Zoono Group Limited

.png)

ZNO Details

ZNO Informs COVID-19 results Relating to its Supply Deal With EAGLE: Zoono Group Limited (ASX: ZNO) helps in producing, manufacturing and distributing a set of scientifically validated, long-lasting and ecologically friendly antimicrobial solutions. On 28 February 2020, ZNO updated the market relating to its existing Distribution Agreement with Eagle Health Holdings Limited, wherein the latter will distribute ZNO’s products in China. ZNO notified Eagle that it’s Z-71 Microbe Shield Surface Sanitiser has recently given successful laboratory test results against Coronavirus COVID-19 (more than 99.99% effective results). The company remains assured that it is well placed to be part of the solution to both coronavirus and other new virus threats.

Other Recent Update: The company recently stated that Regal Funds Management Pty Ltd, has become a substantial holder of the company with a voting power of 9.18%. In another update, the company notified that Paul Russell Hyslop, Margaret Jane Morgan and NPT MEG Trustee Limited, that together form substantial holders of the company, have reduced their voting power from 51% to 41%.

1HFY20 & December Quarter Key Highlights: Total revenue for the period amounted to NZ$1.71 million, up by 144% year over year on the back of higher orders received from current and new distributors. Net loss after tax for the period amounted to NZ$727.9k, against a net loss of NZ$1.38 million reported in the prior corresponding period. For the current quarter, the company reported unaudited revenues of NZ$3.5 million. ZNO’s cash resources for the quarter stood at NZ$4.0 million, up from more than NZ$1.0 million as on 31 December 2019.

.png)

Income Statement (Source: Company Reports)

What to Expect: The company remains on track to rampup production and relocate to a considerably bigger warehouse and office facility in early March 2020. The company also aims to order 4 million bottles and hire more staff to cope with the increased demand for its products.

Stock Recommendation: The stock of ZNO is trading at $2.26 with a market capitalization of $309.48 million. The stock is trading at the upper band of its 52-week trading range of $0.063 to $2.440.The stock has delivered exponential returns of ~577% and 2646% in the last three months and six-months, respectively. On the valuation front, the stock is available at an enterprise value to sales multiple of 157x on trailing twelve months (TTM) basis as compared to the industry average of 84.4x. Considering the aforesaid facts, price movements, and current trading levels, we believe that most of the positives are factored in at the current juncture. Hence, we have a watch stance on the stock at the current market price of 2.26, up 19.261% on 02 March 2020 on account of the recently announced distribution agreement and testing results of its products against coronavirus impact.

.jpg)

ZNO Daily Technical Chart (Source: Thomson Reuters)

Atlas Arteria

.png)

ALX Details

NPAT for FY19 Increased 9% Year Over Year: Atlas Arteria (ASX: ALX) is engaged in operating and managing a portfolio of toll road assets. As on 02 March 2020, the market capitalisation of the company stood at ~$7.05 billion. Recently, the company announced that it has appointed Sheena Dottin as the company’s Secretary following the resignation of Andrew Davidson.

Debt Refinancing Update: ALX informed the market that APRR and Eiffarie SAS have jointly refinanced €2.87 billion of debt facilities, which consisted of €1.07 billion term loan at Eiffarie and a €1.80 billion revolving credit facility at APRR. Both the facilities will be maturing in February 2022.

FY19 Financial Highlights for the Period Ended 31 December 2019: ALX announced its FY19 financial results wherein, the company reported revenues and other income of ~$175.2 million, as compared to $132.5 million reported in FY18. The company reported net profit after tax amounting to $178.2 million, up 9% year over year, majorly due to growth in net profit from APRR along with robust growth in net earnings at Warnow Tunnel. Traffic at APRR continues to grow, with 1.1% rise on a year over year basis.

.png)

FY19 Financial Highlights (Source: Company Reports)

What to Expect: The company has provided distribution guidance of 18 cents per share for 2H FY19 as well as 1HFY20, up 6% from the previous guidance.It added that the distribution guidance remains subject to asset performance, movements in foreign exchange rates, French tax rate changes as well as future events.

Valuation Methodology:P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of ALX is quoting at $7.900 with an annual dividend yield of 3.74%. The stock is trading at the upper band of its 52-week trading range of $6.675 to $8.54. The stock has delivered a positive return of ~14.4% in the past one year. We have valued the stock using P/E based relative valuation approach and for the purpose, we have taken the peer group - Transurban Group (ASX: TCL), Reece Ltd (ASX: REH) and Seven Group Holdings Ltd (ASX: SVW). We have arrived at a target price correction of single digit (in percentage terms). Therefore, we have a watch stance on the stock at the current market price of $7.900 per share, down by 1.496% on 2 March 2020.

.jpg)

ALX Daily Technical Chart (Source: Thomson Reuters)

A.P. Eagers Limited

.jpg)

APE Details

Revenues up a Whopping 41.4% Year Over Year: A.P. Eagers Limited (ASX: APE) is involved in the sale of new and used motor vehicles, distribution of parts, accessories, car care products, and the repair and servicing of motor vehicles. Recently, the company announced that it will distribute a dividend of $0.225 per share, with an ex-date of March 31, 2020 and payment date of April 20, 2020.

APE Inks Deal With Anchorage to Sell its AHG Refrigerated Logistics division: On 27 February 2020, APE entered into a binding agreement to sell Automotive Holdings Group Limited’s Refrigerated Logistics division (a subsidiary of APE) to Anchorage Capital Partners for a consideration of $100 million on a debt and cash free basis.Notably, the move will follow the reduction in APE's net debt of ~$95 million. The sale transaction is expected to be completed in the 1HFY20, subject to closing market conditions.

FY2019 Performance Highlight: Statutory revenue in FY19 witnessed a growth of 41.4% year over year to $5.8 billion. Underlying EBITDA increased by 15.6% year over year to $163.2 million. Underlying profit after tax decreased 3.1% year over year and came in at $69.2 million in FY19. The company reported a total dividend of 36.5 cents in FY19, flat year over year.

.png)

FY19 Income Statement Highlights (Source: Company Reports)

Outlook: The company expects to deliver improved operational performance via ongoing integration of AHG including realisation of targeted $30 million in synergies, divestment of non-core assets and successfully controlling the exit of Holden.

Valuation Methodology:P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock has gained around 14.7% returns in the past one year with an annual dividend yield of 4.11%. As on 02 March 2020, the market capitalisation of the company stood at ~$2.28 billion. We have valued the stock using P/E based relative valuation method and for the purpose, we have taken the peer group - Autosports Group Ltd (ASX: ASG), Iress Ltd (ASX: IRE), Inghams Group Ltd (ASX: ING), to name few. We have arrived at a target price offering a correction of single-digit (in percentage terms). The stock is trading at the lower band of its 52-week trading range of $7.1 to $14.49. Considering the aforesaid facts, price movements, and current trading levels, we have a watch stance on the stock at the current market price of 8.45, down 4.842% on 02 March 2020.

.jpg)

APE Daily Technical Chart (Source: Thomson Reuters)

Bendigo and Adelaide Bank Limited

.png)

BEN Details

Robust Customer Growth Remains a Key Catalyst: Bendigo and Adelaide Bank Limited (ASX: BEN) is engaged in providing an array of financial services like retail banking, mortgage distribution, business lending, margin lending, business banking and commercial finance. Recently, the company announced that it has paid an interest of 1.9%per annumon the security - HYBRID 3-BBSW+1.00% PERP SUB CUM RED. Interest amount per security stood at$0.4789. In another update, BEN stated its intention to non-underwriteShare Purchase Plan (“SPP”), under which shareholders can apply for up to $15,000 new fully paid ordinary shares in BEN. This follows the successful $250 million completion of institutional share placement at a price of $9.34 per share.

H1FY20 Key Highlights for the Period ended 31 December 2019: BEN reported its half yearly results, wherein statutory net profit after tax came in at $145.8 million, down 28.2% year over year, which includes a pre-tax software impairment of $87.1 million and accelerated amortisation of $19.0 million. Total income stood at $814.7 million, up 1.4% on pcp. The company declared a fully franked dividend of $0.3100 per share. Robust customer growth of 4.9% on pcp terms is a key catalyst, despite a challenging environment and Coronavirus impact.

.png)

Key H1FY20 Operational Highlights (Source: Company Reports)

What to Expect: The company expects its mortgage lending growth rates to surpass system, with persistent growth in the small business portfolio and the Commercial Real Estate business.

Valuation Methodology:Price to Book Value Based Valuation

.png)

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The market capitalisation of BEN stood at ~$4.78 billion as on 2 March 2020. The stock has corrected around 16.45% in the past six months. As per ASX, the stock is trading at the lower band of its 52-week trading range of $8.820 and $11.74, with a P/E multiple of 14.14 and annual dividend yield of 7.18%. Considering the price performance and customer growth, we have valued the stock using price to book value based relative valuation method. For the purpose, we have considered peers like Bank of Queensland Ltd (ASX: BOQ), Virgin Money UK PLC (ASX: VUK), Australia and New Zealand Banking Group Ltd (ASX: ANZ), and arrived at a limited upside (in % terms). Hence, we have a watch stance on the stock at the current market price of $9.01 per share, down 1.959% as on 2 March 2020.

.jpg)

BEN Daily Technical Chart (Source: Thomson Reuters)

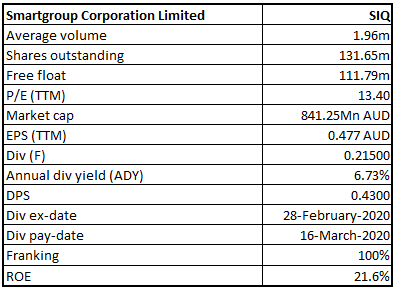

Smartgroup Corporation Ltd

SIQ Details

Revenues up 3% Year Over Year in FY19: Smartgroup Corporation Ltd (ASX: SIQ) is engaged in salary packaging administration and fleet management services. The market capitalisation of the company stood at $841.25 Mn as on 2 March 2020. The company recently announced that Mitsubishi UFJ Financial Group, Inc has ceased to be a substantial holder in the company on 26 February 2020. In another update, the company stated that Ian Watt, one of the Directors of the company, has acquired 5,000 ordinary shares for a consideration of $35,500.

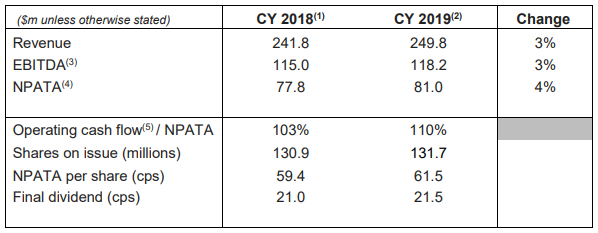

FY19 Key Highlights: Revenue for the period was reported at $241.8 million, an increase of 3% year over year. Profit after tax, as measured by NPATA, for the period was reported at $77.8 million, up 4% as compared to the previous corresponding period. EBITDA for FY19 stood at $115 million, up 3% year over year. The Board of Directors declared a final dividend of 21.5 cents per share for FY19.

FY19 Financial Highlights (Source: Company Reports)

Focus Areas: The company continues to focus on increasing the adoption of digital channels and automation. The company also remains focused on operational excellence as well as improving customer outcomes. Strong cashflow generation with flexible balance sheet is a key positive.

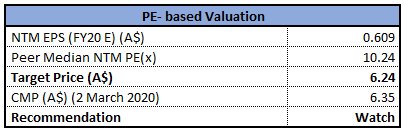

Valuation Methodology: P/E based Valuation

P/E-Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock has corrected around 43.65% in the past six months. As per ASX, the stock is trading at the lower band of its 52-week trading of $6.080 and $12.65, with a P/E multiple of 13.4 and annual dividend yield of 6.73%. We have valued the stock using price to earnings based relative valuation method. For the purpose, we have considered peers like Mcmillan Shakespeare Ltd (ASX: MMS), SG Fleet Group Ltd (ASX: SGF), Service Stream Ltd (ASX: SSM), and arrived at a correction of lower single digit (in % terms). Hence, considering the expected correction in valuations, in combination with the full year 2019 earnings release, and current trading levels, we have a watch stance on the stock at the current market price of $6.35 per share, down 0.626% on 2 March 2020.

SIQ Daily Technical Chart (Source: Thomson Reuters)

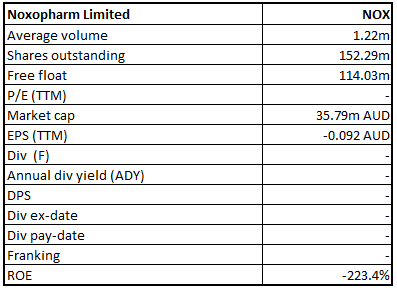

Noxopharm Limited

NOX Details

Approval Received from US-FDA: Noxopharm Limited (ASX: NOX) is a pharmaceutical and biotechnology company with a market capitalisation of $35.79 Mn as on 2nd March 2020. The company recently achieved the U.S FDA approval for the Investigational New Drug (IND) application for Veyonda® for combination treatment with doxorubicin in patients with soft tissue sarcomas. Veyonda® has a strong chance of being a treatment drug of late-stage prostate cancer.

During February 2020, the company has issued buy back and termination notices to The Lind Partners, LLC and CST Investment Funds with respect to existing convertible notes. On 18th February 2020, NOX paid $4.085 million for reducing the convertible loan balance to zero.

Consolidated Profit & Loss (Source: Company Reports)

Focus for FY20:The company would continue working towards a potential listing of its securities in the U.S. Looking at the performance in 2HFY19 and the first 2 months of FY20, the company is confident about achieving the milestones for future. Veyonda® has received good response as per the clinical data and has marked the beginning of commercialization for Noxopharm, with marketing approval for Veyonda® in the U.S and Europe.

Stock Recommendation:During FY19, the company experienced a decent improvement in its key margins. Debt to equity multiple of the company stood at nil in FY19 as compared to the industry median of 0.15x. During the span of three months and six months, the stock of NOX has corrected 36.49% and 39.74%, respectively. Hence, considering the corrections experienced during past months, we have a wait and watch stance on the stock at the current market price of $0.240 per share, up by 2.128% on 2nd March 2020.

NOX Daily Technical Chart (Source: Thomson Reuters)

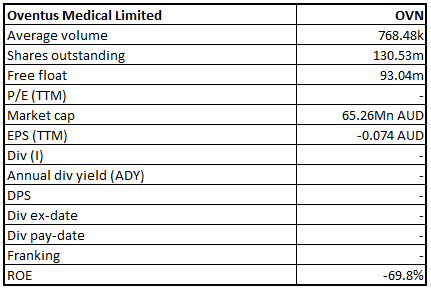

Oventus Medical Limited

OVN Details

Agreement with Aeroflow:Oventus Medical Limited (ASX: OVN) is engaged in the development of oral devices for therapeutic treatment of breathing disorder, especially sleep apnoea. The market capitalisation of the company stood at $65.26 Mn as on 2nd March 2020. The company recently inked an agreement with Aeroflow Healthcare Inc, which possesses a term of three years along with an automatic 3-year renewal, unless a party elects not to renew no later than 180 days prior to the end of the three-year period.

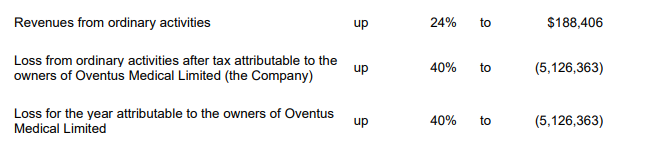

Under the scope of the agreement, the sleep treatment platform of OVN including O2Vent Optima and consumables would be introduced by Aeroflow across its locations, direct-to-consumer e-commerce platform and via agreements with referring sleep clinics across the Southeastern US states. The below picture provides an overview of the financial performance of 1H FY20:

Financial Performance (Source: Company Reports)

Plans for Future Year:Going forward, the company anticipates significant progress in generating sales of the O2Vent range. OVN expects additional partnerships for clinical delivery and distribution in various geographies. Subject to FDA approval, it is planning to rollout new products in the US Markets.

Stock Recommendation:Gross margin of the company stood at 67.5% in FY19, reflecting YoY growth of 5.9%. Current ratio of the company stood at 2.91x in FY19 as compared to the industry median of 2.47x. This reflects that the company is in a decent position to address its short-term obligations against the broader industry. As per ASX, the stock is trading slightly above its 52- week low-high average. We would like to see how the company spans out its future commitments for the launch of new products in US markets. Therefore, considering the afore-mentioned facts, we are of the view that most of the positive factors are discounted at the current levels. Hence, we have a watch stance on the stock at the current market price of $0.540 per share, up by 8% on 2nd March 2020 and suggest the investors to wait for further catalysts to drive the growth.

OVN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...