.png)

Stocks’ Details

XERO Limited

Robust Subscriber growth & AMRR Trends: Xero Limited (ASX: XRO) offers an online accounting system. The software features bank transaction importing, a cashbook, a general ledger, invoicing, accounts receivable, accounts payable, financial reporting, and management of expense claims. The operating revenues for the 1H FY2019 came in at $256.5 Mn exhibiting a rise of 37% over PCP. This was achieved on the back of phenomenal growth seen in the Average Monthly Recurring Revenue (AMRR) which stood at $589.1 Mn. Also, the average revenue escalated by 6% to reach $31.09 for the first half year 2019. The underlying EBITDA came in at $16.8 Mn in 1HFY19, showing decent growth of 7% on PCP basis. This growth in EBITDA was on account of the reduction in the cost of revenue driven by the continued efficiencies in the hosting costs and other productivity gains realized from investment in the customer service platform. However, the EBITDA was adversely impacted by a non-cash asset impairment of $16.3 Mn on account of the Gusto partnership & $2.3 Mn of transaction cost & operating losses from the acquisition of Hub lock. Going forward, the company will continue to concentrate on its global business platform and expects to reduce cash outflows for FY19 from the levels attained for FY 2018. Xero is focused on managing its business in a manner that aid in achieving cash flow break even within its current cash balance without the requirement of any debt.

.png)

XRO’s revenues segmented by geographies (Source: Company Reports)

Meanwhile, the share price has fallen 16.22% in the past three months as at November 19, 2018 and traded below the average of 52 week high and low prices of $39.19. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $37.62.

NetComm Wireless Limited

Robust cash flows coupled with expected 5G rollout: NetComm Wireless Limited (ASX: NTC) designs, manufactures and distributes communication and networking devices including analogue modems, wired and wireless networking devices, routers, and ADSL modems. The Company distributes its products to retailers, telecom carriers and Internet service providers. The EBITDA for the FY2018 came in at $20.5Mn exhibiting a rise of 472.4% over PCP. This was achieved on the back of major revenues garnered by the two major segments namely the telecommunication infrastructure equipment and the industrial internet of things (IIOT) in the key markets i.e., Europe, UK & North America. On the business segmental front, telecommunication infrastructure equipment BU contributed 86.1% in total revenue in FY18 and rest came from the Industrial Internet of Things (IIOT) business segment. NPAT was clocked at $8 Mn in FY18 while the firm had recorded a net loss after tax of $1.8 Mn in the prior year. As a result, return to the shareholders also turned around to be positive and recorded 4.7% during the same period.

.png)

Telecom Equipment Market Growth Trends (Source: Company Reports)

There are attractive market fundamentals which are expected in the upcoming years as the company has been at the forefront of keeping itself ready for the 5G roadmap. The 5G rollout will notably open up new avenues in terms of geographical markets. As per the company’s guidance for FY 2019, the revenues are expected to grow at 15-20% as compared to the prior year. This forecast growth is slightly down due to a slower than expected rollout of the nbn FTTC project and AT&T Fixed Wireless project. Moreover, the EBITDA margins are expected to be around similar levels to FY18 on account of revenue growth offset by the margin contraction. Meanwhile, the share price has fallen 36.32% in the past three months as at November 19, 2018 and traded close to lower level. Hence, we maintain our “Hold” recommendation on the stock at a Current market price of $0.745.

Appen Limited

Upwardly Revised EBITDA Guidance for Full Year: Appen Limited (ASX: APX) is a language, search, and social technology company. The Company provides solutions to improve the internalization of products, management of data, and project management for companies. The company has recently upgraded its earnings estimate for the FY ending 31 December 2018 stating that the underlying EBITDA for the full year is expected to be in the range of $62 Mn to $65 Mn, representing growth of between 10.2% and 14.8% as compared to the previous guidance of $54Mn to $59 Mn, respectively. These revised earnings forecasts are on account of the growth in the monthly revenues from the existing projects & customers. However, the actual earnings might surprise on either side on account of foreign exchange fluctuations & the timing of work from major customers. On the other hand, the half-year saw an expansion of around 100% in the EBITDA. This was on the back of strong “Content Relevant” revenue garnered from the acquisition of Leapforce & also the incremental work from existing customers. However, at the same time EBITDA margins contracted by 52 bps and were reported at 16.8% in 1HFY18 due to the change in language resource mix of the work during the period. Underlying NPAT stood at $17.8 Mn in 1HFY18, exhibiting strong growth of 119% on Y-o-Y basis. This was on account of the reduction in effective tax rate from 30.3% to 21.2% due to the availability of credit on tax paid upon employee share issue.

.png)

1HFY18 Financial Highlights (Source: Company Reports)

The company is continuously experiencing traction in demand due to the need for data privacy and commercial confidentiality. The firm’s new platform “Appen Connect” is poised to improve the scalability & productivity. Also, the new customer wins in the technology sector and early project wins in China could be the growth drivers. However, considering the recent run in the stock of 18.66% in the past five days we believe that the positives are already discounted at the current juncture. Hence, we maintain our “Expensive” recommendation on the stock at the Current market price of $13.0.

Nearmap Limited

Stellar growth in US ACV’s coupled with growing geospatial mapping market: Nearmap Limited (ASX: NEA) is involved in the geospatial (mapping) market. The Company supports the government and corporate customers through its online-based mapping content. The operating revenue for the FY 2018 came in at $54.1 Mn a rise of 32% over PCP. This was on the back of continued customer retention & the rapid growth achieved in its customer base. Also, the above growth was because the ACV (Average contract revenue) portfolio of the Australian operations, which grew by 22% to reach $48.8 Mn & simultaneously the US portfolio increased by a stellar 142% to arrive at US$12.9 Mn. Further, the consolidated Net loss after tax was clocked at $11 Mn. This was on account of the expanded capture cost that the company had to incur due to the rollout of “HyperCamera2” systems, thus leading to an incremental cost of 28% on PCP. Moreover, the technology & general operations and Depreciation & amortization expenses escalated by 57% and 113%, respectively.

.png)

NEA’s ACV, Subscription & ARPS Growth Trends (Source: Company Reports)

For the Quarter ended 30 September 2018, the group portfolio denoted by ACV exceeded $70 Mn. This was on account of robust performance across all its channels and enhanced integrity and scalability of its operations. The company is poised for the long-term growth as the global market for the Geospatial mapping and it is expected to grow at a CAGR of 14.6% and hence reach $4.5 Bn by the end of 2025. Moreover, the firm has got adequate cash resources which it can use to achieve strategic M&A objectives. In the meantime, the share price has risen 71.66% in the past six months as of November 19, 2018 and traded close to higher level. Based on foregoing and current trading level, we maintain our “Hold” recommendation on the stock at the current market price of $1.580.

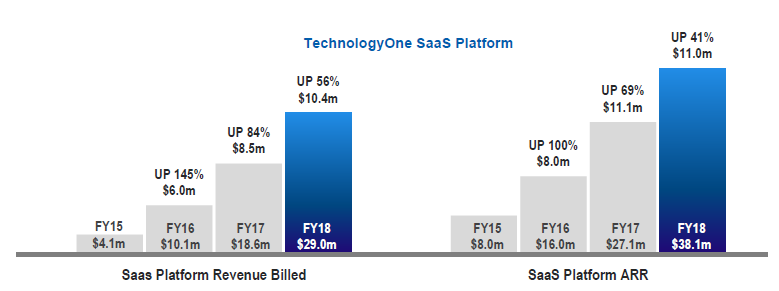

Technology One Limited

Robust SaaS performance along with Growth in License fees: Technology One Limited (ASX: TNE) is an Australian-based company that is engaged in the development, marketing, sales, implementation, support, and distribution of financial management and enterprise software solutions. The Company has operations in New Zealand, the United Kingdom, the South Pacific, and Malaysia. The operating revenue for the FY 2018 came in at $ 299 Mn a rise of 9% over PCP, this was mainly on account of the rapid growth achieved in its “Technology One SaaS” platform. Also, the firm continued to maintain its stronghold in the government sector where it closed 11 major deals, and hence this segment contributed $80 Mn to the revenue. Further, the underlying PBT was clocked at $66.5 Mn up by 15% on PCP. This was on the back of strong geographical segment performance from APAC which exhibited a profit growth of 20%. It was due to the robust license fee growth, the revamp of the consulting business and the market leadership in the SaaS offering with ARR (annual recurring revenue) now at $38.1 Mn, up by 41% on PCP. Moving ahead, the company continues to see the robust growth in the Government sector with the growth of license fee at the rate of 17% Y-O-Y. The growth in the SaaS is expected to continue with the target of ARR reaching up to $62Mn in the upcoming 12 months period, which would be a rise of 62%. Also, the firm believes that the SaaS platform will be the single most significant platform for generating recurring profits for the company in the near future.

TNE’s SaaS Growth Trends (Source: Company Reports)

Meanwhile, the share price has risen 9.75% in the past three months as at November 19, 2018 and traded at higher PE level of 40.48x. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $5.630.

Class Limited

Decent Performance in Q1FY19: Class Limited (ASX: CL1) designs and develops application software. The Company offers cloud-based software solutions for accounting, administration, and reporting of investment portfolios. Class serves accountants, administrators, and advisors. Recently, the company posted decent performance in Q1FY19 quarter wherein the total accounts increased by 3,039 to 172,452. Of which, 166,102 belong to SMSFs Class Super account, and 6,350 belong to Class Portfolio account. Going forward, we expect that with the launch of the company’s “Do More” sales campaign & also with the introduction of stringent caps, limits, and event-based reporting, it is expected that the “Class Super” will gain traction & the company will be able to replicate its previous year’s December quarter exemplary sales performance. Based on decent performance in Q1FY19 and current trading level (i.e., scrip is trading at the lower end), we maintain our “Hold” recommendation on the stock at the current market price of $1.770.

Total Account Growth Trend (Source: Company Reports)

AU

AU

Please wait processing your request...

Please wait processing your request...