6 Key Stocks in the Resource Sector – AWC, IGO, BHP, STO, S32, ILU

Stocks’ Details

Alumina Limited (ASX: AWC)

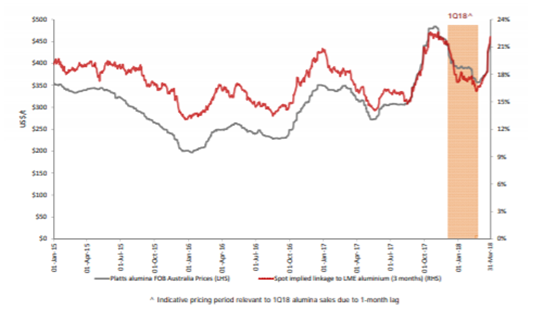

First Quarter Earning Update:The share price of AWC was up by 11.20 per cent in the past one month and rocketed by 7.1 per cent on 19 April 2018 with the rising commodity prices. Meanwhile, Alcoa Corp released quarterly earnings report for the first quarter of 2018 wherein the alumina segment performance was down as compared to the previous period and this was due to lower index pricing and higher cost but still generated significant positive cash flow. Since the end of the 1Q 2018 pricing period, alumina prices have surged, and the joint venture is well placed to take advantage of this increase. The Platts FOB Australia alumina prices as on 18 April 2018 were US$710 per tonne. In 1Q 2018, AWAC’s production of alumina was 3.0 million tonnes and bauxite production from wholly owned mines plus the equity shares in MRN and CBG was 10.6 million bone dry tonnes. During 1Q 2018, the gross distributions received by Alumina Limited from AWAC entities were US$266.2 million and US$52.8 million and these were reinvested as equity contributions. The net cash receipts from AWAC entities for 1Q 2018 were US$213.4 million, of which US$198 million were included in Alumina Limited’s 2017 final dividend. The Group expects to receive distributions of approximately US$56 million from AWAC entities during April 2018. Alumina Limited’s net debt was approximately US$114 million at the end of March 2018. Given the uptrend, we recommend to “Hold” the stock at the current market price of $ 2.870.

Spot alumina & Implied linkage trend (Source: Company Reports)

Independence Group NL (ASX: IGO)

Prospectus tie-up with Arrow Minerals: Up 7.7% on April 19, 2018 at the back of nickel prices soaring high given possible further sanctions against Russian companies, IGO seems to be gaining traction. Meanwhile, Independence Group has become a major shareholder for Arrow Minerals. The investment by IGO, along with the broker equity raising, has raised over $5 million which has allowed Arrow to commit to significant drilling programmes at both the Strickland Gold and Malinda Lithium Projects. Moreover, the Pilbara Gold Project sale and the joint venture will add up to $1 million over the next 12 months. Arrow is in its ever-financial position, with around 2 cents per share of cash and investments. Arrow is currently undertaking a major aircore drilling programme at the Strickland Gold Project, which will cover T8, T6, T2 and T1 prospectus. Independence Groupholds 34,482,759 securities and 11.24 per cent of the voting power in Arrow Minerals Limited. The share prices are trading at a higher level and have been up by 46 per cent in the past one year at the back of surging commodity prices and various developments by the group. We recommend to “Hold” the stock at the current market price of $ 5.600.

BHP Billiton Limited (ASX: BHP)

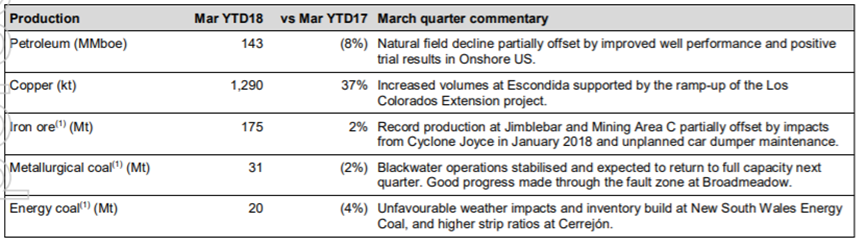

On track to achieve volume growth:BHP released its operational review for the nine-months’ period ending on 31 March 2018 and disclosed that the full year production will remain unchanged for Petroleum, Metallurgical Coal and Energy Coal. It remains on track to achieve six per cent volume growth for FY2018. It is anticipated that Group’s copper equivalent production will increase by 6 per cent in 2018 and it has increased its footprint for Petroleum in the northern extension of the Wilding prospect in the US Gulf of Mexicothrough the acquisition of 33.33 per cent of interest in Samurai prospect and all the projects that are under development are on track. The group reported for iron ore production rising by 2 per cent but slightly reduced its iron ore production guidance for fiscal 2018 to 272-274 million tonnes (down from 275-280 million tonnes), at the back of some system related challenges. The group also narrowed its total copper production guidance to between 1,700 and 1,785 k. BHP is moving on track with regards to its US shale assets’ sale. Recently, Adelaide Brighton Limited (ASX: ABC) signed a contract with BHP Billiton Limited for the continuation of the supply of cement and lime to BHP’s Olympic Dam mine. ABC is a leading construction material and lime producing group of companies which supplies the Australian infrastructure, building and resource industries. The new contract maintains and extends the long-term relationship between BHP Billiton (Olympic Dam Corporation) Pty Ltd and Adelaide Brighton Cement Ltd, on terms generally like those applicable between the parties for many years. It is expected that this relationship will continue for several years.

Production Performance (Source: Company Reports)

The stock price has jumped up by 10.67 per cent in the past six months and was up by nearly 2.8 per cent as on 19 April 2018. We recommend to “Hold” the stock at the current market price of $ 30.920.

Santos Limited (ASX: STO)

Strong cash flow generation:STO released its report on Activities for first quarter of FY18 and disclosed that it is reaping the benefits of its new low cost, high efficiency operating model. The Group generated $246 million of free cash flow and reduced the net debt (to $2.5 billion) by 8 per cent as compared to previous quarter. The Group announced that it has received an unsolicited, non-binding and indicative proposal from Harbour Energy to acquire 100 per cent of Santos shares by way of scheme of arrangement. In PNG, Santos along with the other PNG LNG parties has commenced discussions with both the PRL 3 (P’nyang) and PRL 15 (Papua LNG) joint ventures to build alignment for the proposed construction of three additional LNG trains at the PNG LNG site. The Group has maintained its 2018 forecast free cash flow breakeven at ~US$36/bbl, despite the significant increase in drilling activity in Queensland and the Cooper Basin, and the temporary shutdown in PNG following a major earthquake activity. The stock prices have been climbing up since past one year and we recommend to “Hold” the stock at the current market price of $ 6.000.

Comparative Performance (Source: Company Reports)

South32 Limited (ASX: S32)

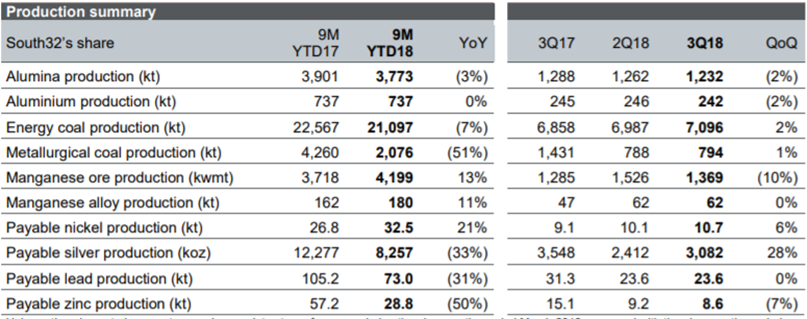

Production Record at Australia Manganese:South32 released its Quarterly Report for March 2018, wherein net cash increased by US$477M to US$1.9B1 during the March 2018 quarter as commodity prices remained elevated and it received net distributions amounting to US$158M from its manganese equity accounted investments (EAI) (South32 share) and US$44M (pre-tax) from the sale of a financial asset. The Group’s strong financial position allowed it to return a further US$85M to its shareholders during the period. It advanced its plans to manage South Africa Energy Coal as a stand-alone business from the June 2018 quarter, which will allow it to simplify the business, lower overhead costs and fundamentally change the way it works. It upgraded the production guidance at Australia Manganese by 6% and by 5% for South Africa Manganese on the back of strong market demand and record operating performance at Australia Manganese. It increased the payable silver production at Cannington by 28% in the quarter as mining entered a higher-grade sequence of stopes. It finalised its plans at Illawarra Metallurgical Coal that are expected to deliver more productive longwall and development performance, underpinning a recovery in production to more than 6Mt in FY19 and an anticipated return to historical rates above 8Mtpa from H2 FY20. The share price surged up by 8.8 per cent in the past one month and jumped up by nearly 4.6 per cent on 19 April 2018 with support from commodity prices along with decent update. We recommend to “Hold” the stock at the current market price of $ 3.880.

Production Summary (Source: Company Reports)

Iluka Resources Limited (ASX: ILU)

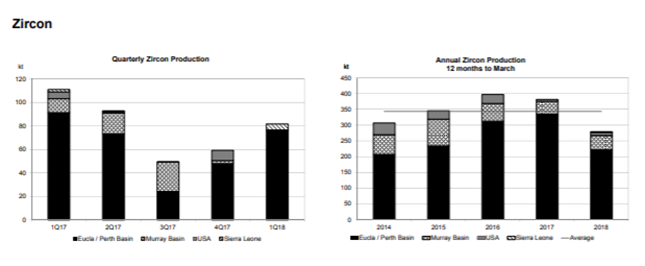

Strong market conditions:The Group recently announced its Quarterly Report for March 2018 and disclosed that Zircon/Rutile/Synthetic Rutile(Z/R/SR) production for the March quarter was 182 thousand tonnes, 8% higher than the December 2017 quarter. Zircon production was higher, largely due to a full quarter of processing at Narngulu mineral separation plant (MSP). The market dynamics remained unchanged, including tight supply in the zircon market and strong demand from pigment producers for high-grade titanium feedstocks continued. Iluka has experienced a solid quarter of sales and has seen steady appreciation in prices. Weighted average prices for Z/R/SR increased in the quarter from the end of 2017. This reflects the achievement of previously announced price increases for rutile and contractual outcomes. Iluka plans to double the capacity of both the Gangama and Lanti dry operations from 500-600 tonne per hour to 1,000-1,200 tonnes per hour. The Net debt further reduced to $108 million, down from $183 million as on 31 December 2017. The stock price advanced by 7.3 per cent in the past five days and we recommend to “Hold” the stock at the current market price of $ 11.680.

Production Summary for Zircon (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...