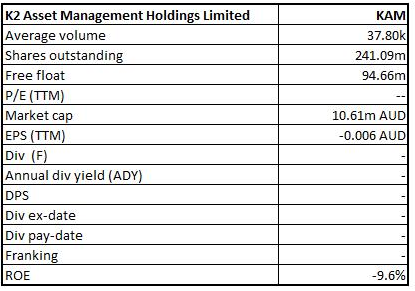

K2 Asset Management Holdings Limited

KAM Details

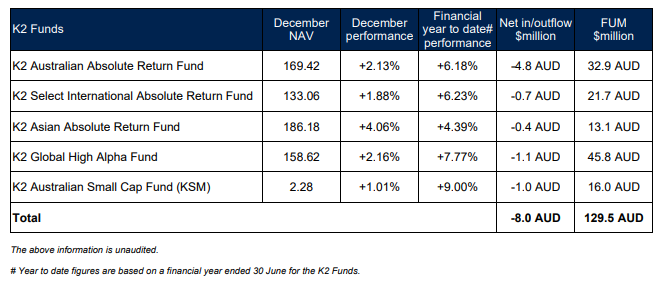

Performance Outcome from Market Volatility:K2 Asset Management Holdings Ltd (ASX: KAM) is the holding company of K2 Asset Management Ltd, KII Pty Ltd and Trusuper Pty Ltd. The market capitalisation of the company stood at A$10.61 Mn as on 7th January 2020. During FY19, the company posted total revenue amounting to $4.8 million, out of which $4.4 million was management fees. As per the key personnel of the company, the volatility in the market during FY19 has offered a mixed bag of performance outcomes broadly and for the K2 Funds. The following picture provides an idea of monthly FUM and fund performance of the funds which are managed by K2 Asset Management Ltd as at 1st January 2020:

Monthly Performance (Source: Company Reports)

Well Positioned for Future Growth:The company stated that the new financial year would require vigilance and those, which can survive the late stage of this passive cycle would be well-positioned for the future. There is far less competition within the active space because of the large number of closures and losses of key mandates and the company would be helped by this moving forward.

Stock Recommendation:Current ratio of the company stood at 10.11x in FY19 as compared to the industry median of 1.45x. This reflects that the company is in a decent position to address its short-term obligations as compared to the broader industry. On the valuation front, the stock of KAM is trading at a price to book multiple of 0.8x as compared to the industry average (Financials) of 3.4x on TTM basis. It has EV to sales multiple of 2.2x against the industry average (Financials) of 10.4x on TTM basis. Therefore, considering the valuations, decent liquidity position, growth in FUM, etc., we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.044 per share on 7th January 2020.

KAM Daily Technical Chart (Source: Thomson Reuters)

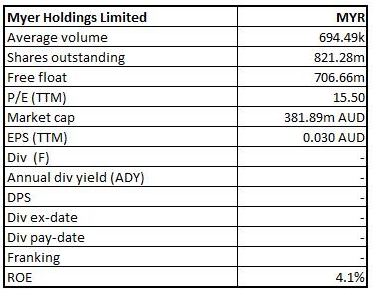

Myer Holdings Limited

MYR Details

Rise in Digital Sales of 21.9%:Myer Holdings Limited (ASX: MYR) is in the operation of the portfolio of 66 department stores throughout Australia and has a market capitalization of A$381.89 Mn as on 7th January 2020. The company recently announced that Jonathan Garland has resigned from the role of General Counsel and Company Secretary, and the last day was 18th December 2019.Total digital sales of the company stood at $292 million, reflecting a rise of 21.9%, which include Marcs and David Lawrence and sass & bide online sales, Myer Market and $29.8 million via in-store iPads. Digital business of the company represents 9.8% of total sales.

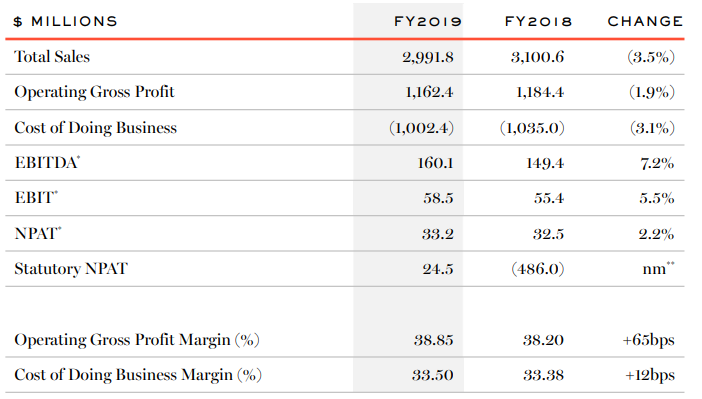

Total Sales (Source: Company Reports)

Anticipation of Challenging Macro Environment:The company expects the challenging macro environment as well as subdued consumer sentiment to continue during FY2020. It has identified several opportunities for improving productivity as well as to continue to decrease costs, via cost savings and efficiencies, throughout its supply chain and other non-customer facing activities.

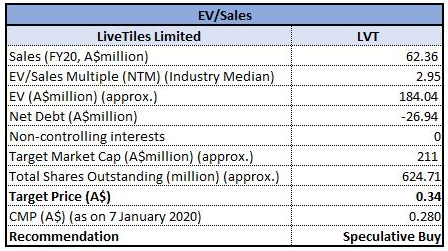

Valuation Methodology:P/E Multiple Approach

P/E Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:Even though the company has made progress with respect to executing Customer First Plan, it stated that there is much more which is yet to be done and it would continue to deliver against the Plan in best interests of customers as well as shareholders. Net margin of the company stood at 1.0% in FY19, reflecting YoY growth of 19.9%. This reflects that the company has improved its position to convert its topline into the bottom line. Debt to equity of the company stood at 0.14x in FY19 as compared to the industry median of 0.67x. We have valued the stock using P/E based valuation approach, and for the said purposes, we have considered peers like, Metcash Ltd (ASX: MTS) and Super Retail Group Ltd (ASX: SUL) and Adairs Ltd (ASX: ADH). Therefore, we have arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering the decent position of the key margins, lower Debt/Equity ratio and growth in digital sales, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.470 per share, up by 1.075% on January 7, 2020.

MYR Daily Technical Chart (Source: Thomson Reuters)

LiveTiles Limited

LVT Details

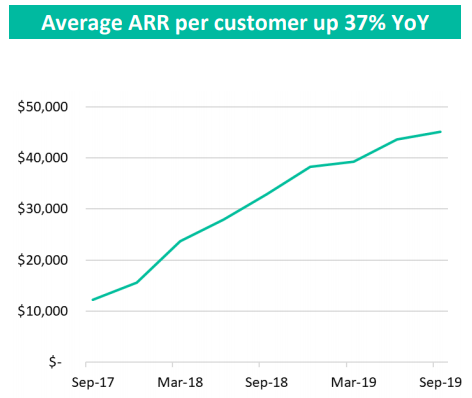

Growth in Average ARR:LiveTiles Limited (ASX: LVT) is involved in the development and sale of business software in Australia and overseas. The market capitalisation of the company stood at A$240.92 Mn as on 7th January 2020. Recently, the company, through a release dated 3rd December 2019, announced that it has wrapped up the acquisition of CYCL, which happens to be a leading intelligent intranet software business in Europe. As per the release, LVT has issued 42,605,922 shares as part of the upfront consideration for the acquisition. During Q1 FY20, the company reported strong growth in average ARR per customer of 37% on YoY basis, which was resulted by (1) A higher proportion of new enterprise customers, (2) Product cross-sell / bundling, and (3) Increased penetration of existing customers.

Average ARR per Customer (Source: Company Reports)

Expectation of Strong Revenue and Customer Growth: For FY20, the company anticipates delivering another year of the strong customer as well as revenue growth, which would be fueled by its continued investment into its products, partners and sales and marketing channels.The key financial objective of the company is to deliver ARR of minimum $100 million by 30th June 2021.

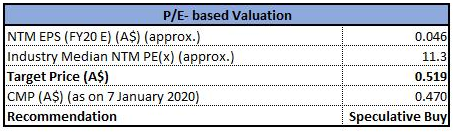

Valuation Methodology:EV/ Sales Multiple Approach

EV/ Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company has recorded strong growth in customer cash receipts in Q1 FY20 and the figure stood at $8.5 million. We have valued the stock using EV/Sales multiple approach, and for the said purposes, we have considered peers like Citadel Group Ltd (ASX: CGL) Catapult Group International Ltd (ASX: CAT), rhipe Ltd (ASX: RHP) and Class Ltd (ASX: CL1). Therefore, we have arrived at a target price, which is offering an upside of lower double -digit (in percentage terms). Therefore, considering the company’s outlook, decent performance in Q1 FY20, and expected upside, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.280 per share as on 07 January 2020.

LVT Daily Technical Chart (Source: Thomson Reuters)

LiveHire Limited

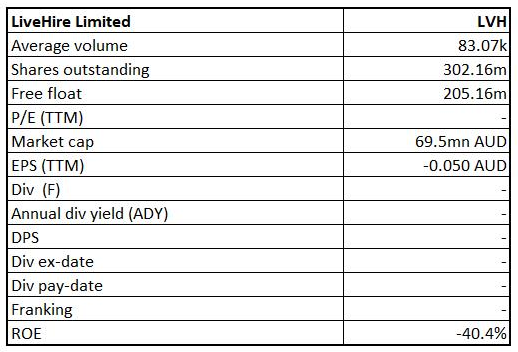

LVH Details

LiveHire Enters Australian MSP Market with Chandler Macleod: LiveHire Limited (ASX: LVH) provides cloud-based human resources software and platform services. As on 7th January 2020, the market capitalisation of the company stood at $69.5 million. The company has recently announced that it has entered an enterprise wide agreementwith Chandler Macleod. It will use the LiveHire platform to provide a Managed Service Program for a large ASX listed company’s contingent workforce. As per the release, the enterprise agreement would be having an initial term of 12 months from December 18, 2019 and would automictically renew for additional 12-month periods unless either party gives written notice about the non-renewal minimum 60 days before the end of then-current term.

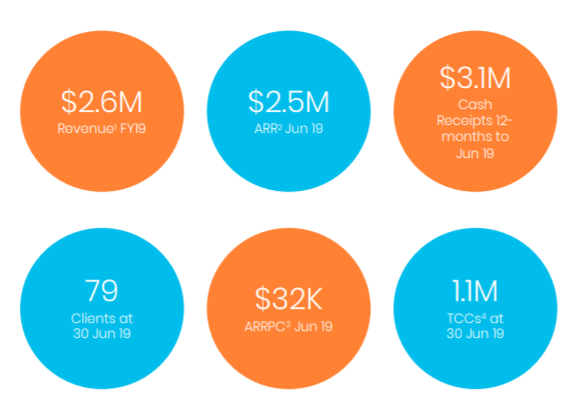

Extension of Loan Back Shares: LiveHire Limited agreed to extend the loan period associated with the issue price of 22,545,131 ordinary shares for a further four years until 22 December 2023. In the recently held AGM, the Board stated that the company maintains a robust capital position with no debt and a cash balance of $34 million. During FY19, the company signed 41 new clients through its Direct Sales and Partner channels and witnessed an increase of 88% in Annualised recurring revenue to over $2.5 million.

Key Numbers (Source: Company Reports)

What to Expect from LVH: The company had a sound start to FY20. Based on the traction with the existing partners as well as recent partnership wins, sustained success of the Direct Sales team along with the pipeline of opportunities, the company expects that its revenue momentum might continue across the financial year. It continued to expand its direct sales and channel partner pipelines.

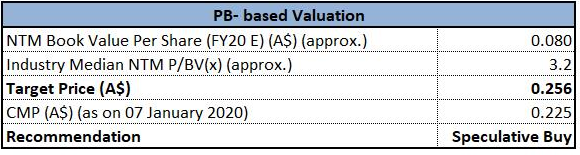

Valuation Methodology: Price/Book Valuation Approach

Price/Book Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of LVH gave a return of 2.22% in the last one month and is trading very close to its 52-week low level of $0.210, proffering a decent opportunity for accumulation. In the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 127.31% in revenue and saw an improvement in EBITDA margin and net margin in the same time span. Considering the returns, trading levels, CAGR in revenue and improving margins, we valued the company using Price/Book Value valuation approach, and for the said purposes we have considered peers like Xero Ltd (ASX: XRO) and LiveTiles Limited (ASX: LVT), and have arrived at a target upside which is offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.225, down by 2.174% on January 07, 2020.

LVH Daily Technical Chart (Source: Thomson Reuters)

Bionomics Limited

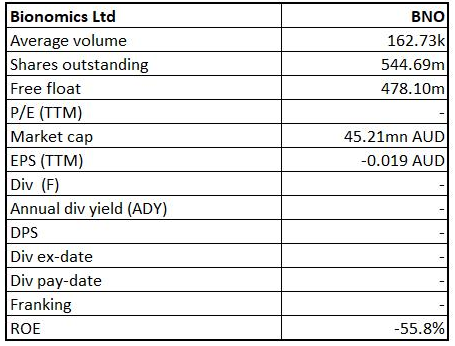

BNO Details

Sale of French Subsidiaries to Domain Therapeutics: Bionomics Limited (ASX: BNO) is a developer of innovative treatments for cancer and diseases of the central nervous system. The company has recently announced that it has accepted an offer from Domain Therapeutics for Neurofit SAS and PC SAS. It was added that sale price amounting to €1,810,028.97 is the amount of intercompany debt that is owed by Bionomics to subsidiaries for scientific research conducted by them on Bionomics drug candidates. Notably, the debt would be assumed by Domain upon acquisition. The parties anticipate completion of the transaction on or about January 31, 2020, subject to the satisfaction of conditions precedent.BNO also announced that it has received a R&D Tax Incentive Refund of A$5,183,291.69 for FY2018/19.

The company has recently released its quarterly report wherein it stated that cash balance as at 30 September 2019 stood at $9.36 million with net operating cash outflow of $2.56 million. It also mentioned that research & development costs went down by 49% as compared to the previous quarter.

Net Cash Used in Operating Activities (Source: Company Reports)

Growth Opportunities: The company anticipates to further develop the prototype tablet formulation to optimize the formulation for a Phase 2b clinical trial and expects to manufacture BNC210 drug substance and tablets on a large scale for the supply of Phase 2b drug. It is pursuing its licensing and partnering possibilities for its CNS pain and cognition programs and is planning to retire some or all of its debt during FY 2020.

Stock Recommendation: As per ASX, the stock of BNO gave a return of 2.47% on YTD basis and is inclined towards its 52-week low level of $0.031. In the span of 4 years from FY15 to FY19, the company witnessed an improvement in EBITDA margin. On TTM basis, its EV/Sales ratio stood at 3.2x and the industry median (Healthcare) is 9.2x, while its P/B multiple is 2.6x while the industry average (Healthcare) is 3.6x. Considering decent returns, improvement in EBITDA margin and lower valuations, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.085 per share, up by 2.41% on January 07, 2020.

BNO Daily Technical Chart (Source: Thomson Reuters)

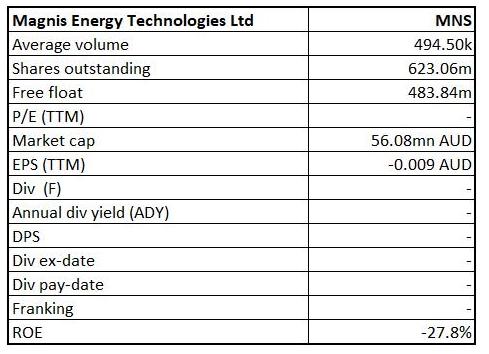

Magnis Energy Technologies Ltd

MNS Details

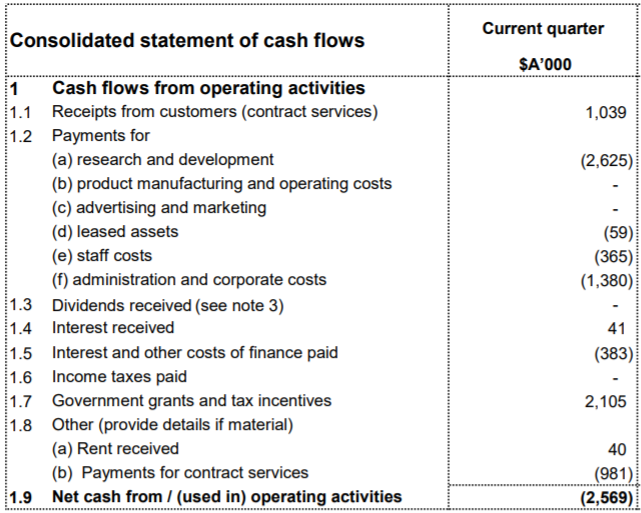

Nachu Graphite Binding EPC Contract Executed: Magnis Energy Technologies Ltd (ASX: MNS) has a multi strategy business of lithium-ion battery technology manufacturing in the USA and Australia combined with pre-mine development of its Nachu Graphite project in Tanzania. The company has recently announced that it has executed a binding engineering, procurement and construction contract with Metallurgical Corporation of China to provide a turn-key solution for a 240,000 tpa graphite production facility at the Nachu Project. The company has started funding applications and negotiations with China Export Credit Agency, and concurrently, Magnis and MCC have been continuing further negotiations with regards to closure of residual project funding amounts, with an objective of minimising equity portion needed. On 30 September 2019, the company has announced that, as part of due diligence for iM3 New York battery plant funding, independent valuation wrapped up by O’Brien & Gere valued equipment at US$71.34 Million (A$105.5 Million) with the company’s direct and indirect ownership at 50.86% of the project.

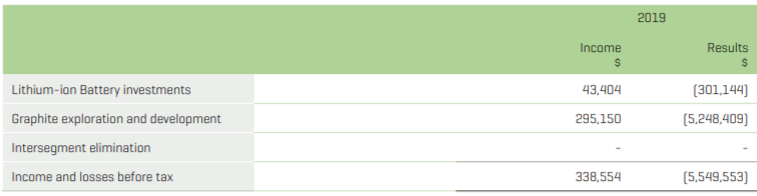

The company also announced that National Australian Bank had been engaged as an advisor to Imperium3 Townsville, bringing experience in advising financing large projects in the renewables sector, which includes working alongside with government bodies, to advise projects in North Queensland.During FY19, the group incurred an operating loss after tax of $5,549,553.

Financial Performance (Source: Company Reports)

Growth Strategies: The company’s growth strategy revolves around leveraging off a graphite asset in Tanzania, associated production IP, as well as a strategic partnership with US based Charge CCCV LLC. The strategy encompasses producing 99.95% graphite purity for LIB (Lithium-ion Battery) with strong green credentials and by maintaining a competitive advantage through unique IP.

Stock Recommendation: In the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 8.29% in revenue and saw a substantial improvement in EBITDA margin in the same time span. As per ASX, the stock is trading close to its 52-week low level of $0.074, offering a good opportunity for accumulation. Considering the CAGR in revenue, improvement in EBITDA margin, trading levels and decent outlook, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.100, up by 11.111% on January 7, 2020.

MNS Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...