is to deliver shareholders a rising stream of fully franked dividends. It is one of the largest listed investment companies on ASX and it has a decent dividend yield. The dividend has grown every year but there is only a few years of profit reserves as per recent WAM investor update, and if WAM keeps performing in line, then it will continue growing dividends and NTA for shareholders. The full-year shareholder return for WAM was 14.1% and return on equity portion of the portfolio was 17.2%, and it reported operating profit before tax of $88.9 million for 2017. The investment portfolio performance was 11.7%, which was achieved with an average cash weighting of 36.1%. The company declared a fully franked full year dividend of 15.0 cents per share which is an increase of 3.4% on prior year and has a conservative balance sheet having a high cash weightage with no debts and a flexible investment approach. By seeing the overall picture, we recommend a “Hold” at the current price of $2.40

Investment Performance (Source: Company Reports)

Australia and New Zealand Banking Group Ltd (ASX: ANZ)

Aiming for better returns: Recently, ANZ Bank informed that New Zealand’s Overseas Investment Office has declined HNA Group’s application to acquire UDC Finance and if it doesn’t materialise then ANZ will assess their strategic options regarding the future of UDC. Meanwhile, ANZ’s FY17 statutory profits were $6.4 billion which were up by 12% and cash profits were $6.9 billion which were up by 18%. Further, the bank has significantly lowered the interest rate on the low rate credit card, easy?to?understand contracts for small business, removed ATM fees and reduced home loan interest rates for owner occupier principal and interest borrowers. The bank’s strategy remains to be ahead of the peers by focusing on only those areas where the bank can deliver exceptional customer outcomes, and is focusing on real customer needs while delivering a decent return for the shareholders. ANZ Bank is one of the largest contributor of corporate tax in Australia and it will also buy back its shares amounting to $1.5 billion in early 2018 based on proceeds from its stake in Shanghai Rural Commercial Bank. We give a “Buy” recommendation on the stock at the current price of $28.89

Super Retail Group Ltd (ASX: SUL)

Outlook for 2018: SUL’s FY17 NPAT was at $135.8 million which is an increase of 25% over the prior year and group’s segment Earnings Before Interest and Tax was $207.3 million which is an increase of 18.3%. SUL’s operating cash flow was $75.3 million higher over the comparative period which was $234.5 million, and the company declared a final dividend of 25.0 cents. They have seen a strong growth in digital sector across all the brands, and grew by 75% for the Auto Division, over 150% in the Leisure Division and 73% in the Sports Division. They have a positive outlook for 2018 and will focus on delivering their strategic pillars and financial targets. SUL is trying to extend their services to their Supercheap Auto customers to offer solutions and not only products. The group will be combining Rebel’s strengths in solutions and services with Amart Sport’s customer service excellence into one strong, national Sports retailer and this will strengthen the competitive position of the Sports Retailing Division in this changing and competitive environment. On the other hand, the annual growth rates indicate that SUL might experience some sluggishness in revenue growth going forward. We give a “Hold” recommendation on the stock at the current price of $8.34

G8 Education Ltd (ASX: GEM)

Acquisition plan on track: G8’s underlying EBIT has been forecasted to be around $160 million for FY17, which is a 5% increase on prior year after adjusting for movements in Long Day Care Professional Development Program Funding. The earnings forecast has been lower owing to factors including softness in occupancy growth. It has also seen an improvement in the team turnover and small indicators of recovery were also seen in Western Australia. GEM has accelerated trainings for G8 team members in various areas to build a high-performance culture and it has resulted into an increase of $1 million of net outflows in respect to Funding Programme as compared to last year. Its acquisition of Oxanda has been successful and is expected to deliver its targeted incremental earnings in 2018; and looking into the market conditions, challenges continue to exist for next 6-9 months, but they continue to implement the changes which are required for the new child care funding package.On the other hand, GEM is tracking well with regards to its acquisition and development pipeline with FY16 and FY17 EBIT contributions of $13m and $3m, respectively.There is an expectation that conditions might move towards stabilisation in the long-term and we give a “Hold” on the stock at the current price of $3.40

National Australia Bank Ltd (ASX: NAB)

Efforts on maintaining liquidity: In September 2017 full year, there was a reduction in statutory profit of $727 million ($500 million after tax) from fair value and it was majorly due to market-to market losses from derivatives which are used to hedge NAB’s long-term funding issuances that are driven by the unfavourable movements in interest rates, foreign exchange rates and cross currency spreads. In September 2017, the group launched seven Customer Journeys which aimed at driving customer advocacy through increased efficiencies and also improving interactions with customers. The group continued to shift its portfolio towards business with higher returns and delivered a statutory return on equity of 10.9% and a cash return on equity of 14.0% on continuous operating basis. NAB has maintained a strong liquidity with quarterly average Liquidity Coverage Ratio (123%) which is above the APRA requirement of 100%. The group also has a capacity to access its funds through the Reserve Bank of Australia under the Committed Liquidity Facility. It has maintained its dividend for the last couple of years and has indicated that it will continue to do so. We recommend a “Buy” on this stock at the current price of $29.45

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...