Stocks’ Details

BHP Billiton Ltd (ASX: BHP)

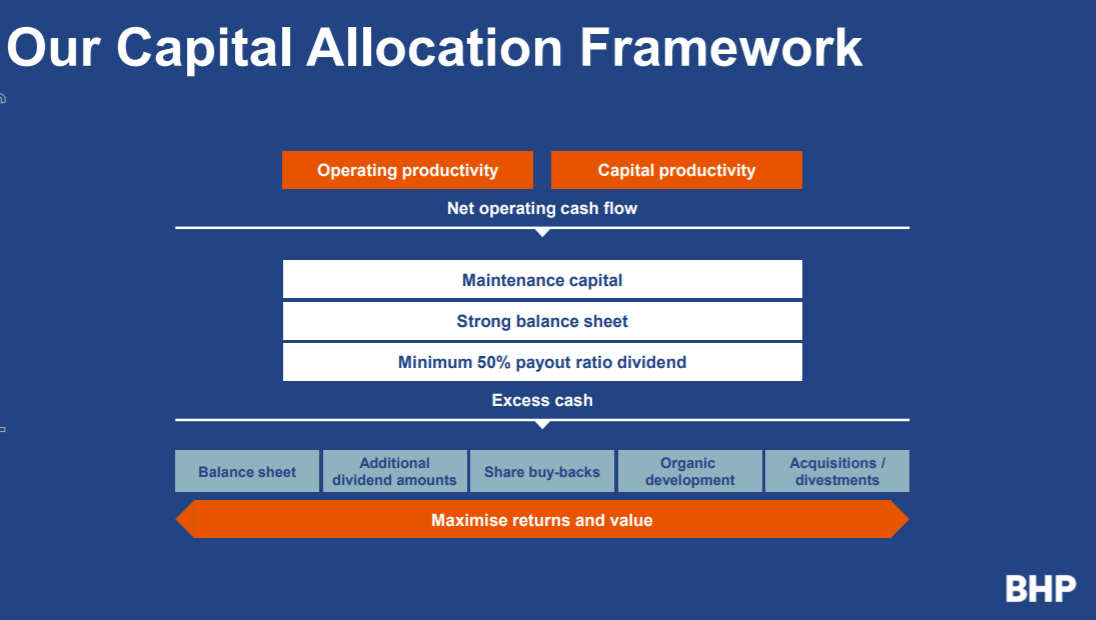

Creating value for shareholders: BHP is expected to benefit from an upgrade in oil prices that is believed to translate into better earnings with Petroleum expected to account for about 20% of FY18 EBITDA. Overall commodity prices also seem to move favourably for BHP. Recently, BHP agreed to fund up to US $181 million in the financial support for the Renova Foundation and Samarco Mineracao S.A till 30 June 18; and out of this US $133 million will be used to fund the Renova Foundation and US$48 will be made available to Samarco. The group has strong plans to grow value and improve returns on capital across the Australian operations. Brownfield Expansion option (BFX) at Olympic Dam is a perfect example of a project which has a potential to deliver sustainable returns to the shareholders, government and local community. The capex is below US$8 billion for FY19 and FY2020. BHP generated strong free cash flow of US$12.6 billion and also reduced the net debt by US$10 billion and US$72.9 million were voluntarily invested in the social projects.The group will seek Board’s approval for the South Flank project with submission to be made in mid of 2018 and first ore targeted for 2021. In 2017, it successfully achieved its five-year target to keep the greenhouse gas emission below their 2006 baseline and now it aims to limit 2022 greenhouse emissions at or below 2017 levels. With more upside expected in 2018, we recommend a “Buy” at the current price of $30.33

Capital Allocation Framework (Source: Company Reports)

Australia and New Zealand Banking Group Ltd (ASX: ANZ)

Capital management: ANZ’s buy-back plan’s quantum of about $1.5bn looked modest and the earnings are expected to get some lift with the better 2018 capital management plan. ANZ has recently sold its superannuation, adviser network and investments arm to IOOF for $975 million and was looking to offload its life insurance business. The Bank also sold its residential mortgages to the NZ Branch. It then completed the simplification of its Wealth Australia division with the sale of its life insurance business to Zurich Financial Services and the sale consideration comprised of two transactions with total proceeds of $2.85 billion and $1 billion inclusive of upfront reinsurance commission from Zurich. At present, ANZ Bank’s shares provide a decent trailing fully franked dividend and capital ratios have increased mainly due to the reduction in the underlying credit RWA in Institutional, cash earnings generation and benefit from the partial settlement of the Asia Retail and Wealth sale, while this was offset by interim dividend payments and implementation of ANZ’s new Australian mortgages capital model. ANZ carried a BB+ credit rating from S&P as on 30 September 2017. ANZ trades at about 12.9x 12-month prospective earnings and looks to be a good opportunity in the long-term despite the royal commission in the financial sector. We give a “Buy” recommendation at the current price of $28.52

Ramsay Health Care Ltd (ASX: RHC)

Poised to leverage its growth strategy: Looking at the financial performance, RHC’s FY17 revenue increased by 0.2% on previous year and EBIT also increased by 5.2% on previous year, Moreover, EPS also grew by 13.0% over the previous year. Despite the challenges it faced in Europe, it still managed to invest in its facilities appropriately at the right time to meet the growing demand for its services. It also acquired a healthcare transport business in Lyon in France. Its vision is to develop as a leading health service provider on the global stage. As on 30 June 2017, group’s Consolidated Leverage Ratio was 2.2 times which is within its internal parameters. Major expansions are on its way and include St Andrew’s Private Hospital in lpswich, Albert Road Clinic in Melbourne, Warners Bay Private Hospital in Newcastle and the new Northside Clinic in Sydney. The group also has potential for out-of-hospital growth opportunities in its adjacent businesses like retail pharmacy across all the markets in which it operates. Meanwhile, RHC stock has risen 11.46% in three months as on January 03, 2018. Given the potential, boost from private insurance reforms, and macro industry trends, the group seems to be well placed to meet EPS growth target of 8% to 10% in FY18 with continued margin expansion; and we put a “Buy” recommendation on the stock at the current price of $70.60

Growth Strategy (Source: Company Reports)

Aristocrat Leisure Ltd (ASX: ALL)

Focussing on efficiency improvement: Aristocrat delivered a strong performance over the 2017 fiscal year which further extended the business track record of consistent and high-quality growth in NPATA. Group revenue increased by more than 15% in reported terms over prior year. Operating cash flow also increased by more than 17% and net gearing reduced to 0.6x from 1.2x compared to the prior year. NPATA also increased by 36% as compared to previous year. A robust balance sheet ensures that ALL can continue to promote shareholders long-term interest by investing for growth both organically and inorganically. It also acquired Plarium Global Ltd for a total consideration of US$500m in cash which increased its presence in the high-growth social games market and also expanded its digital market as it successfully acquired Big Fish which is one of the top six digital social casino game publishers globally. Directors recommended the payment of a final dividend of 20.0 cents per fully paid ordinary shares. A strong growth was seen in Americas as business drove a $109 million improvement in post-tax profits as compared to prior year. Digital also generated a strong growth of $31.7 m due to the successful launch of Heart of Vegas and Cashman Casino. As on 30 September 2017, ALL held a credit rating of BB+ from S&P and Ba1 from Moody’s. On the other hand, foreign exchange impacted the business performance by $18.3 million which was partially offset by a decrease in interest. Group’s success and profitability is dependent on its ability to successfully enter new segments in the existing markets and in the new markets and channels including mobile and online gaming. Further, group’s move on acquisition of Big Fish has raised concerns with regard to the amount paid. We believe that the stock is still “Expensive” at the current price of $22.96, and would look for a better buying opportunity.

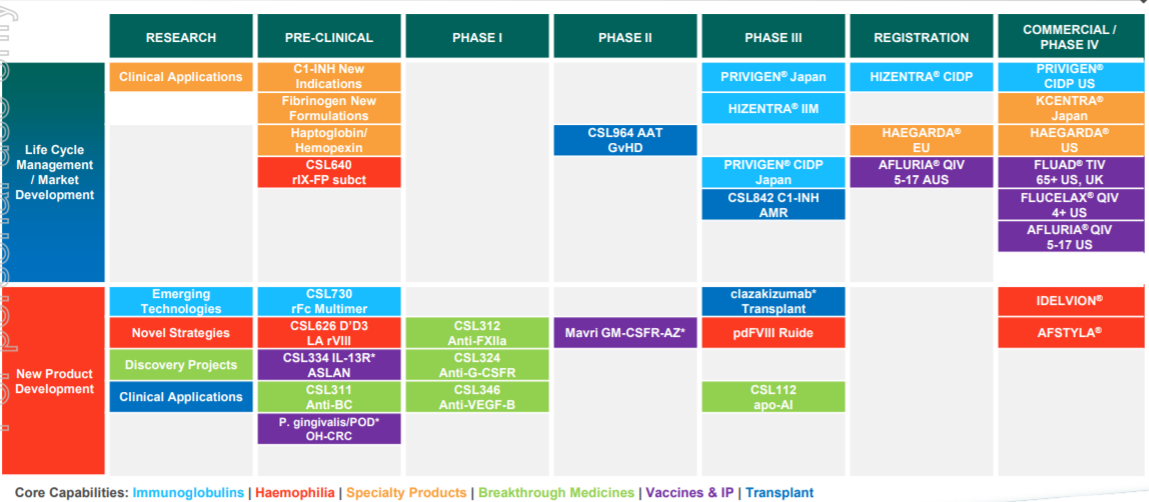

CSL Ltd (ASX: CSL)

Focussing on valuable products: Recently, Paragon Care Limited (a CSL Company) announced that it acquired the Immunohaematology business unit from Seqirus for a total consideration of $8.5m. This acquisition will be funded internally via the existing debt facility and cash reserves and this acquisition will provide sustainable and solid long-term growth opportunities for Paragon Care. The business also enjoys deeply embedded relationships in the Australian Blood Banking and Pathology Industries.

R&D Progress as at December 2017 (Source: Company Reports)

In addition to the acquisition of Seqirus immunohaematology, the Company also entered into the final stages on the small to medium acquisitions which are likely to be finalised over the coming months. Meanwhile, CSL is setting itself high with products such as CSL112 to address the unmet medical need with commercial strategy already planned. Peaking close to 52-week high level, we believe that the stock is “Expensive” at the current price of $141.55

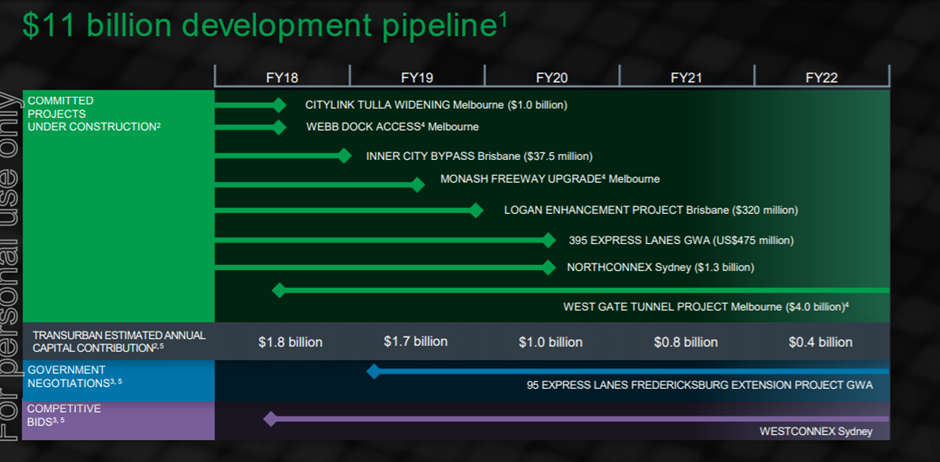

Transurban Group (ASX: TCL)

Encouraging outlook despite high levels: Transurban completed the despatch of its Retail Information Booklet and of the personalised entitlement and acceptance forms to Transurban security holders who are eligible to participate in the retail component of Transurban’s pro rata accelerated renounceable entitlement offer relating to the new Transurban staples securities. It also successfully completed its Institutional Entitlement Offer through which it raised gross proceeds of approximately A$1.35 billion. It has a positive outlook with FY18 distribution expected to be approximately 100% covered by free cash and includes 5.0 cps fully franked dividend and the new securities which will be issued will be entitled to FY18 second half distribution which is expected to be 28.0 cps.

Pipeline for Economic Benefits (Source: Company Reports)

One of the key projects is West Gate Tunnel Project that is targeted to deliver good economic benefits. An internal rate of return of over 10% might emanate from the project with a value of over $2bn. Transurban has achieved contractual close with the State and the construction phase has commenced to build, toll and operate WGTP until 2045. The stock is also expected to get a boost from the overall infrastructure industry trends, and we put a “Buy” recommendation at the current price of $12.23

Suncorp Group Ltd (ASX: SUN)

Performance expected to continue:SUN’s 1Q18 APS330 (Australian Prudential Standard) update indicates for another healthy upcoming year with decent credit quality (CET1 ratio of 8.77% within operating range and better lending growth). Meanwhile, ASX announced that Suncorp’s convertible preference shares will be removed from the official quotation immediately after the completion of the redemption of these securities. Further, a $1.5bn capital effective Residential Mortgage Backed Security transaction was issued to support funding stability. Lately, the group indicated to issue Suncorp Capital Notes 2 to raise $250 million for funding one or more regulated entities, as well as for generalcorporate and funding purposes. It delivered FY17 net profit after tax (NPAT) of $1,075 million, and for the first time Suncorp reported an increase in the customer number, with 399,000 new customers joining the group. Its top line growth has been supported by the entry into the South Australia and it focuses on delivering the value to customers, which places the group at a strong position. In terms of its CET1 position, its general insurance businesses CET1 position was 1.32 times the prescribed capital which is above its targeting operating range of 1.0-1.2 times PCA (prescribed capital amount).The stock is trading at slightly higher levels, and we maintain a “Hold” at the current price of $13.83

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...