.png)

Stocks’ Details

Xero Limited (ASX: XRO)

Expected improvement: Xero is an easy-to-use global online platform for small businesses and their advisors, with over one million subscribers in more than 180 countries. Xero seamlessly integrates with more than 600 apps. It lately announced the appointment of UK-based entrepreneur Dale Murray as a non-executive director on its Board of Directors. The Group has also issued 30,000 ordinary shares upon exercise of vested options granted under the NZ Plan. The Exercise price for the options was NZ$17.51 per option. The group is gaining a lot of traction and is said to be transiting from a loss-making company into a profitable one by many market experts. We also believe in the group’s potential given its proven business model and sizeable structural growth opportunities. The regulatory changes in the United Kingdom in the coming period will also help the stock. Particularly, ‘Making Tax Digital’ initiative in the UK with adoption of cloud accounting software by SMEs before April 2019, are expected to provide boost to XRO.

.png)

Trend of subscribers and market leadership (Source: Company Reports)

Xero’s global footprint is expanding as it executes its strategy to rewire the global small business economy, connecting millions of businesses to their banks, advisors and each other. It launched a wave of significant new products at Xerocon and targets investment towards strengthening the platform and leveraging the machine learning and artificial intelligence. As Xero continues to grow, enhanced access to deeper capital markets, increased trading liquidity and a broader base of potential investors is critical to fulfilling the company’s aspirations. We recommend to “Hold” the stock at the current market price of $39.02, post a run-up of 100% in a year.

Myob Group Limited (ASX: MYO)

Improved online subscriber growth: MYO continues to deliver strong growth and solid returns year on year to its shareholders, and 2017 financial year was no exception. The group expects to touch 1 million online subscribers’ count by 2020 (73% 1Q18 net adds growth witnessed on year in year basis). MYOB reported double-digit growth across all key financial measures, driven by record growth in online subscribers. Revenue ($416 million) and NPATA ($102 million) for FY17 were up by 12 per cent and by 10 per cent respectively as compared to prior year. Underlying earnings (EBITDA) were $190 million in FY17, an increase of 11 per cent on prior year. The Group delivered a record growth in online subscribers of 60 per cent, reaching 399,000 online subscribers in December 2017. Customer Lifetime value continues to increase, through the growth in subscriber base, sustained ARPU increases and through achieving record retention rates. The success of the MYOB rebrand in 2017 has played an important role in increasing the funnel of new SME wins and lifting its profile and brand across the next generation of SMEs. The percentage of new clients taking an online subscription has also hit an all-time high at 94 per cent.

.png)

Financial Performance (Source: Company Reports)

On the back of strong financial results, and a healthy balance sheet, the Board was pleased to declare a final dividend for FY17 of 5.75c per share for the year, bringing the full year dividend to 11.5 cents per share. This represents a dividend pay-out ratio of 68.6 per cent of the full year 2017 Statutory NPATA. In FY18, it expects that the Connected Practice vision, together with the development of the MYOB Platform, will continue to accelerate its online subscriber growth. If the Reckon acquisition proceeds, it expects revenue growth to be in the 14% to 16% range, generating a higher revenue with the inclusion of revenue from the RAG clients, although this does depend on when the acquisition is approved. The Group recently bought back 170,000 shares and till now it has bought back 22,823,018 shares. The share price has been falling since the start of the year that is by 9.9 per cent, followed by a rise of 7.6 per cent in the past one month. We present a “Hold” recommendation at the current market price of $3.25.

Nearmap Limited (ASX: NEA)

Record Portfolio Growth: This aerial imagery company reported an increase of 27 per cent and of 80 per cent in Group Revenue Growth and Group Gross Margin for H1FY18 respectively, as compared to the same period in the prior year. It captured Australia’s population up to 6 times per year and 67% of the US’s population up to 3 times per year. The Group has expanded its footprint and is now photographing over 500,000 square kilometers annually, a 90% increase over its FY2017 capture program. It has a diverse customer base in both AU and US with National enterprise customers in both territories, as well as partners. In New Zealand, it captured 14 cities and 72 per cent of the population. In 2018, it will focus on opening source developer community and will export 3D content.

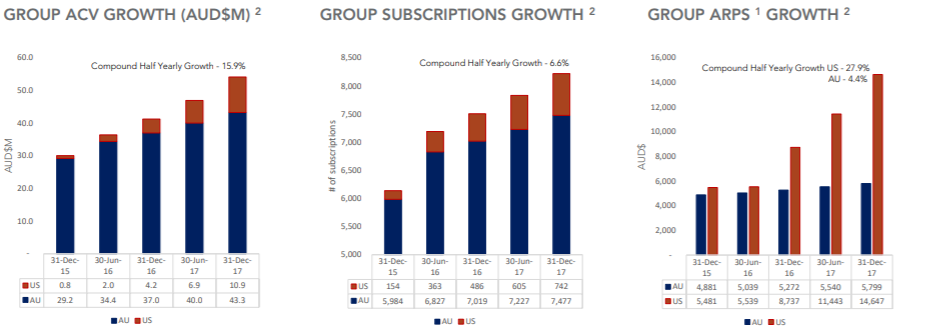

ACV, Subscriptions and ARPS Growth (Source: Company Reports)

It is unlocking new opportunities with multi-dimensional content and is working on making 3D content available for everyone. It reaffirmed H2 Guidance and Australia and US incremental ACV (annualised contract value) and STCR were consistent with H1FY18. US ACV was more than USD$10 million on 31 March 2018. Nearmap posted record growth in February with US ACV rising to US$8.5 million from US$5.3 million at the end of June 2017 and Australian ACV rising to $43.3 million from $40 million. It is expected that lower Australian dollar against the greenback will benefit the profits given the strong growth in its US operations. The stock price climbed up by 47 per cent in the past six months, followed by a drop of 6.7 per cent in the past five days. We give a “Hold” recommendation at the current market price of $0.89, in view of the potential of benefitting from its US operations.

Afterpay Touch Group Limited (ASX: APT)

International Expansion: Following the successful launch of Afterpay in New Zealand during the second half of calendar year 2017, Afterpay Touch Group Limited has continued to investigate expanding its market leading product into other markets, while at the same time developing its internal capabilities and resources to ensure the Company’s ability to innovate and grow in its established markets is maintained. It is currently investigating opportunities to introduce Afterpay in the United States market. This process is at a preliminary stage and the Company will update shareholders in due course with respect to its longer-term strategy. It has entered into a strategic relationship and new share issuance transaction with Matrix Partners (Matrix). Matrix will collaborate with and provide advice to Afterpay Touch to further investigate and execute a potential expansion into the United States.

Financial Performance (Source: Company Reports)

Afterpay Touch does not expect Afterpay US to materially contribute to revenue in the 2018 financial year. Meanwhile, the group announced that 53,000,000 ordinary shares (Escrowed shares) and 4,300,000 options (Escrow options) in the Company will be released from Escrow on 4 May 2018. The stock price was down by 21.2 per cent in the last three months at the back of negative sentiments on growth, followed by an increase of 3.5 per cent in the last five days and a further rise of 4.2% on May 03, 2018 with reviving momentum amongst investors. APT otherwise posted a decent third quarter 2018 performance and delivered over 400% growth in the sales for the first three quarters of FY18, compared with the first three quarters of FY17. Given the recent payment related challenges, the group is set to establish tougher fraud checks. We give a “Hold” recommendation at the current market price of $6.2.

Netcomm Wireless Limited (ASX: NTC)

Accelerating Growth: The Group recently signed a Product Purchase Agreement with Bell Canada for the supply of Intelligent Fixed Wireless Access technology devices. Bell is Canada’s largest communications company and will be delivering high-speed broadband services to select rural communities, starting in Ontario and Quebec, using NetComm Wireless’ fixed wireless technology. As is the normal practice with Product Purchase Agreements in the telecommunications industry, no specific unit volumes are contained in the Agreement. However, NetComm Wireless is of the view that this Product Purchase Agreement will generate significant revenues in the coming financial years. NetComm Wireless anticipates that initial deliveries of the Intelligent Fixed Wireless Access devices should occur in Financial Year 2019, after attaining normal customer acceptance and required Canadian regulatory approvals.

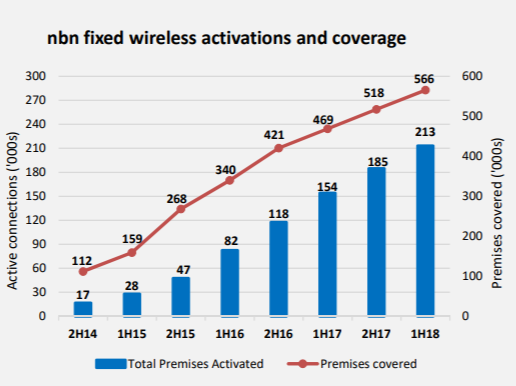

NBN Fixed Wireless activation and coverage Trend (Source: Company Reports)

This contract win with Bell Canada follows a successful 4-month in-field trial and builds on its previous fixed wireless contract wins with Ericsson / NBN in Australia and AT&T in the USA. It is another key milestone in the growth of its international footprint servicing tier 1 telecommunications carriers in developed markets. A practical and economical alternative to fibre, cable and copper networks, Fixed Wireless delivers broadband speeds to regional, remote and outer urban areas over 4G LTE networks worldwide. Recently, NBN Co Ltd (NBN) announced that it would increase its planned Fibre-to-the-Curb (FTTC) footprint, with an additional 440,000 homes and businesses around Australia set to receive the new technology. This takes the total planned FTTC footprint closer to 1.5 million homes and businesses by 2020. NetComm Wireless is hopeful that as the rollout progresses over the coming years, it will receive further orders. Since past three months, the price was up by 12.93 per cent and it rose by 3.8% on May 03, 2018. The potential is getting unearthed and we give a “Buy” recommendation at the current market price of $1.36.

iSignthis Limited (ASX: ISX)

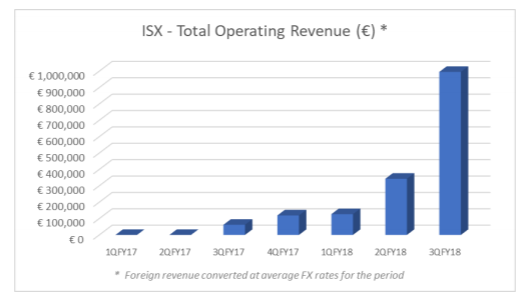

Continual transaction volume growth: Australian Securities and Frankfurt Stock Exchange cross-listed iSignthis Ltd, the global leader in RegTech for identity verification and transactional banking/payments, provided an update on the Quarterly Activities of the Business and reported an Unaudited revenue of A$1.48 million for the March quarter, representing a QoQ increase of 267%. Cash Receipts increased to A$1.571 million, representing approximately a 400% increase versus the December quarter (A$392k). The Company continues to increase the value of its contracted GPTV, which is now in excess of AU$500 million. Company continues research and development and extends IP portfolio with Chinese patent acceptance and filing of patents for new inventions

.

Operating Revenue (Source: Company Reports)

The ongoing focus is to continue to build on these numbers to reach a break-even position as quickly as possible. The Company is also resolving an upstream technical issue with one of its key suppliers. This short-term supply side technical issue affects the processing of payments to some of its merchants in the EEA area. The ability to divert traffic to other suppliers, even at a higher cost, is an essential design feature of the resilient ISX network, to ensure that it can offer maximum processing uptime to its merchants in the event of upstream supply issues. The Company currently has a strong pipeline of merchants on-boarding, which will in, turn, impact both operational core services revenue and the contracted book value for settlement services over the coming quarters. The stock has been declining for past six months that is by 21 per cent but rose up by 3.33 per cent on May 03, 2018. We give a “Speculative Buy” recommendation at the current market price of $0.155.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...