Telstra Corporation Ltd

.png)

TLS Details

Telstra and News Corp sign definitive agreements to combine Foxtel and FOX SPORTS Australia: Telstra Corporation Ltd (ASX: TLS) is known to be a good dividend payer of the past but the stock was impacted last year by multifarious factors; and despite the downfall, it still seems to be gearing up with many self-driven key efforts. The group for instance is taking many steps towards its target of delivering 1.5 billion in net productivity gains by fiscal 2022, and one such effort has been relating to cutting fixed costs by 7% in the first half of FY18. Lately, TLS and News Corp signed definitive agreements to combine Foxtel and FOX SPORTS Australia, and this is expected to deliver premium and innovative content to Australians with ever greater quality, variety and efficiency. Further, the combination of Foxtel and FOX SPORTS Australia along with their content assets would position TLS strongly to compete in the dynamic media market and is an important part of TLS' strategy. Moreover, TLS will be an exclusive telco sales agent for the combined entity on mobile and IP products and the company will continue with the broadcast reseller arrangements. The transaction is expected to close during the fourth quarter of FY18. TLS expects to record one-off accounting gain of A$263 million due to the fair value of the combined business compared with the book value. However, this is subject to changes arising from the timing of completion and finalisation of adjustments on completion. Additionally, for 2018, the income is now expected to be in the range of $27.6 to $29.5 billion and EBITDA of $10.1 to $10.6 billion. The company in 2018 expects to spend capex of $4.4 to $4.8 billion or approximately 18 per cent capex to sales. The free cash flow is expected to be in the range of $4.2 to $4.7 billion. TLS has reconfirmed the dividend guidance and the 2018 total dividend is expected to be 22 cents per share fully franked, including both the ordinary and the special components. Meanwhile, TLS stock has fallen 12.6% in three months as on March 29, 2018, but is trading at a low P/E. We give a “Buy” recommendation on the stock at the current price of $3.14

.png)

TLS Daily Chart (Source: Thomson Reuters)

Scentre Group

.png)

SCG Details

Development pipeline in excess of $3 billion: Scentre Group (ASX: SCG) has a strong base with revaluations with a potential for buyback and decent capital structure while some retail headwinds are hovering over REITs. Scentre in 2017, posted for 4.25% growth in the Funds from Operations (FFO) to $1.290 billion, which represents 24.29 cents per security. The distribution is of 21.73 cents per security, which is an increase of 2%. Excluding the impact of transactions, FFO growth is approximately 4.9%. The company’s net operating income grew due to the growth in the customer visitation with retailer demand. For 2018, SCG expects FFO growth of approximately 4.0% and the distribution for 2018 is expected to be 22.16 cents per security, which is an increase of 2%. On the other hand, Moody’s Investors Service has lowered the long-term rating from “A1” (review for possible downgrade) to “A2” (stable) to SCG, which will have no adverse impact on its cost of funds. Additionally, SCG has a development pipeline in excess of $3 billion, and is looking forward to open 106,000 square metres of new space in 2018. In addition, the group has recently announced NZ$790 million (SCG share: NZ$400 million) redevelopment of Westfield Newmarket, which will create a world class retail and lifestyle destination unparalleled in the New Zealand market. The group might also be able to normalize the existing divergence between FFO and DPS gradually. Meanwhile, SCG stock has fallen 8.6% in three months as on March 29, 2018 and is trading at a very low P/E. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $3.83

.png)

SCG Daily Chart (Source: Thomson Reuters)

Kidman Resources Ltd

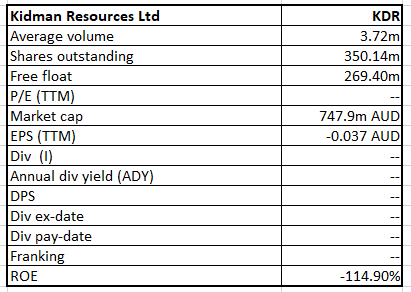

KDR Details

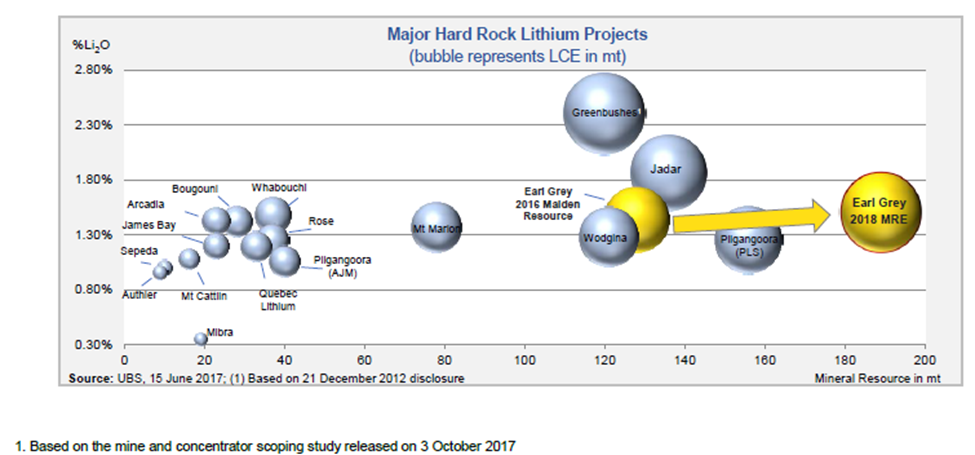

Significant Increase in Earl Grey Lithium Combined Mineral Resource Estimate: Kidman Resources Ltd.’s (ASX: KDR) stock has risen 9.6% in three months as on March 29, 2018 as the company posted a 54% increase in the combined Mineral Resource Estimate (MRE) for the Earl Grey Lithium Deposit. Earl Grey is estimated to contain 189 million tonnes of 1.50% Li2O or 7.03 million tonnes of Lithium Carbonate Equivalent, which is 91% of Resource classified as Measured or Indicated. Further, the result has confirmed Earl Grey’s position to be one of the world’s Tier-1 globally significant hard rock lithium deposits. Earl Grey is also expected to be in the first quartile of the global hard rock cost curve, as per the mine and concentrator scoping study.

Major Hard Rock Lithium Projects (Source: Company Reports)

Moreover, Western Australia Lithium joint venture (JV) with Sociedad Quimica y Minera de Chile (SQM) is rapidly advancing the project and the site selection for the proposed refinery will be announced in the next quarter. Additionally, there is high level of interest from various parties seeking lithium hydroxide off-take. The expanded Exploration Target is within KDR’s highly strategic Forrestania landholding, where multiple pegmatite targets are still to be tested, providing continued upside. Meanwhile, KDR has updated that market about the trading of issued options (KDRO) to shareholders that participated in May 2016 Rights Issue and the shareholders can exercise the options in all or portion, sell all or a portion or do nothing with expiry of options on April 30, 2018. While the volatility on lithium stocks is also continuing, KDR slipped by 3.3% on March 29, 2018; however, given the potential and quality assets, we put a “Buy” recommendation on the stock at the current price of $2.06

.png)

KDR Daily Chart (Source: Thomson Reuters)

Magellan Financial Group Ltd

.png)

MFG Details

Termination of three-year partnership with Cricket Australia: Magellan Financial Group Ltd (ASX: MFG) stock edged slightly lower on March 29, 2018 after the company announced the termination of its three-year partnership with Cricket Australia as the naming rights sponsor of the Australian Men’s Domestic Test Series. This came at the back of the integrity issues with regards to the conspiracy of the Australian Men’s Test Cricket team breaking the rules to get unfair advantage during a test series. On the other hand, in the first half of 2018, MFG completed the $1.57 billion initial public offering of the Magellan Global Trust, the largest closed end fund raising in Australian history. The company has recently announced two strategic acquisitions, Frontier Partners in the United States and Airlie Funds Management to strengthen its retail funds management business in Australia and add significant focus to its institutional distribution activities in North America. Despite some temporary headwinds, Magellan is a successful international equity and infrastructure fund manager with earnings growth backed by funds under management and performance fees; and is well positioned to cater to retail investor demand. MFG stock has fallen 11.6% in three months as on March 29, 2018; while the group’s total funds under management in February increased to $65,363 million from $58,882 million as at January 2018. As of now, we give a “Buy” recommendation on the stock at the current price of $23.84

.png)

MFG Daily Chart (Source: Thomson Reuters)

Woolworths Group Ltd

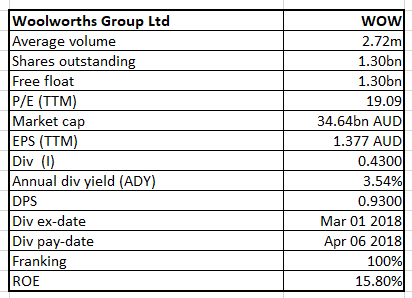

WOW Details

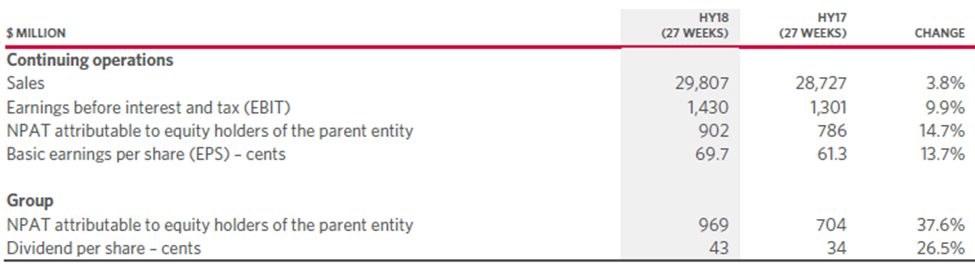

Expects a better second half 2018 result:Woolworths Group Ltd (ASX: WOW) is witnessing an increase in its market share (with continued greater sales momentum than Coles) and the group found support from the latest interim result. In 1H 2018, WOW reported 3.8% growth in the sales from continuing operations to $29,807 million. The growth of 4.9% and 4.8%, respectively, in Australian Food and Endeavour Drinks led to the overall growth. Further, all businesses have reported positive sales growth during the half of 2018. NPAT attributable to equity holders of the parent entity from continuing operations rose 14.7% on the prior year to $902 million, with corresponding EPS up 13.7% to 69.7 cents. Additionally, WOW expects a better second half result than the prior year with the BIG W FY18 loss before interest and tax currently expected to be in the range of $80 - $120 million.

1H 18 Financial Performance (Source: Company Reports)

Further, WOW is completing the rollout of 1Store and other technology upgrade programs for process and efficiency improvement in FY19 and beyond. The company continues its first half improvements in BIG W and improving stock flow disciplines. In addition, WOW is accelerating investment in digital and data to better meet customers’ needs. While costs due to enhanced competition may give rise to some hiccups; investments in digital, offer and service are capable of yielding better outcomes. WOW stock has fallen 3.7% in three months as on March 29, 2018, and with the price scenario, we have a “Buy” recommendation on the stock at the current price of $26.29

.png)

WOW Daily Chart (Source: Thomson Reuters)

Resolute Mining Limited

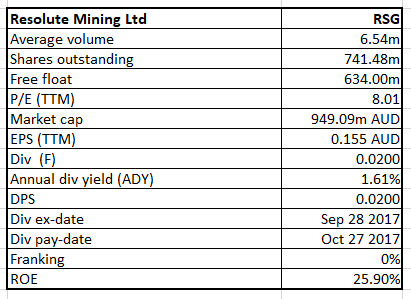

RSG Details

Expects to improve production and unit costs in the second half of 2018: Resolute Mining Limited (ASX: RSG) seems to be a good bet considering the market volatility at the back of geopolitical scenario, and its decent fundamentals that can drive future growth. For 1H 2018, RSG delivered 20% growth in the revenue, while posted the net profit after tax of A$38 million. During 1H 2018, gold production of 142,748 ounces (oz) was achieved at an All-In Sustaining Cost of A$1,395/oz (US$1,092/oz). Additionally, for FY 18, the gold production and cost guidance have been maintained at 300,000oz at an All-In Sustaining Cost of A$1,280/oz (US$960/oz). The company expects to improve production and unit costs in the second half of 2018 as the company will process higher grades at both Syama and Ravenswood. Further, Syama Underground mine development is on schedule and on budget for completion of the sublevel cave in December 2018. As a result, RSG stock has risen 9.2% in three months as on March 29, 2018 and is still trading at a low P/E. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $1.245

.png)

RSG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...