Fortescue Metals Group Limited

.png)

FMG Details

Decent Q2 FY19 Performance:Fortescue Metals Group Limited (ASX: FMG) is an iron ore company based in Perth, Australia. The share price of the company increased by 4.244% on 31 January 2019 owing to the release of December 2018 quarterly updates which stated that themaiden cargo of West Pilbara Fines was shipped in December, and partnership with CSIRO for the development and commercialization of hydrogen technology. In FY19, it expects a capex of US$1.2 billion, shipment of 165-173mt, and an average strip ratio of 1.5x.

.png)

Production Summary (Source: Company Reports)

During FY18, it reported a free cash flow of A$700 million witha favourable debt/equity ratio of 0.41x and Net debt/EBITDA of 0.92x. It reported a higher dividend yield of 4.24% as compared to the metal and mining industry median of 2.9% representingmore income for its shareholders.

Over the last three months, FMG has generated a positive return of 33.50% and is trading at the higher level. With the beginning of shipment of West Pilbara Fines ores, a partnership with CSIRO, favourable capital structure, better FY19 outlook and higher than industry dividend yield, we have a ‘buy’ recommendation on the stock at the current market price of $5.650.

FMG Daily Chart (Source: Thomson Reuters)

Commonwealth Bank of Australia

.png)

CBA Details

Bullish indication with decent FY19 earnings guidance:Commonwealth Bank of Australia (ASX: CBA) is a multinational bank based out in Sydney, Australia. The bank will be declaring its interim result for the period ending 31 December 2018 on 6 February 2019 at 11:00 am AEDT in which it expects non-cash loss of $169 million to be included in the statutory NPAT in its interim result.

.png)

FY19 Interim Highlights (Source: Company Reports)

During FY18, the bank reported a higher than industry Net interest margin of 2.15% as compared to the industry median of 1.94%. The Tier 1 risk-adjusted capital ratio has improved over the past five financial years and is currently calculated at 12.3% which is above the industry median of 11.13% showing thatthe bank's financial health is improving.

Over the past three months, the scrip has generated a positive return of 4.52% and is currently trading at $69.910. The Relative Strength Index (RSI) along with the Bollinger band is visible in positive territory.With the better-expected earnings guidance for FY19, decent financials and bullish indication through charts, we put a ‘Buy” recommendation on the stock at the current price of $69.910 (down 1.867% on 31 January 2019).

CBA Daily Chart (Source: Thomson Reuters)

Boral Limited

.png)

BLD Details

Better FY19 outlook:Boral Limited (ASX: BLD) is an Australia-based material company engaged in manufacturing and supplying building and construction materials. For FY19, the company expects a high single-digit EBITDA growth excluding Property in both years for Boral Australia, profit growth of 10% for USG Boral, and EBITDA growth of ~20% for Boral North America.

.png)

FY18 Financial Highlights (Source: Company Reports)

Over the past five years,the margins of the company have improved. During FY18, the company reported EBITDA and Net margin of 15.6% and 6.9% respectively as compared to FY14 margins of 10.0% and 2.5% respectively.It reported a higher dividend yield (TTM) of 6.0% as compared to the basic material industry median of 3.6% representingmore income for its shareholders.

Over the past three months, the stock has generated a negative yield of 11.23% and is trading close to the lower level. The RSI along with the Bollinger band is visible in neutral territory. By looking at its improving margins along with a better outlook for FY19, we, therefore, maintain our ‘Buy’ recommendation on the stock at the current market price of $4.950 (up by 1.02% today).

BLD Daily Chart (Source: Thomson Reuters)

QBE Insurance Group Limited

.png)

QBE Details

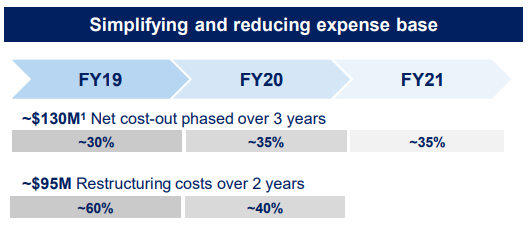

Decent Outlook:QBE Insurance Group Limited (ASX: QBE) is an Australia-based insurance company. The company is expected to release its FY18 results on 25 February 2019 and will also declare the information related to the dividend. It has also announced a 3-year operational efficiency program with the target of net cost saving of $130 million and an expense ratio of ~14% in 2021.

Cost reduction over the upcoming years (Source: Company Reports)

During FY17, the company reported a lower than industry expense ratio of 17.3% as compared to the industry median of 34.3% indicating that the company charges less fee to manage the funds. The combined ratio has also improved over the past 5 years and is reported at 88.2% in FY17. Moreover, it reported afavourable capital structure in 1HFY18 with a debt/equity ratio of 0.37x with earning retention ratio of 0.41x.

Over the past six months, the stock has generated a positive yield of 5.53%. The RSI along with the Bollinger band is visible in neutral territory. With the upcoming FY18 results, favourable capital structure, improving combined ratio and lower than industry expense ratio, we maintain our ‘Buy’ recommendation on the stock at the current market price of $10.730 (up by 0.468% today).

QBE Daily Chart (Source: Thomson Reuters)

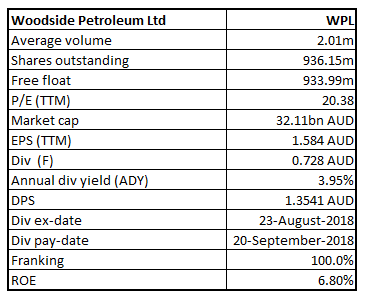

Woodside Petroleum Limited

WPL Details

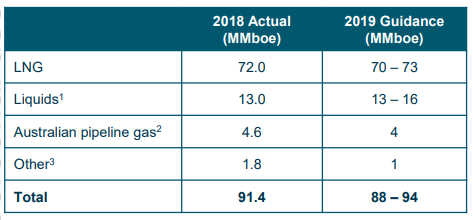

Wheatstone LNG gas plant to start operating in 1Q19:Woodside Petroleum Limited (ASX: WPL) is an Australia-based oil and gas explorer. The company expects the first domestic gas production from Wheatstone LNG gas plant in 1Q19. As per its 2019 production guidance, it is expected to produce 88-94 MMboe gas and has planned major turnarounds for Pluto LNG, Goodwyn Project, and integrated NWS Project.

FY19 gas production guidance (Source: Company Reports)

Over the past few years, the margins of the company have improved and are reported above the industry median.It reported an EBITDA and Net margin of 71.4% and 24.8% respectively in 1H18 as compared to the industry median of 33.9% and 10.4% respectively. The company reported a higher than the industry dividend yield of 5.5% as compared to the industry median of 4.6% showing that the company is generating more income for its shareholders.

During the last month, the stock hasgenerated a positive return of 9.51%. With the better FY19 production guidance, improving margins and higher dividend yield, we maintain our ‘buy’ recommendation at $34.320 (up by 0.058% today).

WPL Daily Chart (Source: Thomson Reuters)

Carsales.com Limited

.png)

CAR Details

Higher than industry margins:Carsales.com Limited (ASX: CAR) is an Australia-based online marketplace which provides classifieds business for motorcycle, automotive, and marine. Integration of core carsales IP and technology is expected to drive revenue in Chile, Mexico, and Argentina in FY19. International look through revenue and EBITDA grew 54% and 76% respectively in FY19.

.png)

Look through summary (Source: Company Reports)

During FY18, the margins of the company were reported above the industry median.It reported an EBITDA and Net margin of 46.1% and 42.4% respectively in FY18 as compared to the industry median of 42.6% and 31.4% respectively. Similarly, the return to its shareholders have improved and is better than its peers as its ROE of 61.5% was above the industry median of 31.1% in FY18.

During the last one month, the stock hasgenerated a positive return of 13.0%. With the Integration of core carsales IP and technology, better FY19 look through revenue and EBITDA, and higher than industry margins, we maintain our ‘buy’ recommendation at $12.610 (up by 1.448% today).

CAR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...