Stocks’ Details

Healthscope Limited

Speculation on group takeover: Healthscope Limited’s (ASX: HSO) stock rose 3.4% on April 12, 2018 due to the speculation that the company is a takeover target and is eyed by private equity firms BGH Capital and Bain Capital. BGH Capital was founded by former TPG Australia head Ben Gray and Simon Harle; and TPG, along with the Carlyle Group, paid $2.7 billion for Healthscope in 2010, which was later divested through an IPO. On the other hand, HSO’s Statutory NPAT from continuing operations fell 12.8% to $77.5 million in 1H 2018. The Group Revenue grew 4.9% to $1,222.1 million in 1H 2018 from recently completed and maturing brownfield hospital expansions. Moreover, Hospitals’ operating EBITDA projection for FY18 remains unchanged, which is expected to be broadly similar to FY17. Meanwhile, HSO stock has fallen 5.01% in three months as on April 11, 2018. As of now, we give a “Hold” recommendation on the stock at the current price of $ 1.960.

Ramsay Health Care Limited

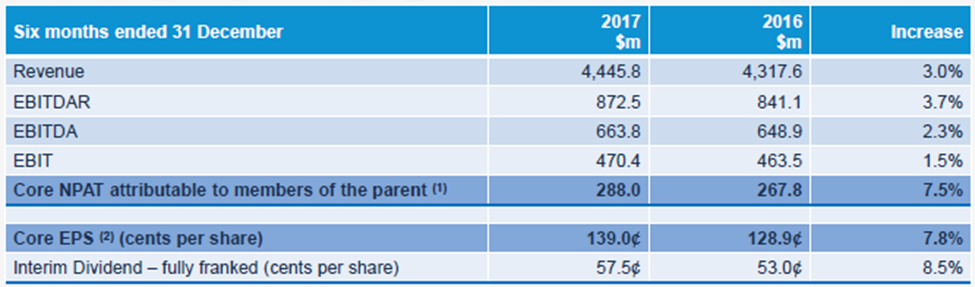

Aging Population Demand is growing:Ramsay Health Care Limited’s (ASX: RHC) stock has fallen 9.26% in three months as on April 11, 2018 as the company is facing challenging environment in Europe, but the company is investing in a major transformation project in the French operations that will centralise non-core hospital resources and distinguish this business for the long term. Further, in Australia, people aged over 65 form for more than 15% of the total population, which will increase the demand of the ageing population, and ensure RHC’s growth in admissions and procedural volumes. The increasing proportion of people with chronic disease and mental illness is also boosting treatment volumes. Meanwhile, RHC has delivered decent performance for 1H 2018, and reported 7.5% rise in Core net profit after tax to $288.0 million. The Group revenue grew 3.0% to $4.4 billion and Group EBIT is up 1.5% to $470.4 million in 1H 2018. The EBIT grew due to the strong performance in the Australian business. The Australian operations posted 9.1% EBIT growth on the previous corresponding period due to above market volume growth and the benefits of recent cost efficiency programmes. Additionally, RHC has reaffirmed the FY18 Core EPS growth of 8% to 10%. We give a “Buy” recommendation on the stock at the current price of $ 61.740.

1H 18 Group Financial Performance (Source: Company Reports)

Cochlear Limited

Reaffirmed FY18 net profit guidance:Cochlear Limited’s (ASX: COH) stock has fallen 4.30% in one month as on April 11, 2018 after the company for 1H 2018 reported 2% fall in the Cochlear implant units to 15,972 (units up 5% excluding Chinese Central Government tender units). The developed market unit growth for 1H 2018 is of 12%, but this was offset by a reduction in emerging market units, basis the timing of a number of tenders. The company’s reported net profit fell 1% to $110.8m (up 1% in CC). The reduction in US corporate tax rates, had reduced the reported net profit growth by 5%. Additionally, COH has reaffirmed FY18 net profit guidance of $240-250 million, which is a 7-12% increase on FY17. COH expects the full year net impact of the change in US tax legislation to reduce net profit by $3-4 million for the second half of FY18. Meanwhile, COH is trading at a high P/E. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $ 177.770.

CSL Limited

Uneven profit profile for the first and second halves of 2018:CSL Limited’s (ASX: CSL) stock has fallen 4.12% in one month as on April 11, 2018 as the company expects to have an uneven profit profile for the first and second halves of 2018, due to the seasonality of the influenza business and the timing of expenses, particularly research and development. The Group’s net profit after tax for FY18 is expected to be in the range of approximately $1,550 to $1,600 million at constant currency. Moreover, CSL expects strong ongoing demand for the company’s Behring biotherapies, including the strong patient uptake of the newly approved specialty product Haegarda. The haemophilia market is evolving and the new generation products, Idelvion (rFIX-FP) and Afstyla (rFVIII-SC) are well placed in the market. Further, CSL expects Helixate sales to decline in the future as the product winds down. The competition in the factor VIII space is intense as new entrants are coming to the market. Additionally, during the first half of FY18, CSL had raised approximately US$700 million through a US private placement, for general corporate purposes, which is a part of the company’s overall capital management program. Meanwhile, CSL is trading at a high level and looks “Expensive” at the current price of $ 159.290.

Bionomics Limited

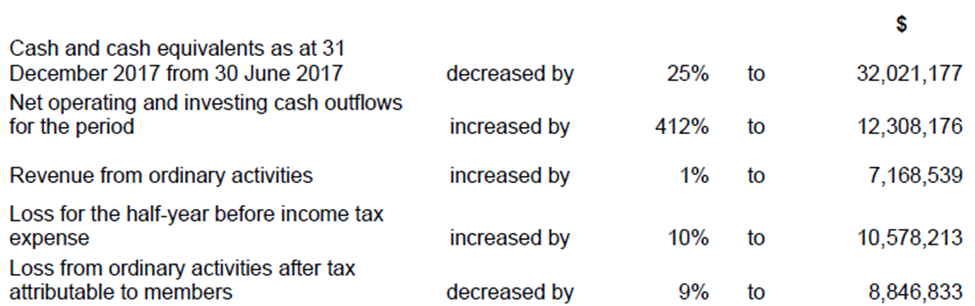

Losses fell in 1H 2018: Bionomics Limited’s (ASX: BNO) stock has risen 43.59% in three months as on April 11, 2018 after the company reported 9% fall in the loss from ordinary activities after tax attributable to members to $8,846,833 for 1H 2018 from $9,696,734 for prior corresponding period. The revenue for 1H 2018 grew by 1% to $7,168,539. The cash and cash equivalents as at 31 December 2017 from 30 June 2017 decreased by 25% to $32,021,177. This is in line with the company’s expectations, as the funds were slated to be used to meet the regulatory requirements. The group reported to have enrolment tracking to expectations in the Phase 2 clinical trial of BNC210 in Post-Traumatic Stress Disorder (PTSD). BNO has in fact announced for full recruitment in the RESTORE trial. The company has received FY17 R&D Tax Incentive refund ($6.788 million) in January 2018. We give a “Hold” recommendation on the stock at the current price of $ 0.570.

1H 18 Financial Performance (Source: Company Reports)

Nanosonics Limited

Expansion in Germany:Nanosonics Limited’s (ASX: NAN) stock has fallen 12.36% in three months as on April 11, 2018 after the company reported weak 1H 2018 results. NAN for 1H 2018 has delivered fall in the sales and net profit after tax. Moreover, NAN expects R&D spend to increase in second half. Beyond FY18, NAN expects the introduction of new products including the 2nd generation of trophon and is targeting one or more new infection prevention solutions in FY20, which is subject to regulatory approvals. Additionally, for second half of FY18, the company expects the potential to delay timing of capital purchase as the Healthcare reform in USA is ongoing. MES program in UK also continues to gain momentum, there is an expectation of FY18 new unit growth of 75% -100% over FY17, of which 90%+ of installations will be under MES. NAN also updated the market that the German Society of Ultrasound in Medicine (DEGUM) has published comprehensive recommendations for infection prevention in ultrasound and endoscopic ultrasound and the new guidelines address the cleaning and disinfection requirements for ultrasound and endoscopic ultrasound probes in procedures ranging from percutaneous interventions to transvaginal and transrectal ultrasound. These guidelines that focus on the aspect about ultrasound probe decontamination, and particularly, disinfection of all semi-critical ultrasound probes with disinfectants are expected to boost the use of NAN’s trophon® EPR device that is said to meet all the requirements. Basis this, NAN aims for higher direct sales and service infrastructure in Germany given the adoption of its Trophon system. We give a “Speculative Buy” recommendation on the stock at the current price of $ 2.360.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...