As per the recent US Tax Reform, the US corporate tax rate will be sharply reduced to 21% from 35%, which looks to be a boon to the income statements of most of the companies having operations in the US. The outcome is still uncertain; however, many investors have started planning on investments with regards to their portfolio keeping the criteria that lower taxes would result in higher profits for the companies which will lead to higher share prices. Below are key stocks that have significant exposure to the US region and are expected to be impacted by the US tax Reform.

Stocks’ Details (Price movements as at December 21, 2017)

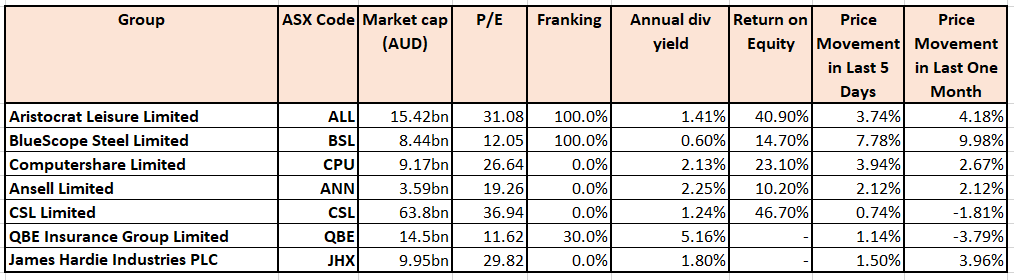

Aristocrat Leisure Limited (ASX: ALL)

This year, Aristocrat’s Digital business transformed into 2nd largest Social Casino business globally in respect of revenue, and the group entered into a binding agreement to acquire 100% of Big Fish (world’s largest developers of Social casino, Social Gaming and Premium Paid games) for a total consideration of US$990 million in cash but this has been subject to customary completion adjustments and has increased overall Digital revenue by 94%. Aristocrat will also fund the acquisition via US$890 million Term Loan B debt facility. ALL’s revenue has increased by more than 15% in reported terms and over 18% in constant currency this year to a record of over $2.45 billion. The group also completed the acquisition of Plarium Global Limited for a total consideration of US$500m by way of cash. It holds credit rating of B++ from Standard and Poor and Ba1 from Moody’s. It is worth noting that ALL has an earning exposure of about 70% from the US. Though there is good potential, ALL is trading at a high level and looks “Expensive” at the current price of $23.83, and will be worth a watch going forward.

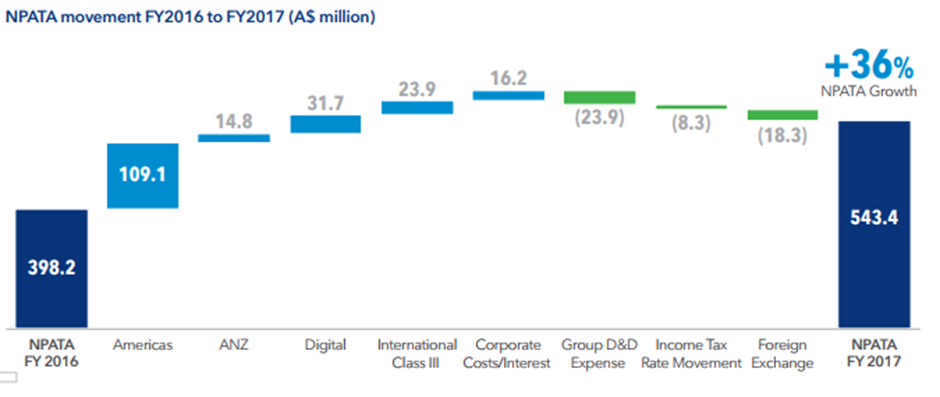

NPATA’s Summary (Source: Company Reports)

BlueScope Steel Limited (ASX: BSL)

Recently BlueScope announced that it expects underlying earnings before interest and tax for the six months ended 31 December 2017 to be around $460 million as compared to the prior guidance which was provided in August of $420 million. In November, it performed well as steel prices were high and a higher contribution was achieved due to export of coke which was approximately $20 million. Currently, steel macro conditions are positive but there is going to be a strong competition from imports. BSL expects its US earnings to benefit through a lower federal tax rate with an anticipated 7% decrease in 2018 that will be partly offset by a toll charge on foreign earnings which is immaterial. The group, which trades at a higher level in the current scenario, is dependent on the US for a good portion of its earnings and hence the tax reform is expected to be in favour of the group.

Computershare Limited (ASX: CPU)

As per the new US tax reform, the corporate tax rate got reduced from 35% to 21%, and this will lead to some tax reductions for Computershare as well. As per the preliminary assessment of the implications of the Act for Computershare, it will generate one-time FY18 statutory NPAT benefit associated with the reduction of Computershare’s US net deferred tax liability, but this benefit will be excluded from Computershare’s Management earnings. The group has a good chunk of its earnings emanating from US. CPU is also undertaking a detailed evaluation of the other implications of the Act like inclusion of the new interest expense limitation rule, anti-base erosion rule and anti-hybrid rules. Overall, this new update will be a catalyst for better returns in future, so it might be worth considering any dip in the stock, which is currently trading at a high level.

Ansell Limited (ASX: ANN)

Ansell Limited is a global leader in protection solutions and it also provided a recent update on US tax reforms, which will help the group generate a profit after tax of US$3-5 million per annum by FY19. The reduction in the amount of interest expense deductible is not expected to have any material tax expense impact on group results which will be based on current US debt levels. The restatement of previously recorded Net Deferred Tax balance is expected to provide a one-off tax expense benefit which will be in the range of $18-$22 million in FY18, which includes a benefit arising from the changes in US corporate tax rate on US deferred tax liabilities. This will be partially offset by the unfavourable impact which is expected on the rate changes on deferred tax balances in other jurisdictions in which Ansell conducts operations. The company also announced buy-back of its shares which was of total 33,770,461 million FPO shares. It was reported that NPAT was down by 7.17% to $147.7 million for the year ending on 30 June 2017; and on the other hand, revenue was up by 1.7% from last year and there was a slight increase in dividend as compared to last year. Given the mixed scenario, investors may want to evaluate an opportunity considering the above shortcomings and risk.

CSL Limited (ASX: CSL)

CSL is another company that is considered to have an impact from the reform. The group is on track with many of its key products performing as expected. Progress on its breakthrough therapy, CSL112, for cardiovascular events is also tracking well and this is said to be the largest ever undertaken by CSL. Almost 20% of group’s earnings are contributed by the US operations and the group expects its NPAT in the range of $1,480 million - $1,550 million for FY18. Bio21 expansion is also expected to be completed by Feb 2018, so by looking at the overall picture, 2018 is going to be a very crucial year for CSL, which is trading at a higher level already.

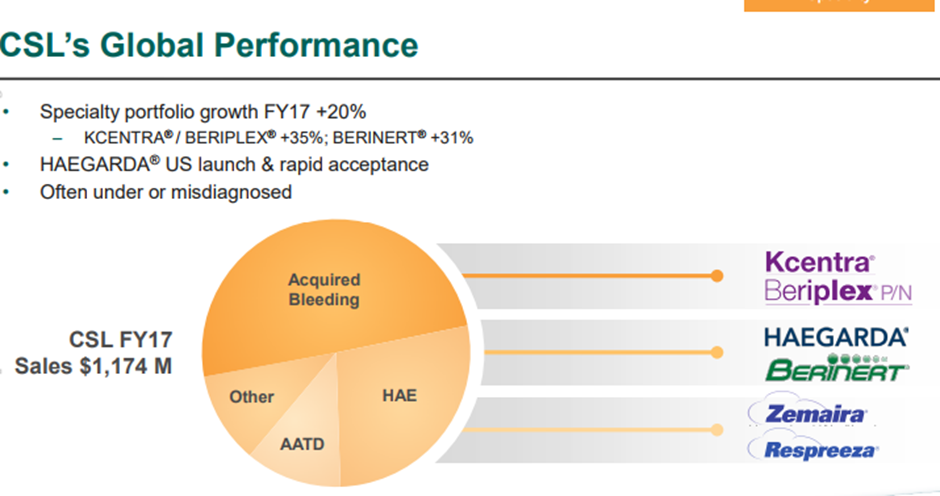

Global Performance (Source: Company Reports)

QBE Insurance Group Limited (ASX: QBE)

Few months ago, QBE Insurance Group advised that the 'A+' financial strength ratings on QBE’s core operating Companies and 'A-' issuer credit rating (ICR) on the Company have been affirmed by S&P Global Ratings. It is also worth noting that Moody’s maintained stable rating outlook on QBE’s financial strength and senior unsecured debt ratings despite the weakened earnings for FY17.Due to the increase in the number of natural calamities in 2017, QBE’s earnings were dented and were below its expectations. It will be worth a watch that how the group performs based on the impact from the tax reform.

James Hardie Industries PLC (ASX: JHX)

US centric-firm, James Hardie has more than half of their profit in the US, and has recently offered wholly-owned subsidiary senior notes. The proceeds from these offerings will be used for general corporate purposes like repayment of outstanding borrowings and other capital expenditure. Group’s net sales were US$525.8 million for the second quarter of the fiscal year 2018 and US $1,033.5 million for the second half of the year 2017 which is an increase of 6% in both the periods when compared to prior corresponding periods, and management expects its full year adjusted net operating profit to be between US$245 million and US$275 million assuming housing conditions to improve in the United States.Investors wait to see the results after the challenging FY17 performance wherein capacity constraints and pressure at North American fibre cement business impacted growth.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...